BULL CALL SPREAD

| Strategy Details | |

| Strategy Type | Moderately bullish |

| # of legs | 2 (Long ATM Call + ShortOTM Call) |

| Maximum Reward | (Strike price of short Call - Strike price of long Call) - (Premium of long Call - Premium of short Call) |

| Maximum Risk | Premium of long Call - Premium of short Call |

| Breakeven Price | Strike price of long Call + Premium of long Call - Premium of short Call |

| Payoff Calculation | Payoff of Long Call + Payoff of Short Call |

Explanation of the Strategy

A Bull Call Spread is a strategy that involves buying a Call option that has a lower strike price and simultaneously selling a Call option that has a higher strike price. Traditionally, the Call option that is bought is an ATM Call option and the Call option that is sold is an OTM Call option. When entering into this strategy, both the options must have the same underlying and must be for the same expiry. What differs is just the strike price and the premium. Unlike a naked long Call, a Bull call Spread is a moderately bullish strategy. Both profits and losses are limited under this strategy. Maximum profit potential is achieved when the underlying price rises to the higher strike price (i.e. the strike price of the short Call). Beyond this, no matter how higher the underlying price goes, the trader does not earn anything more. On the other hand, the trader suffers maximum loss when the underlying price falls to the lower strike price (i.e. the strike price of the long Call), a level where both the options expire worthless. Below this, no matter how lower the underlying price goes, the trader does not incur any more losses.

Because the strategy does not generate any further profits once the underlying price rises beyond the higher strike price, a Bull Call Spread must be deployed only when one has a moderately bullish outlook on the underlying.This strategy is unlike a naked long Call, in which the trader has anoutright bullish stance on the underlying. A disadvantage of a Bull Call Spread over a naked long Call is that the former has a limited profit potential while the latter an unlimited profit potential. However, an advantage of a Bull Call Spread over a naked long Call is that the former reduces the cost of the strategy because of the proceeds received from shorting a Call. Another advantage is that a Bull Call Spread has a lower breakeven point than a naked long Call. Meanwhile, the breakeven point of the strategy is calculated as the strike price of the long Call plus the difference between the premium amounts. Because this strategy is moderately bullish, the trader would want the price of the underlying to rise above the breakeven point for him/her to start making profits. This is because as long as the price of the underlying remains below the breakeven point, the trader will be in a loss-making position.

Benefits of the Strategy

-

The major advantage of this strategy is that it reduces the total cost of the strategy

-

Because of the lower total cost, the risk of the strategy is also less

-

Profit as a percent of the total cost will be higher for this strategy than that for a naked long Call if the underlying price rises up to the strike price of the short Call

-

This strategy has a lower breakeven point, which means that to become profitable, the underlying price will not have to rise as much as it would have to in case of a naked long Call

Drawbacks of the Strategy

-

This strategy has a limited profit potential

-

If the underlying price does not rise up to the breakeven point, the trader would incur a loss

-

If the underlying price rises beyond the strike price of the short Call, the trader would not be able to any make additional gain

Strategy Suggestions

-

Ensure that the price trajectory of the underlying is moderately bullish

-

Have conviction that the underlying price will trade with a bullish bias within a certain price range

-

When selecting an OTM strike to sell the Call, be realistic. Don’t select a strike that is too high from the current price, unless you are convinced that the underlying can rally up to that strike

-

Similarly, when selecting an OTM strike to sell the Call, don’t select a strike that is too low from the current price, as this would make the overall risk-reward ratio highly unattractive

-

Hence, the strike that is chosen for selling the Call must not only be realistic for the underlying price to rise till there until expiration, but must also be favourable from a risk-reward perspective

-

If the underlying price rises above the strike price of the OTM short Call and if the outlook continues to look bullish, one could consider closing out the existing short Call and either write a new Call with an even higher strike price or just let the long Call run in isolation

-

Ensure that there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Bull Call Spread

| Greek | Value is | Notes |

| Delta | Positive |

Because the strategy involves buying at ATM Call and selling an OTM Call, the overall Delta is positive at initiation. As a result, the position stands to benefit when the underlying price rises, and vice versa. However, unlike a naked Call, the impact of Delta on the overall position is quite less because of the two opposite positions that have been created (long Call and short Call). |

| Gamma | Positive |

At initiation, the position Gamma is positive, causing the position Delta to rise for a given rise in the underlying price, and vice versa. However, once the underlying price rises beyond the breakeven price, the position Gamma becomes negative, causing the position Delta to decrease for a given rise in the underlying price, and vice versa. |

| Vega | Positive |

Vega does not have a material impact on this strategy because the trader is long as well as short a Call. That said, initially when the strategy is entered into, the overall Vega is positive and benefits the position so long as the underlying price is below the breakeven price. Once the underlying price moves above the breakeven price, Vega starts hurting the position. |

| Theta | Negative |

The overall Theta is negative at initiation. Beyond this however, much depends on how the underlying price moves as the time progresses. If the underlying price is below the breakeven price, Theta harms the position; while if the underlying price rises and moves beyond the breakeven price, Theta benefits the position. |

| Rho | Positive |

The overall Rho is positive at initiation. As a result,rising interest rates benefit the position, and vice versa. However, it must be noted that this is the least significant of the Greeks, especially in case of short-dated options. |

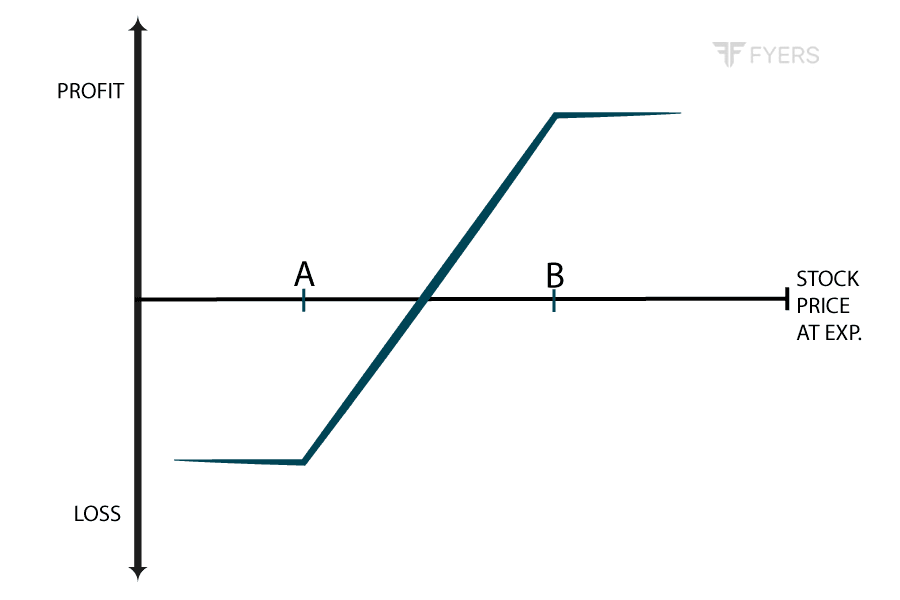

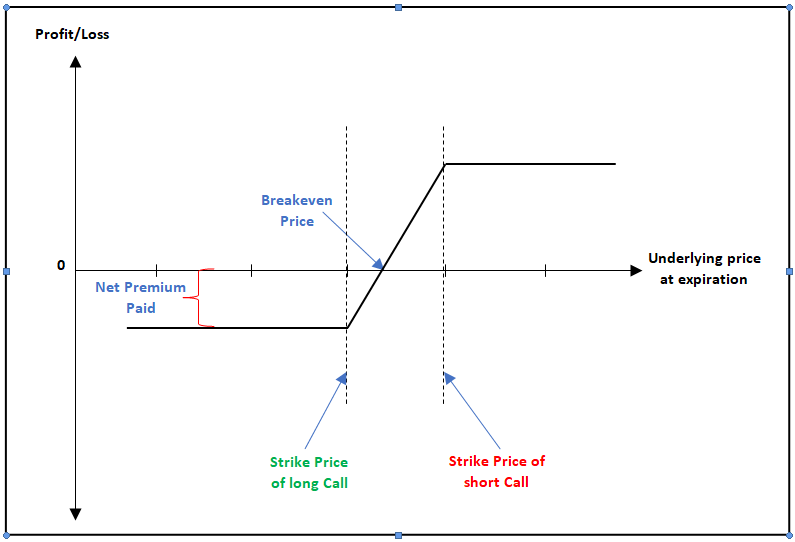

Payoff of Bull Call Spread

The above chart shows the payoff chart for a Bull Call Spread. As we can see, the strategy works only within a certain range. If the underlying price falls below the lower strike price, the strategy attains its maximum loss potential. No matter how lower the underlying price goes below the lower strike price, the amount of loss is fixed. Similarly, if the underlying price rises to the higher strike price, the strategy attains its maximum gain potential. No matter how higher the underlying price rises above the higher strike price, the amount of gain is capped. Meanwhile, the breakeven point of the strategy is calculated as the strike price of the long Call plus the difference between the two premium amounts. This is the point at which the buyer makes no profit, no loss. As long as the underlying price stays below the breakeven point, the buyer is in a loss. Once the underlying rises above the breakeven point, the buyer starts making profit. The sweetest spot of this strategy is achieved when the underlying rises to and trades near the higher strike price.

Example of Bull Call Spread

Let us say that Nifty has just broken its immediate resistance of 8360, which is also confirmed by a bullish signal generated by the RSI and an expansion in volume. Based on this, Mr. ABC feels that the index will head higher in the days ahead. However, he also observes that there is a formidable hurdle up ahead at 8800, which he feels will hold for this expiry. Based on this, ABC decides to enter into a Bull Call Spread strategy, wherein he will buy a NTM 8400 strike Call option and simultaneously sell an OTM 8800 strike Call option. Let us assume that the premium on the lower strike Call is ₹100 and that on the higher strike Call is ₹30. Given that he would be paying a premium of ₹100 and receiving a premium of ₹30, the net debit would amount to ₹70. Given the lot size of 75, the total net debit would amount to ₹5,250. Let us summarize the details below:

-

Strike price of long Call = 8400 CE

-

Strike price of short Call = 8800 CE

-

Long Call premium = ₹100

-

Short Call premium = ₹30

-

Net Debit = ₹70

-

Net Debit (in value terms) = ₹5,250

-

Breakeven price of the strategy = ₹8,470 (8400 + 100 - 30)

Now, let us assume a few scenarios in terms of where Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 7500 | Loss of ₹5,250 | Payoff = [maximum of (7500-8400,0)-100]+[30- maximum of (7500 - 8800, 0). As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 7800 | Loss of ₹5,250 | Payoff = [maximum of (7800-8400,0)-100]+[30- maximum of (7800 - 8800, 0). As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 8100 | Loss of ₹5,250 | Payoff = [maximum of (8100-8400,0)-100]+[30- maximum of (8100 - 8800, 0). As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 8400 | Loss of ₹5,250 | Payoff = [maximum of (8400-8400,0)-100]+[30- maximum of (8400 - 8800, 0). As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 8470 | No profit, No loss | Payoff = [maximum of (8470-8400,0)-100]+[30- maximum of (8470 - 8800, 0).As the underlying price at expiration is equal to the breakeven price, the trader will neither make a profit nor incur a loss |

| 8600 | Profit of ₹9,750 | Payoff = [maximum of (8600-8400,0)-100]+[30- maximum of (8600 - 8800, 0). As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 8800 | Profit of ₹24,750 | Payoff = [maximum of (8800-8400,0)-100]+[30- maximum of (8800 - 8800, 0).As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 9000 | Profit of ₹24,750 | Payoff = [maximum of (9000-8400,0)-100]+[30- maximum of (9000 - 8800, 0).As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 10000 | Profit of ₹24,750 | Payoff = [maximum of (10000-8400,0)-100]+[30- maximum of (10000 - 8800, 0).As the underlying price at expiration is above the breakeven price, the trader will make a gain |

Notice from the above table that the both profits and losses are limited in this strategy. The worst case scenario occurs when the underlying price drops below the lower strike price, in which case the trader would lose the entire net premium that he/she has paid on the strategy. Meanwhile, the best case scenario occurs when the underlying price rises to the higher strike price. At this point, the trader would be earning the maximum possible profit under this strategy. Beyond the higher strike price, no matter how higher the underlying price goes, the trader will not earn a penny more. Hence this strategy must be deployed only when the trader is moderately bullish on the underlying and does not expect it to move much farther beyond the higher strike price. Also notice that for the trader to enter into the profitable zone, the underlying price will have to rise above the long Call strike plus the net debit of the strategy.

BEAR CALL SPREAD

| Strategy Details | |

| Strategy Type | Moderately bearish |

| # of legs | 2 (Long OTM, higher strike Call + Short OTM, lower strike Call) |

| Maximum Reward | Premium of short Call - Premium of long Call |

| Maximum Risk | (Strike price of long Call - Strike price of short Call) - (Premium of short Call - Premium of long Call) |

| Breakeven Price | Strike price of short Call + Premium of short Call - Premium of long Call |

| Payoff Calculation | Payoff of Long Call + Payoff of Short Call |

Explanation of the Strategy

A Bear Call Spread is a two-legged strategy wherein the trader would sell an OTM Call option and simultaneously buy an OTM Call option for the same underlying and same expiration. The Call that is sold will have a lower strike price, while the Call that is purchased will have a higher strike price. Put it in other words, the strike price of the short Call will be below that of the long Call. This a moderately bearish strategy, wherein the trader benefits when the underlying price either consolidates or declines. Unlike a Bull Call Spread which is a net debit strategy, a Bear Call Spread is a net credit strategy. This is because the premium received on shorting the Call is higher than the premium paid on buying the Call. The trader who executes this strategy gets to retain the entire net credit of the strategy as long as the underlying price is trading below the strike price of the short Call. This is one of the reasons why an OTM Call is written, because it gives the trader some leeway between the current market price and the short Call strike price. Meanwhile, once the underlying price rises above the strike price of the short Call, the trader’s net credit received starts reducing until the underlying price reaches the breakeven price of the strategy, which is a point of no profit, no loss. Once the underlying price moves above the breakeven price, the trader starts suffering losses.

Compare this strategy to a naked short Call strategy. In shorting a Call naked, the risk is potentially unlimited because there is no limit to the extent to which the underlying price can rally. By executing a Bear Call Spread, the long Call acts as an insurance to the short Call. This is because if the underlying price rises and crosses the strike price of the long Call, the trader’s losses get capped at that strike. Beyond this, no matter how higher the underlying price rallies, the trader does not incur any more losses. Hence, by paying a small premium, the trader is protecting his/her position against any sharp, adverse price move.

Benefits of the Strategy

-

If used in correct market conditions, the strategy can be a good source of income

-

The strategy achieves its maximum profit potential even if the underlying price does not move

-

Maximum loss in this strategy is capped, no matter how higher the underlying price moves above the breakeven price

-

Depending on your risk-reward expectations, you can adjust the strike prices that you choose for going long and short.

Drawbacks of the Strategy

-

The maximum reward is limited to the extent of the net credit received

-

If the underlying price falls sharply, there would be an opportunity loss

-

The risk-reward profile is unfavourable as risk is usually greater than reward

Strategy Suggestions

-

Ensure that the price trajectory of the underlying is sideways or moderately bearish

-

If you are outrightly bearish on the underlying, then you would be better off by deploying other strategies such as long Put or short futures

-

Have conviction that the underlying price will stay below the strike price of the short Call

-

Select the strikes depending on how much you expect the underlying price to move

-

A general rule to remember is the larger the difference between the two strikes, the larger would be the reward and so would be the risk, and vice versa

-

So, if you want reward over safety, select strikes that are far away from each other, and vice versa

Option Greeks for Bear Call Spread

| Greek | Value is | Notes |

| Delta | Negative |

Because the strategy involves selling an OTM Call with a lower strike and buying anOTM Call with a higher strike, the overall Delta is negative. As a result, the position stands to benefit when the underlying price falls, and vice versa. Delta reaches zero when the underlying price either falls sharply below the lower strike or rises sharply above the higher strike. Meanwhile, Delta is at its maximum negative value when the underlying price is in between the two strikes. |

| Gamma | Negative |

At initiation, the position Gamma is negative, causing the position Delta to decrease (become more negative) for a given rise in the underlying price, and vice versa. However, once the underlying price rises beyond the breakeven price, the position Gamma becomes positive, causing the position Delta to increase (become less negative) for a given rise in the underlying price, and vice versa. Meanwhile, when the position is deep ITM or deep OTM, Gamma approaches zero. |

| Vega | Negative |

When the strategy is initiated, the overall Vega is negative, meaning rising volatility hurts the position, and vice versa. Once the underlying price rises above the midpoint of the two strikes, the overall Vega becomes positive, meaning rising volatility helps the position, and vice versa. Meanwhile, Vega reaches zero when the underlying price either falls sharply below the lower strike or rises sharply above the higher strike. |

| Theta | Positive |

The overall Theta is positive at initiation, meaning time decay benefits the position as long as the underlying price is below the breakeven price.Once the underlying price rises and moves beyond the breakeven price, Theta becomes negative, meaning time decay starts hurting the position. |

| Rho | Negative |

The overall Rho is negative at initiation. As a result, rising interest rates hurt the position, and vice versa. However, it must be noted that this is the least significant of the Greeks, especially in case of short-dated options. |

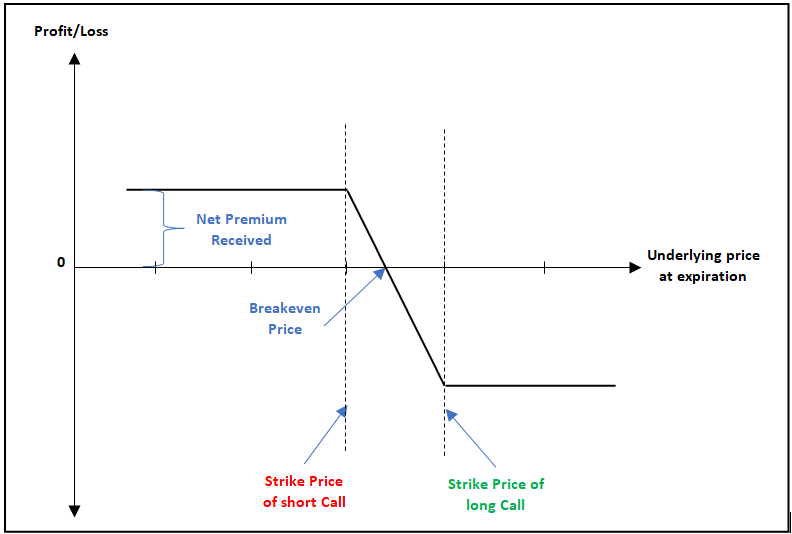

Payoff of Bear Call Spread

The above is the payoff chart of a Bear Call Spread. Usually, this strategy is traded by selling an OTM, lower strike Call and buying an OTM, higher strike Call. As a result, this is an income strategy, wherein the trader receives a net credit into his/her trading account. Notice in the chart that the maximum gain under this strategy is limited to the extent of the net credit received. The trader is in a profitable position as long as the underlying price is trading below the breakeven price of the strategy. Once the underlying price crosses the breakeven price, the trader starts incurring losses. Unlike a naked short Call however, losses are not unlimited. The Call that has been bought at higher strike acts as a ceiling, beyond which losses will not increase. Keep in mind that this strategy must be deployed only when your outlook on the underlying is range bound to moderately bearish. If you expect the underlying to fall sharply, you have to look out for other bearish strategies where the profit potential is unlimited, such as a long Put.

Example of Bear Call Spread

Let us assume that Bank Nifty has broken below a minor support of 20000 and is currently trading at 19850. Mr. ABC is of the opinion that the index will head slightly lower in the days ahead towards its key support level of 19000. Based on this, ABC decides to enter into a Bear Call Spread strategy, wherein he will sell anOTM 20000 strike Call option and simultaneously buy an OTM 21000 strike Call option. Let us assume that the premium on the lower strike Call is ₹200 and that on the higher strike Call is ₹140. Given that he would be receiving a premium of ₹200 and paying a premium of ₹140, the net credit into his trading account would amount to ₹60. Given the lot size of 20, the total net credit would amount to ₹1,200. Let us summarize the details below:

-

Strike price of short Call = 20000 CE

-

Strike price of long Call = 21000 CE

-

Short Call premium = ₹200

-

Long Call premium = ₹140

-

Net Credit = ₹60

-

Net Credit (in value terms) = ₹1,200

-

Breakeven price of the strategy = ₹20,060 (20000 + 200 - 140)

Now, let us assume a few scenarios in terms of where Bank Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 24000 | Loss of ₹18,800 | Payoff = [maximum of (24000-21000,0)-140]+[200- maximum of (24000 - 20000, 0). As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 22000 | Loss of ₹18,800 | Payoff = [maximum of (22000-21000,0)-140]+[200- maximum of (22000 - 20000, 0). As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 21000 | Loss of ₹18,800 | Payoff = [maximum of (21000-21000,0)-140]+[200- maximum of (21000 - 20000, 0). As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 20500 | Loss of ₹18,800 | Payoff = [maximum of (20500-21000,0)-140]+[200- maximum of (20500 - 20000, 0). As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 20060 | No profit, No loss | Payoff = [maximum of (20060-21000,0)-140]+[200- maximum of (20060 - 20000, 0). As the underlying price at expiration is equal to the breakeven price, the trader will neither make a profit nor incur a loss |

| 20030 | Profit of ₹600 | Payoff = [maximum of (20030-21000,0)-140]+[200- maximum of (20030 - 20000, 0). As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 20000 | Profit of ₹1,200 | Payoff = [maximum of (20000-21000,0)-140]+[200- maximum of (20000 - 20000, 0). As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 19500 | Profit of ₹1,200 | Payoff = [maximum of (19500-21000,0)-140]+[200- maximum of (19500 - 20000, 0). As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 18000 | Profit of ₹1,200 | Payoff = [maximum of (18000-21000,0)-140]+[200- maximum of (18000 - 20000, 0). As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 17000 | Profit of ₹1,200 | Payoff = [maximum of (17000-21000,0)-140]+[200- maximum of (17000 - 20000, 0). As the underlying price at expiration is below the breakeven price, the trader will make a gain |

It can be seen from above that both maximum profit and maximum loss are limited under the Bear Call Spread strategy. Losses get capped once the underlying price rises to the higher strike price. No matter how higher the underlying price moves beyond the higher strike price, the trader will not incur any additional losses. Similarly, profits are capped at the lower strike price. No matter how lower the underlying price declines below the lower strike price, the trader does not earn anything more. The sweetest spot is when the underlying price stays below the lower strike price but does not fall sharply below it. This is because in case the underlying price drops sharply, there would be an opportunity loss as the trader will not earn a penny more beyond the net credit that he/she has received.

Next Chapter

Comments & Discussions in

FYERS Community