RATIO CALL SPREAD

| Strategy Details | |

| Strategy Type | Neutral to slightly Bullish |

| # of legs | 3 (Long 1 Lower Strike Call + Short 2 Higher Strike Calls) |

| Maximum Reward if price declines | Limited to the extent of Net Premium Received |

| Maximum Reward if price rallies | Higher Strike Price - Lower Strike Price + Net Premium Received |

| Maximum Risk | Unlimited |

| Breakeven Price | Higher Strike Price + Difference between Higher and Lower Strike + Net Premium Received |

| Payoff Calculation | Payoff of Long Call+ (2 * Payoff of Short Call) |

In the above table, we have assumed the traditional 2:1 ratio wherein the trader is writing 2 Calls and buying 1 Call. However, note that this strategy can be executed using other combinations as well, such as writing 3 Calls and buying 2 Calls, writing 4 Calls and buying 2 Calls, writing 6 Calls and buying 4 Calls etc. The most commonly used short-long ratio to trade this strategy is 2:1 followed by 3:2. For our discussion henceforth, we will assume a total of 3 legs i.e. 2 Calls short at a higher strike and 1 Call long at a lower strike.

Explanation of the Strategy

A Ratio Call Spread is a strategy that involves buying 1 lower strike Call and writing 2 higher strike Calls having the same strike price, underlying, and expiration. Unlike a Ratio Call Backspread, which is primarily a capital appreciation strategy, a Ratio Call Spread is an income strategy. Because a greater number of Calls are written than are bought, this strategy has limited reward and unlimited risk profile. As such, this strategy must be initiated by experienced option traders only. This strategy can be either a net debit strategy or a net credit strategy. However, given the risk profile of this strategy, a net credit is almost always preferable over a net debit.

Usually, this strategy is initiated by buying 1 ATM or ITM Call option and simultaneously selling 2 OTM Call options. When initiated for a net credit, this strategy has one breakeven point. You would profit as long as the underlying price is below the breakeven point. Maximum profit under this strategy is limited and occurs when the underlying price rises to the higher strike price. Meanwhile, in case the underlying price declines and moves below the lower strike, the trader will get to retain the net premium. On the other hand, maximum loss under this strategy is unlimited and occurs when the underlying price rises above the breakeven point. The higher the underlying price moves above the breakeven point, the larger will be the losses.

Ratio Call Spread is a neutral to slightly bullish strategy that benefits when the underlying price either stays rangebound or rises but only up to the higher strike price. Because this strategy is exposed to unlimited risk, a trader should consider exiting this strategy or modifying it in a way to make it bullish, should the underlying price rise above the breakeven point. Compare this strategy to a Bull Call Spread, which is a moderately bullish strategy that involves buying an ATM Call and writing an OTM Call. The addition of the second OTM short Call is what makes the Ratio Call Spread a neutral strategy.

Benefits of the Strategy

-

Is mostly executed as a net credit strategy, in which case no upfront payment is needed

-

The trader gets to retain the net credit in case the underlying consolidates

-

Theta works in the trader’s favour

Drawbacks of the Strategy

-

This strategy is exposed to unlimited risk in case the underlying price rises sharply

-

Because this is a low volatility strategy, a surge in volatility could hurt the trader

-

Because this strategy involves selling more options than buying, it will require a greater margin in your trading account

Strategy Suggestions

-

Ensure that the trend is range bound and that there is a strong resistance at a higher level, beyond which you do not see the underlying price rising

-

Keep in mind that the number of Calls sold must exceed the number of Calls bought. The ideal short-long ratio for this strategy is 2:1 and to some extent even 3:2

-

Although this strategy can be initiated for net debit, avoid doing so and always prefer a net credit

-

When choosing strikes, do not just randomly select any strike. Remember, you want the underlying price to remain range bound, so select strikes accordingly and realistically

-

The difference between the lower strike and the higher strike will be a trade-off between net credit and risk

-

The narrow the difference between the two strikes, the larger would be the net credit but so would be the risk, and vice versa.

-

Because this strategy is a low volatility strategy, ensure that the underlying instrument being chosen for this strategy is and will likely continue exhibiting low volatility

-

Because you have a greater number of short Calls than long Calls and because you want the underlying price to stay range bound, give yourself little time to go wrong by selecting options that have fewer days to expiry

-

Ensure there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Ratio Call Spread

At the time of initiation, the sign of Greeks can vary depending upon the distance between the strike price of the long Call (lower strike) and those of the two short Calls (higher strike). Hence, we shall be talking about Greeks in general without discussing about the sign of each Greek at initiation.

| Greek | Notes |

| Delta |

As the underlying price rises and moves away from the lower strike, Delta rises. However, by the time the underlying price approaches the higher strike, Delta would have started falling sharply to move into negative. Meanwhile, the more the underlying price rises above the higher strike, the deeper the Delta goes into negative. Eventually, Delta starts flattening out as the underlying price moves above the breakeven point, meaning the impact of Delta on the option position starts reducing. |

| Gamma |

Above the lower strike, Gamma is negative most of the time and has the highest impact on Delta when the underlying price is near the higher strike. Once the underlying price moves above the higher strike, Gamma starts tapering off (i.e. becomes less negative). As the underlying price rises further to approach the breakeven point, Gamma would have reached near zero, meaning its impact on Delta would have turned negligible. |

| Vega |

As this strategy involves writing more Calls than buying Calls, Vega is negative most of the time, meaning that rising volatility hurts the option position, and vice versa. Vega tends to bottom out near the higher strike, meaning it is at this point where the negative impact of rising volatility is the greatest on the option position. |

| Theta |

As this strategy involves writing more Calls than buying Calls, Theta is positive for most of the time, meaning that time decay benefits the option position. Theta tends to peak out near the higher strike, meaning it is at this point where the positive impact of time decay is the greatest. |

| Rho |

As this strategy involves writing two Calls as opposed to buying one Call, Rho turns negative as the underlying price rises and approaches the higher strike. As a result, rising interest rates can hurt the option position at higher levels. That said, this is the least significant of the Greeks, especially in case of short-dated options. |

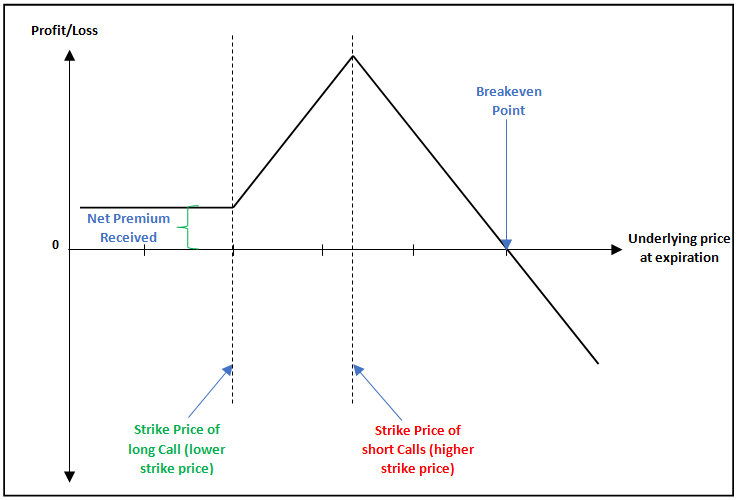

Payoff of Ratio Call Spread

The above is the payoff chart of Ratio Call Spread strategy. As can be seen, this strategy benefits from a modest rise in the underlying price. Maximum profit is achieved when the underlying price rises to the higher strike price. Beyond this, the profitability starts reducing. Meanwhile, if the underlying price crosses above the breakeven point, the trader will start incurring losses. The higher the underlying price rises above the breakeven point, the higher will be the trader’s losses. Also observe that because this strategy is established as a net credit strategy, the trader will also profit in case the underlying price drops below the lower strike price. In this case, the maximum profit will be limited to the extent of the net premium received, no matter how lower the underlying price drops below the lower strike.

Example of Ratio Call Spread

Let us say that Mr. ABC has looked at the chart of Tata Steel and has decided to initiate a Ratio Call Spread strategy, wherein he will buy 1 slightly ITM 290 Call at ₹19 and sell 2 OTM 300 Calls at ₹14 each. Let us summarize the details of the strategy below:

-

Strike price of longCall = 290

-

Strike price of shortCall = 300

-

Quantity of Calls bought = 1 lot

-

Quantity of Calls sold = 2 lots

-

LongCall premium (lower strike) = ₹19

-

Short Call premium (higher strike) = ₹14

-

Net Credit = ₹9 (2 * 14 - 19)

-

Net Credit (in value terms) = ₹13,500 (9 * 1500)

-

Breakeven point = 319 (300 + 10 + 9)

-

Maximum downside reward = ₹13,500

-

Maximum upside reward = ₹28,500 ((300 - 290 +9) * 1500)

-

Maximum risk = Unlimited

Now, let us assume a few scenarios in terms of where Tata Steel would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 250 | Profit of ₹13,500 | Payoff = [Maximum of (250-290,0)-19]+[2*{14-maximum of (250-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 270 | Profit of ₹13,500 | Payoff = [Maximum of (270-290,0)-19]+[2*{14-maximum of (270-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 290 | Profit of ₹13,500 | Payoff = [Maximum of (290-290,0)-19]+[2*{14-maximum of (290-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 295 | Profit of ₹21,000 | Payoff = [Maximum of (295-290,0)-19]+[2*{14-maximum of (295-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 300 | Profit of ₹28,500 | Payoff = [Maximum of (300-290,0)-19]+[2*{14-maximum of (300-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 310 | Profit of ₹13,500 | Payoff = [Maximum of (310-290,0)-19]+[2*{14-maximum of (310-300,0)}]. As the underlying price at expiration is below the breakeven price, the trader will make a profit |

| 319 | No profit, No loss | Payoff = [Maximum of (319-290,0)-19]+[2*{14-maximum of (319-300,0)}]. As the underlying price at expiration is equal to the breakeven point, the trader will neither profit nor incur a loss |

| 320 | Loss of ₹1,500 | Payoff = [Maximum of (320-290,0)-19]+[2*{14-maximum of (320-300,0)}]. As the underlying price at expiration is above the breakeven point, the trader will make a loss |

| 330 | Loss of ₹16,500 | Payoff = [Maximum of (330-290,0)-19]+[2*{14-maximum of (330-300,0)}]. As the underlying price at expiration is above the breakeven point, the trader will make a loss |

| 350 | Loss of ₹46,500 | Payoff = [Maximum of (350-290,0)-19]+[2*{14-maximum of (350-300,0)}]. As the underlying price at expiration is above the breakeven point, the trader will make a loss |

Notice in the above table that because this strategy is initiated as a net credit strategy, the trader gets to keep the entire net credit if the underlying price falls below the lower strike price of 290. The profit starts increasing as the price of Tata Steel rises. Under this strategy, maximum profit is ₹28,500 and occurs when the price of Tata Steel is at the higher strike price of 300. However, if the underlying price continues rising and crosses the breakeven point, the trader will start incurring losses, which can potentially be catastrophic.

RATIO PUT SPREAD

| Strategy Details | |

| Strategy Type | Neutral to slightly bearish |

| # of legs | 3 (Long 1 Higher Strike Put + Short 2 Lower Strike Puts) |

| Maximum Reward if price rallies | Limited to the extent of Net Premium Received |

| Maximum Reward if price declines | Higher Strike Price - Lower Strike Price + Net Premium Received |

| Maximum Risk | Unlimited |

| Breakeven Price | Lower Strike Price - Difference between Higher and Lower Strike - Net Premium Received |

| Payoff Calculation | Payoff of Long Put+ (2 * Payoff of Short Put) |

In the above table, we have assumed the traditional 2:1 ratio wherein the trader is writing 2 Puts and buying 1 Put. However, note that this strategy can be executed using other combinations as well, such as writing 3 Puts and buying 2 Puts, writing 4 Puts and buying 2 Puts, writing 6 Puts and buying 4 Puts etc. The most commonly used short-long ratio to trade this strategy is 2:1 followed by 3:2. For our discussion henceforth, we will assume a total of 3 legs i.e. 2 Puts short at a lower strike and 1 Put long at a higher strike.

Explanation of the Strategy

A Ratio Put Spread involves buying 1 Put at a higher strike and simultaneously writing 2 Puts at a lower strike. Each of these options are for the same underlying instrument and for the same expiration. This is a neutral to slightly bearish strategy wherein the trader benefits when the underlying price either consolidates, or better yet, falls up to the lower strike price. A Ratio Put Spread can either be a net credit or a net debit strategy. However, because this strategy has a limited reward and an unlimited risk profile, it always makes sense to establish this as a net credit strategy. Doing so would enable the trader to earn some profits even if the underlying price were to rise to expiration.

When established as a net credit strategy, a Ratio Put Spread has just one breakeven point. The good news is that the trader is in a profitable position as long as the underlying price is above the breakeven point. The bad news is that if the underlying price drops below the breakeven point, the losses could be unlimited. Because of the potential for unlimited losses, a Ratio Put Spread must be executed by experienced traders only. Also, a stop loss must always be in place in case the underlying price declines below the breakeven point.

A Ratio Put Spread is an income strategy, unlike a Ratio Put Backspread which is a capital gain strategy. Because this strategy works best when the underlying is either sideways or declines slightly up to the lower strike, it must be executed on less volatile instruments rather than on volatile instruments. Hence, before executing this strategy, see metrics such as Implied Volatility to ensure than the instrument is not exhibiting volatility. Also, because this strategy involves writing more Puts than buying Puts, see that you give yourself as little time to go wrong as possible.

Benefits of the Strategy

-

Is mostly executed as a net credit strategy, in which case no upfront payment is needed

-

The trader gets to retain the net credit in case the underlying consolidates below the lower strike

-

Theta works in the trader’s favour

-

The trader is in a profitable position as long as the underlying price is above the breakeven point

Drawbacks of the Strategy

-

This strategy is exposed to unlimited risk in case the underlying price falls sharply

-

Because this is a low volatility strategy, a surge in volatility could hurt the trader

-

Because this strategy involves selling more options than buying, it will require a greater margin in your trading account

Strategy Suggestions

-

Ensure that the trend is range bound to slightly bearish and that there is a strong support at a lower level, below which you do not see the underlying price dropping

-

Keep in mind that the number of Puts sold must exceed the number of Puts bought. The ideal short-long ratio for this strategy is 2:1 and to some extent even 3:2

-

Although this strategy can be initiated for net debit, avoid doing so and always prefer a net credit

-

When choosing strikes, do not just randomly select any strike. Remember, you want the underlying price to remain in a narrow range, so select strikes accordingly and realistically

-

The difference between the lower strike and the higher strike will be a trade-off between net credit and risk

-

The narrow the difference between the two strikes, the larger would be the net credit but so would be the risk, and vice versa.

-

Because this strategy is a low volatility strategy, ensure that the underlying instrument being chosen for this strategy is exhibiting low volatility and is likely to continue doing so going forward

-

Because you have a greater number of shortPuts than longPuts and because you want the underlying price to stay within a narrow range, give yourself little time to go wrong by selecting options that have less life remaining

-

Ensure there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Ratio Put Spread

At the time of initiation, the sign of Greeks can vary depending upon the distance between the strike price of the two Short Puts (lower strike) and that of the long Put (higher strike). Hence, we shall be talking about Greeks in general without discussing about the sign of each Greek at initiation.

| Greek | Notes |

| Delta |

As the underlying price falls and moves away from the higher strike, Delta falls. However, by the time the underlying price approaches the lower strike, Delta would have startedrising sharply to move into positive. Meanwhile, the more the underlying price fallsbelow the lower strike, the deeper the Delta goes into positive. Eventually, Delta starts flattening out as the underlying price drops below the breakeven point, meaning the impact of Delta on the option position starts reducing. |

| Gamma |

Below the higher strike, Gamma is negative most of the time and has the highest impact on Delta when the underlying price is near the lower strike. Once the underlying price fallsbelow the lower strike, Gamma starts tapering off (i.e. becomes less negative). As the underlying price falls further to approach the breakeven point, Gamma would have reached near zero, meaning its impact on Delta would have turned negligible. |

| Vega |

As this strategy involves writing more Puts than buying Puts, Vega is negative most of the time, meaning that rising volatility hurts the option position, and vice versa. Vega tends to bottom out near the lower strike, meaning it is at this point where the negative impact of rising volatility is greatest on the option position. |

| Theta |

As this strategy involves writing more Puts than buying Puts, Theta is positive for most of the time, meaning that time decay benefits the option position. Theta tends to peak out near the lower strike, meaning it is at this point where the positive impact of time decay is the greatest. |

| Rho |

As this strategy involves writing two Puts as opposed to buying one Put, Rho turns positive as the underlying price falls and approaches the lower strike. As a result, rising interest rates can benefit the option position at lower levels. That said, this is the least significant of the Greeks, especially in case of short-dated options. |

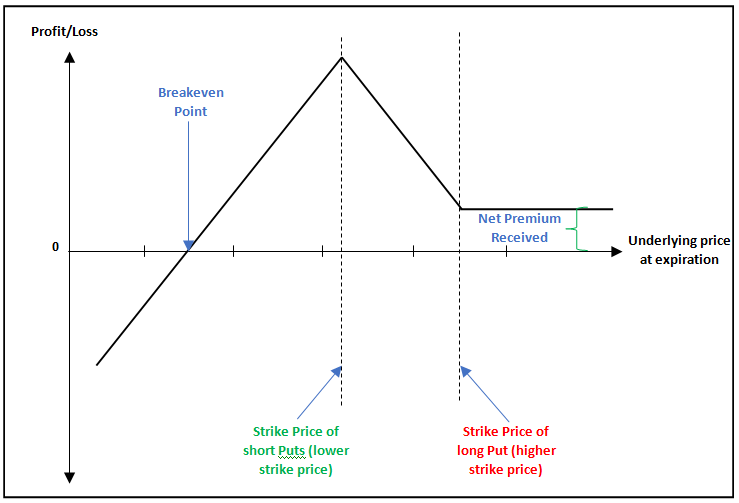

Payoff of Ratio Put Spread

The below is the payoff chart of a Ratio Put Spread. Observe that the strategy is profitable even if the underlying price rises above the higher strike, in which case the trader gets to keep the entire net credit. This, however, is assuming that the strategy is established for a net credit. From the time of initiation, see that this strategy benefits when the underlying price falls moderately until expiration. The sweetest spot of this strategy occurswhen the underlying price drops to the lower strike price, in which case the trader earns maximum profit. Also see that this strategy will hurt the trader if the underlying price drops below the breakeven point, as losses will start kicking in, which can be potentially unlimited.

Example of Ratio Put Spread

Let us say that Mr. ABC has looked at the chart of ICICI Bank and has decided to initiate a Ratio Put Spread strategy, wherein he will buy 1 ITM 380 Put at ₹25 and sell 2 OTM 360 Puts at ₹16 each. Let us summarize the details of the strategy below:

- Strike price of longPut = 380

- Strike price of shortPut = 360

- Quantity of Puts bought = 1 lot

- Quantity of Puts sold = 2 lots

- LongPut premium (higher strike) = ₹25

- Short Put premium (lower strike) = ₹16

- Net Credit = ₹7 (2 * 16 - 25)

- Net Credit (in value terms) = ₹9,625 (7 * 1375)

- Breakeven point = 333 (360 - 20 - 7)

- Maximum reward if the price rallies = ₹9,625

- Maximum reward if the price falls= ₹37,125 ((380 - 360 + 7) * 1375)

- Maximum risk = Unlimited

Now, let us assume a few scenarios in terms of where ICICI Bank would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 420 | Profit of ₹9,625 | Payoff = [Maximum of (380-420,0)-25]+[2*{16-maximum of (360-420,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 400 | Profit of ₹9,625 | Payoff = [Maximum of (380-400,0)-25]+[2*{16-maximum of (360-400,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 380 | Profit of ₹9,625 | Payoff = [Maximum of (380-380,0)-25]+[2*{16-maximum of (360-380,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 370 | Profit of ₹23,375 | Payoff = [Maximum of (380-370,0)-25]+[2*{16-maximum of (360-370,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 360 | Profit of ₹37,125 | Payoff = [Maximum of (380-360,0)-25]+[2*{16-maximum of (360-360,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 345 | Profit of ₹16,500 | Payoff = [Maximum of (380-345,0)-25]+[2*{16-maximum of (360-345,0)}]. As the underlying price at expiration is above the breakeven price, the trader will make a profit |

| 333 | No profit, No loss | Payoff = [Maximum of (380-333,0)-25]+[2*{16-maximum of (360-333,0)}]. As the underlying price at expiration is equal to the breakeven point, the trader will neither profit nor incur a loss |

| 320 | Loss of ₹17,875 | Payoff = [Maximum of (380-320,0)-25]+[2*{16-maximum of (360-320,0)}]. As the underlying price at expiration is below the breakeven point, the trader will incur a loss |

| 300 | Loss of ₹45,375 | Payoff = [Maximum of (380-300,0)-25]+[2*{16-maximum of (360-300,0)}]. As the underlying price at expiration is below the breakeven point, the trader will incur a loss |

| 280 | Loss of ₹72,875 | Payoff = [Maximum of (380-280,0)-25]+[2*{16-maximum of (360-280,0)}]. As the underlying price at expiration is below the breakeven point, the trader will incur a loss |

Notice in the above that as long as the underlying price is above the breakeven point, the trader makes a profit. The maximum profit under this strategy is ₹37,125 and occurs when the underlying price declines to the lower strike price. Meanwhile, observe that when the underlying price rises above the higher strike, the trader gets to keep the entire net credit of ₹9,625, no matter how higher the underlying price rises. On the flip side, observe that if the underlying price drops below the breakeven point, the trader starts suffering losses. The larger the decline in underlying price below the breakeven point, the larger will be the loss.

Next Chapter

Comments & Discussions in

FYERS Community