In the previous two chapters, we talked about various risks that investors are exposed to. In this chapter, we will turn our attention to the other end of the spectrum, i.e., trading, and focus on the key risks that traders face.

Types of Traders

Before talking about risks that traders face, let us first talk about the types of traders, as some risks that traders face are unique to their style of trading. Broadly, there are three types of traders:

- Intraday traders (aka day traders)

- Swing traders

- Positional traders

Let us understand each of these types.

Intraday trader: An intraday trader is a trader who creates positions and closes them out on the same day. The objective is to make small profits per trade and trade multiple times during the day, depending on opportunities in the market. Typically, but not always, an intraday trader intends to capture moves of up to 1-3%, depending on one’s risk appetite and volatility of the instrument. Some intraday traders try to capture moves of just a few ticks, such as 0.1%. Such intraday traders are commonly known as scalpers.

Swing trader: A swing trader is a trader who creates positions and holds them for more than one session, typically for a week or more. The objective is to make larger profits per trade than what an intraday trader makes. Depending on the volatility of the security, a swing trader aims to capture moves between 5-15%.

Positional trader: A positional trader is like a swing trader in that he or she creates positions and holds on to them for more than one session. However, a positional trader holds on to his or her position for an even longer time than a swing trader does. The duration could range from a few weeks to a few months. Naturally, the objective is to make larger profits per trade than what a swing trader makes. Typically, a positional trader aims to capture moves greater than 15-20%.

Leverage is a crucial part of Trading

When investors put money in the stock markets, they do so in the cash segment wherein they take delivery of shares by paying the entire sum (purchase price of a stock * quantity of shares purchased) and then hold on to the position for the long-term. On the other hand, traders trade in both cash market and derivatives market. Because time horizon and profit potential both tend to be very small in trading as compared to that in investing, leverage becomes quite an important tool for traders. To magnify the profit potential within a short time span, most traders prefer trading using margin money. This way, they gain exposure to an entire position by paying only a fraction of the total value of that position. Leverage is available both in the cash and the derivatives segment. In the cash segment, leverage is available for intraday positions only. For positions beyond intraday, the entire value needs to be paid.

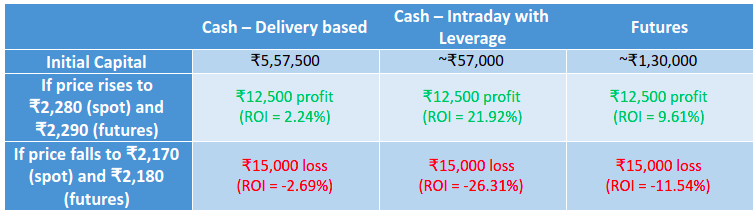

To explain the impact of leverage, let us take a simple example of Reliance Industries. At the time of writing, the spot price of Reliance is ₹2,230 and the futures price is ₹2,240. Also, the lot size of Reliance in futures is 250, meaning 1 contract in futures is worth 250 shares of Reliance. To keep things comparable, let us assume three scenarios:

- A trader buys 250 shares of Reliance in the cash segment and takes delivery. In this case, the trader will have to pay the entire value of 250 shares, which happens to be ₹5,57,500

- A trader buys 250 shares of Reliance in the cash segment on intraday basis (say, a cover order). Because the trade is intraday (entry & exit on the same day), he or she will be able to trade on margin, which happens to be ~₹57,000 as at the time of writing (leverage of almost 10x)

- A trader buys 1 lot of Reliance futures. In this case, the trader will require a margin of around ₹1,30,000 (leverage of almost 4x)

To calculate the leverage we provide, please visit our FYERS margin calculator page by clicking here. In each of the above case, the trader is taking position worth ~₹5.6 lacs. However, notice that the capital required under cash – intraday and under derivatives is much lower than that required for delivery-based trading. Let us now look at the profit/loss potential for a given rise/fall in the price of Reliance.

Notice above that the absolute profit or loss are the same in each of the case. However, what differs is the return on investment (or trade in this case). Notice that the ROI tends to be substantially higher when leverage comes into play. This is the impact of leverage. That said, also notice that leverage is a double-edged sword. If your view goes wrong, then losses on your leveraged positions can be substantial as well. I mean, imagine an intraday loss of ₹15,000 on a capital deployed of ₹57,000. Quite substantial, right? In short, the higher the leverage, the higher can be the returns but so can be the risks. Hence, risk management is extremely critical in trading, especially when one is taking leveraged positions.

Now that we understand the three types of traders and the importance of leverage in trading, let us talk about the various risks that traders are exposed to.

Overnight price risk

This is a risk that swing and positional traders face when carrying positions overnight. Thus, they expose themselves to the risk of a gap between the closing price on one session and the opening price on the following session. Small gaps between two sessions are fine and are in fact quite common. However, big gaps can have a profound impact on a trader’s capital, either positively or negatively. Sometimes, a large opening price gap against a trader’s position can severely erode his/her capital and prompt the trader to get a margin call from his/her broker. Hence, this is a very critical factor to consider, especially when carrying overnight positions in derivatives, in which the profit/loss potential tends to be very high. What factors cause the price to gap up or down between two sessions? Well, there could events lined up and market developments happening outside of market hours. Examples include a major company announcement, an unexpected news about a company, release of an important economic data, global developments and news flows affecting market sentiment etc.

How does one reduce the risks posed by carrying positions overnight?

Well, some overnight events, such as company results and economic data, are known in advance. When such known events are lined up, a trader could simply refrain from carrying overnight a position that he or she believes will be impacted by that event; or use hedging strategies using call or put options to minimize the impact of such events. Alternatively, a trader could backtest and see how the price of the underlying instrument has reacted to such post-market hour events in the past. If the historical opening gaps are well within a trader’s risk tolerance limit per trade, he or she can consider carrying some positions overnight (such as, say, half). However, some events cannot be predicted beforehand, such as unscheduled events, overnight market sentiment etc. The only way to avoid them is to ensure that the positions being carried overnight are not large enough to adversely impact one’s trading capital. This is where position sizing and risk management come into the picture. A swing or a positional trader must devise his/her position size and risk management strategies in such a way that overnight surprises, if any, will not have much of a negative impact on the trading capital.

Yet another, unorthodox way to manage overnight price risk is by gauging your state of mind whenever you carry such positions. Is it affecting your sleep? Are you regularly monitoring movements in the global markets at a time when you should ideally be sleeping at night? If yes, then this may be a sign that you are carrying excessive overnight positions. In such a case, you may need to revisit your position sizing and risk management strategies and make necessary amendments to account for the excess positions that you might be carrying beyond a session.

Slippage

Slippage occurs when a trade gets executed at a price that is less favorable than the one at which it was placed. Examples include entering a market order to buy when the ask price is ₹100, but which instead gets executed at ₹100.15; or exiting a long position when the bid price is ₹105, but which gets executed at ₹104.9. While all traders are impacted by slippage, intraday traders tend to suffer the most. This is because their profit potential on a trade tends to be quite small. Hence, slippage costs can eat up a portion of their winning trade or can widen the losses of their losing trade. When do slippages occur? Usually when volatility is high or liquidity is low. When the volatility is high, swift price movement and changes in the bid-ask spread could lead to slippages when one is trying to execute a market order. Slippages are also common when liquidity is low because the price at which you want to transact (buy or sell) may not have sufficient volume to execute your quantity.

How do you reduce the risk of slippage?

Well, one way is to place limit or stop-limit order rather than market order when entering or exiting trades. Let me explain this using an example. If a stock is currently trading at 100.00/100.05 and you are looking to buy at ₹100, you could place a buy limit order at ₹100. This order would get executed when the ask price falls to ₹100 or lower. On the other hand, if you place a market order to buy when the price is 100.00/100.05 but then the price rises to 100.10/100.15 between the time the order is placed and gets executed, your trade will be executed at ₹100.15, leading to a ₹0.1 slippage. Let me take another example. If you are short a stock at, say, ₹100 and want to safeguard against a price rise, you could consider a buy stop-limit order by placing stop loss price and limit price at, say, ₹100.5 and ₹100.55, respectively. If the stock were to rise and hit ₹100.5, the stop would be triggered and the order would get converted to a limit order. As the limit price is ₹100.55, the position would get executed at a price not more than ₹100.55. On the other hand, what if you placed a buy stop order at ₹100.5? In that case, if the stock were to rise and hit ₹100.5, the stop would be triggered and the order would get converted to a market order. The stock would then be bought at the prevailing market price. If that is above ₹100.5, you would incur slippage.

However, please note that while limit and stop-limit order will help in avoiding slippages, there is a risk that the order might not get executed. For instance, in the above case, after placing a buy limit order at ₹100, if the market price does not fall to ₹100 but instead rises to ₹101, you will miss out on the trade. Similarly, after placing a stop-limit order with stop price at ₹100.5 and limit price at ₹100.55, the trade will not be executed if there is a gap up from, say, ₹100.4 to ₹100.8. While the stop would be triggered, the trade will not be executed until the price falls to the limit price of ₹100.55. Hence, see that there is a trade-off between slippage and execution. If slippages are of foremost concern, then limit orders make sense. However, if execution is a foremost priority irrespective of price at which the trade is executed, then market orders would be more suitable.

Another way traders (especially intraday traders) can reduce the risk of slippage is by ensuring to:

- Trade liquid securities

- Trade during times when liquidity tends to be ample, and

- Trade when volatility is low to moderate but not too high

Leverage risk

As said earlier, leverage is a double-edged sword. If your view goes right, your profit can be substantial. However, if your view goes wrong and the risk is not managed well, the losses could be catastrophic. The higher the leverage, the larger can the loss potential get. Let me explain using an example. To take delivery of 250 shares of Reliance at a price of ₹2,200/share, you need to pay ₹5,50,000. However, to gain an overnight exposure to the same number of shares in futures, you need a margin of ~₹1,30,000. This reduces even further to ~₹65,000 in case of an intraday position in futures. Let us say you have ₹6 lacs in your trading account. Based on your reading of the chart, you feel that the price of Reliance would rise intraday. Hence, you decided to place a cover order and go long 8 lots of Reliance futures, paying a margin of ₹5,20,000 (65000 * 8). Let us assume your view went wrong and the price fell to ₹2,140 in a couple of hours, based on which you decided to exit the trade. In this case, you would have suffered a loss of ₹15,000 per lot ((2140 - 2200) * 250), which translates to a total loss of ₹1,20,000 (15000 * 8). So, just in a couple of hours, the capital in your account would have been wiped out by 20% (120000 ÷ 600000). On the other hand, had you instead bought 250 shares in the cash market (delivery basis), your total loss would just have been ₹15,000 ((2140 - 2200) * 250). In this case, your overall capital would have reduced by just 2.5% (15000 ÷ 600000).

Did you notice the difference between the two above? While capital deployed was nearly identical in both, the significantly larger loss in futures was because of the excess leverage the trader took. See that a 2.7% decline in the price of the stock led to a 20% capital erosion when excess leverage was taken but just a 2.5% erosion when no leverage was taken. This does not mean that one should not use leverage when trading. In fact, leverage is an indispensable part of trading. Without leverage, your risks and loss potential will reduce, but so would the reward potential. Hence, one needs to a strike a balance between the two in a way that if the trade pans out as expected, you would be able to earn handsome profits; but if the trade goes wrong, your capital will still not take a hit in just a single trade.

How do you efficiently manage leverage risk?

Well, before trading, one must always have in place proper risk and money management strategies. One way to achieve this is to first decide on position sizing and determine what is the maximum that you are willing to lose per trade. This will vary from trader to trader depending on one’s risk profile, trading style, and trading experience. Let us assume the risk you are willing to take per trade is 2% of your total capital. Based on this, if your trading capital is ₹6 lacs, the maximum you are willing to lose per trade would amount to ₹12,000. Now that the risk per trade has been determined, the next step is to calculate the stop loss for the trade. One way to do this is using the below formula:

Continuing with our above example of Reliance futures, if the number of lots you intend to trade is 1, then given the lot size of 250 and risk per trade of ₹12,000, your stop loss should be:

What this figure tells is that your stop loss should be 48 points away from the entry level, such that the maximum you could lose out on this trade is ₹12,000. For instance, if the buy entry level is ₹2,200, your stop loss should be placed at ₹2,152. In case this stop loss is hit, your loss would amount to ₹12,000. On the other hand, if you decide to trade 2 lots instead of 1 lot, your stop loss would be 24 points away from the entry level. With 5 lots, your stop loss would be just 9.6 points away from the entry level. In short, the more the number of lots you trade, the closer your stop loss will be from the entry price for a given risk per trade. See that in each of these cases, the maximum you are risking per trade is ₹12,000. This way, you would ensure that even if your view goes wrong, your capital will not take much of a hit.

This is just one of the many ways that a trader can use to efficiently manage leverage. The point I am trying to make is that with proper risk and money management strategies in place, one can enjoy the benefits of leverage but at the same time know how much to risk per trade without having much of a dent on the trading capital.

Recapping the Module thus far

So far in the module, we have covered the basics of risk, introduced the concept of risk and money management, and described the various risks that investors and traders are exposed to. In the next few chapters, we will talk about the statistical tools of measuring risk (and return).

Next Chapter

Comments & Discussions in

FYERS Community