30 Sep, 2025

30 Sep, 2025

4 mins read

4 mins read

When investors explore mutual funds, one term that frequently comes up is AUM in mutual funds. At first glance, it might look like just another financial acronym, but Asset Under Management can tell you a lot about the scale, credibility, and efficiency of a fund. Does a larger AUM mean better performance? How does it compare with NAV? And how should you use this metric while choosing funds? This guide unpacks all of it in clear, simple terms.

Asset Under Management (AUM) refers to the total market value of all the financial assets a fund or financial institution manages on behalf of its clients. In the context of mutual funds, what is AUM in mutual funds is best understood as the combined value of all securities in a fund’s portfolio.

AUM includes:

Investments made by individual and institutional investors

Capital appreciation from rising asset values

Dividend or interest income

Net inflows minus redemptions

Think of it as the size of the mutual fund. Just like a business balance sheet grows or contracts, AUM fluctuates daily with market movements, new investments, withdrawals, and payouts.

AUM is more than just a number. Here is why it matters:

Indicator of popularity and trust: A high AUM reflects investor confidence and often a strong track record.

Operational efficiency: Large AUMs allow fund houses to reduce expense ratios because of economies of scale.

Liquidity assurance: Bigger funds can usually handle redemptions more smoothly without disrupting strategy.

Benchmarking performance: It helps compare funds within the same category. For example, among large-cap funds, a rising AUM may signal growing investor interest.

However, importance of AUM should not be overstated. A higher AUM does not guarantee better returns, especially if the fund strategy struggles in certain market segments.

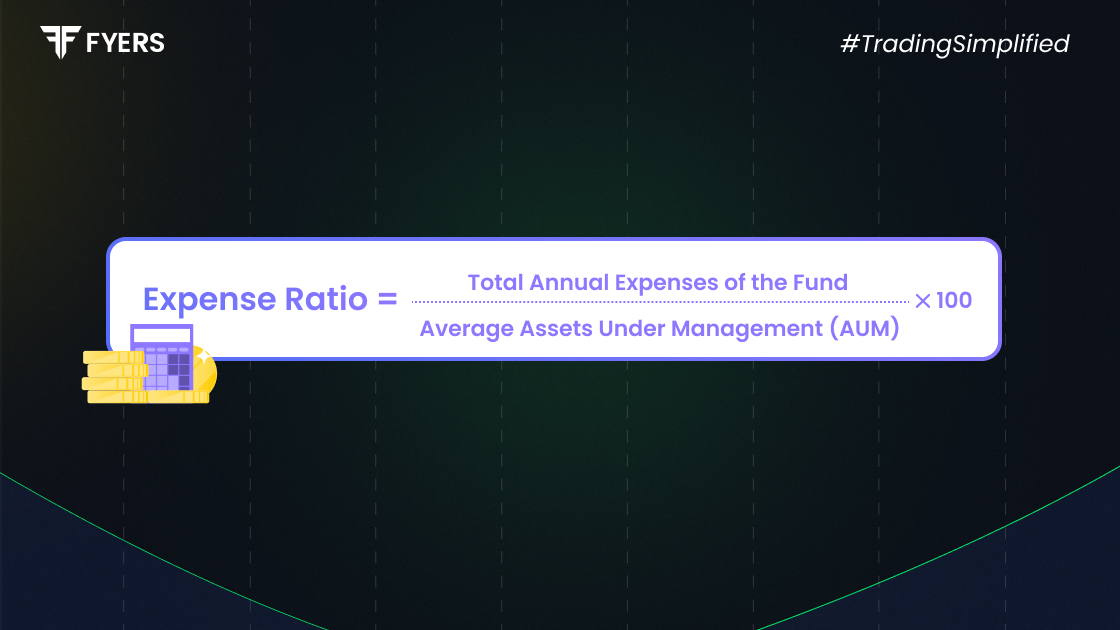

There is no single universal formula for AUM calculation, but the typical method is:

|

AUM = Market value of holdings + Cash & equivalents + Accrued income – Liabilities |

Market value of holdings: Value of stocks, bonds, or securities owned by the fund

Cash & equivalents: Uninvested cash or liquid instruments

Accrued income: Interest or dividends earned but not yet received

Liabilities: Pending obligations to be paid from the fund

Since asset values change constantly, how to calculate AUM is not a one-time exercise. Fund houses usually update AUM at the close of each trading day.

A frequent question for new investors is AUM vs NAV. Although they sound related, they serve different purposes:

|

Parameter |

AUM |

NAV |

|---|---|---|

|

Definition |

Total value of assets managed by the fund |

Per-unit value of the mutual fund |

|

Focus |

Size of the fund |

Price per unit/share |

|

Formula |

Market value of holdings + cash – liabilities |

(AUM – Liabilities) ÷ Total outstanding units |

|

Fluctuation basis |

Market movements, inflows and outflows |

Market value of holdings |

|

Investor impact |

Shows overall fund size |

Determines purchase or redemption price |

In short, net asset value vs. AUM can be thought of as unit price versus fund size. NAV affects what you pay or receive per unit, while AUM gives context about the fund’s overall scale.

AUM is a useful lens through which investors can assess mutual funds, but it should not be the only one. A high AUM can indicate trust, liquidity, and efficiency, yet it does not guarantee superior performance. More important is how the fund’s strategy aligns with your goals and how consistently it has delivered returns.

The AUM full form in finance is Asset Under Management. It represents the total value of assets a mutual fund or financial institution manages for its investors, including stocks, bonds, cash, and other securities.

Not always. A larger AUM might show investor confidence and fund stability, but performance depends more on the fund manager’s strategy and market conditions. Smaller funds can sometimes outperform bigger ones.

In India, mutual fund AUM is usually updated daily after the markets close. The value reflects market prices, inflows, redemptions, and other adjustments.

A high AUM often leads to lower expense ratios and improved fund stability. But in categories like small-cap funds, an excessively large AUM may reduce flexibility, making it harder to enter or exit smaller stocks without affecting their prices.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!