BULL CALL LADDER

| Strategy Details | |

| Strategy Type | Moderately Bullish when initiated, but bearish after a certain point |

| # of legs | 3 (Long ATM Call + Short OTM, Middle Strike Call + Short OTM, Higher Strike Call) |

| Maximum Reward | Middle Strike price - Lower Strike price - Net Premium paid |

| Maximum Downside Risk | Limited to the extent of Net Premium Paid, as long as underlying price is below the lower strike price |

| Maximum Upside Risk | Unlimited, once the underlying price crosses above the upper breakeven price |

| Lower Breakeven Price | Lower Strike price + Net Premium paid |

| Upper Breakeven Price | Higher Strike price + Middle Strike price - Lower Strike price - Net Premium paid |

| Payoff Calculation | Payoff of Long Call+ Payoff of middle Short Call + Payoff of higher Short Call |

Explanation of the Strategy

A Bull Call Ladder is an extension of a Bull Call Spread. Recollect that in a Bull Call Spread, the trader buys an ATM Call and sells an OTM Call. In a Bull Call Ladder, the trader would buy an ATM Call and sell two OTM Calls having different strike prices. So, a total of three legs would be created under this strategy: a lower leg, representing the long ATM Call; a middle leg, representing the short OTM Call; and a higher leg, representing the second short OTM Call. Before discussing more about this strategy, let us first talk about the breakeven point. A Bull Call Ladder has two breakeven points: one lower and one upper. The lower breakeven point is the point above which the underlying price will have to rise for the strategy to become profitable. Until then, the strategy remains unprofitable. Meanwhile, the upper breakeven point is the point below which the underlying price will have to remain for the strategy to remain profitable. If the underlying price moves above the upper breakeven point, the strategy becomes unprofitable. So, as we can see, the strategy is profitable when the underlying price is in between the two breakeven points and is unprofitable when the underlying price is either below the lower breakeven point or above the upper breakeven point.

Compared to a Bull Call Spread, a Bull Call Ladder will further reduce the overall cost as well as the lower breakeven pointof the strategy. However, these benefits come at a cost. And the cost is that the risk of the strategy amplifies. Remember, in a Bull Call Spread, the maximum risk is limited to the extent of the net premium paid. In a Bull Call Ladder however, there are two types of maximum risk: maximum downside risk and maximum upside risk. The maximum downside risk occurs when the underlying price falls to or below the lower strike price, in which case the trader loses the entire net premium amount. And the maximum upside risk occurs when the underlying price rises above the upper breakeven price, in which case the losses could get potentially unlimited as the trader would have two short Call positions that are open against just one long Call. Hence, the trader who has executed this strategy must pay careful attention when the underlying price rises above the higher strike price. If it sustains above the higher strike price, the trader must consider either modifying the strategy to make it more bullish or exiting the position altogether, if necessary.

A Bull Call Ladder is a moderately bullish strategy. The trader would benefit when the underlying price rises to the middle strike, which will enable him/her to maximize the profit potential of the strategy. Even a move beyond the middle strike would enable the trader to earn maximum profits, provided the underlying price does not rise above the higher strike price. Once the underlying price rises above the higher strike price however, the strategy becomes bearish and the trader’s profit potential starts reducing. So, this strategy is moderately bullish as long as the underlying price is below the higher strike price, and bearish once the underlying price crosses the higher strike price. Because a Bull Call Ladder is a limited profit, unlimited loss type of option strategy, it must be deployed by intermediate to advanced option traders and is not suitable for beginners.

Meanwhile, we have said that a Bull Call Ladder is a net debit strategy. But because two options are sold instead of one, a question that could arise in one’s mind is can this strategy be a net credit strategy. The answer is yes, it is possible. This can happen when the two strikes that are chosen for selling Calls are closer to the strike that is chosen for buying a Call. However, executing such a strategy has risks because the upper Breakeven point will be closer, which could cause the position to lose money quickly in case there is a sudden rise in the underlying price that takes it above the upper breakeven price. Hence, more often than not, this strategy is a net debit strategy than a net credit strategy.

Benefits of the Strategy

-

Reduces the overall cost of the strategy even more than a Bull Call Spread does

-

Reduces the lower breakeven point of the strategy even more than a Bull Call Spread does

-

The two strikes for shorting the Calls can be chosen depending upon one’s trading preferences

Drawbacks of the Strategy

-

If the underlying rises above the upper breakeven price, losses could be huge

-

Because this strategy involves selling two options, it will require a greater margin in your trading account

-

As long as the underlying price is below the lower breakeven point, Theta will work against the trader

Strategy Suggestions

-

Ensure that the trend is moderately bullish, that there is a clear support at a lower level which you feel will hold, and that there is a clear resistance at a higher level which you feel won’t break

-

Ensure to maintain the ratio of lots that are transacted at initiation. In other words, for every X number of Calls you buy, you also sell X number of Calls with middle strike and X number of Calls with higher strike

-

When choosing the two strikes for selling the Calls, don’t just randomly select any strike. Look for areas of strong resistance, or whatever factor you feel like, and select strikes accordingly

-

Remember, you want the underlying price to rise to at least the middle strike by expiration, so as to earn maximum profit on the strategy

-

The difference between the lower strike and the two higher strikes will be a trade-off between net cost of the strategy and the reward

-

The larger the difference between the lower strike and the two higher strikes, the larger would be the net cost, downside risk, reward, and the two breakeven points, and vice versa

-

If the underlying price rises sharply and moves above the upper breakeven price, consider closing out the position if you feel the upside will continue or you are unwilling to assume further risk

-

Keep sufficient spread between the lower strike and the higher strike to account for any unexpected sudden surge in the underlying price

-

Because the upside risk is unlimited, see that there is not too much time left in the life of the option contract, so as to give the trade less time to go wrong

-

Ensure that there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Bull Call Ladder

At the time of strategy initiation, the sign of Greeks can vary depending upon the distance between the strike price of a long Call (lower strike) and those of the two short Calls (middle and higher strike). Hence, we shall be talking about Greeks in general without discussing about the sign of each Greek at initiation.

| Greek | Notes |

| Delta |

Because this is a bullish strategy at initiation, Delta is initially positive and thereby benefits the position when the underlying price rises, and vice versa. However, Delta turns negative as the underlying price continues rising and inches towards the strikes of the short Calls. As a result, rising underlying price eventually starts hurting the option position, and vice versa. |

| Gamma |

Gamma peaks out at the lower strike, lifting the Delta as the underlying price rises, and vice versa. Iteventually turns negativeas the underlying moves towards the middle strike, by which time rising prices start dragging the Delta into negative zone. Gamma bottoms out at the higher strike, dragging the Delta further into negative if the underlying price continues rises. |

| Vega |

When the underlying price is below the lower breakeven point or above the upper breakeven point, Vega is positive and hence, rising volatility is helpful to the position, and vice versa. On the other hand, when the underlying price is between the two breakeven points, Vega is negative and hence, rising volatility hurts the position, and vice versa. |

| Theta |

When the underlying price is below the lower breakeven point or above the upper breakeven point, Theta is negative because of which time decay hurts the position. On the other hand, when the underlying price is between the two breakeven points, Theta is positive because of which time decay benefits the position. |

| Rho |

Rising interest rates can benefit the position initially, and vice versa. However, once the underlying price approaches the higher strike price, rising interest rates can hurt the position, and vice versa. That said, this is the least significant of the Greeks, especially in case of short-dated options. |

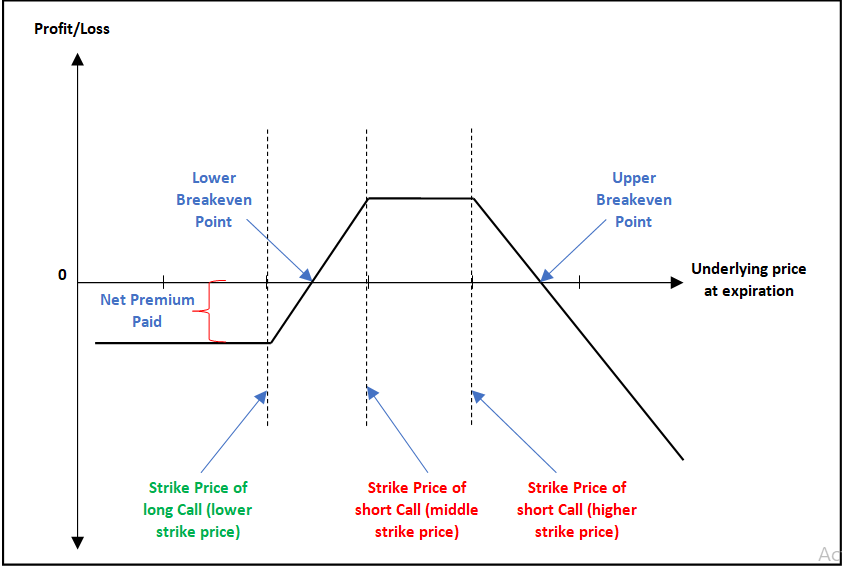

Payoff of Bull Call Ladder

The chart below shows the payoff chart of a Bull Call Ladder. Observe the three strike prices and the two breakeven points of this strategy. The lower strike is the strike price of the long Call, the middle strike is the strike price of the first short Call, and the higher strike is the strike price of the second short Call. Meanwhile, the lower breakeven point is the point beyond which the underlying price will have to rise for the position to start making money. Until then, the trader will be incurring a loss. On the other hand, the upper breakeven point is the point beyond which the trader will start incurring losses again, which can get potentially catastrophic the higher the underlying price rises above it.

Notice that the position is profitable in between the two breakeven points and unprofitable beyond them. The maximum profit of the strategy tends to occur when the underlying price is between the middle and the higher strike price. Hence, this is the sweetest spot position of this strategy. The trader who executes this strategy would want the underlying price to stay inside this range. Meanwhile, if the underlying price continues rising and crosses the higher strike, the profitability of the strategy will start reducing. Beyond the upper breakeven point, the trader will start incurring losses. Hence, if the underlying price crosses the upper breakeven point, the trader should consider exiting the position altogether, if necessary, or modify the position to make it more bullish.

Example of Bull Call Ladder

Let us say that Mr. ABC, based on his observations on Nifty, has decided to initiate a Bull Call Ladder strategy, wherein he will buy 1 ATM 8100 Call at ₹470,sell 1 OTM 8600 Call at ₹230 and another OTM 8800 Call at ₹170. Let us summarize the details of the strategy below:

-

Strike price of long Call = 8100

-

Strike price of middle short Call = 8600

-

Strike price of higher short Call = 8800

-

Long Call premium (lower strike) = ₹470

-

Short Call premium (middle strike) = ₹230

-

Short Call premium (higher strike) = ₹170

-

Net Debit = ₹70 (470 - 230 - 170)

-

Net Debit (in value terms) = ₹5,250 (70 * 75)

-

Lower breakeven point = 8170 (8100+70)

-

Upper breakeven point = 9230 (8800 + 8600 - 8100 - 70)

-

Maximum downside risk = ₹5,250

-

Maximum upside risk = unlimited

-

Maximum Potential Profit = ₹32,250 ((8600 - 8100 - 70) * 75)

Now, let us assume a few scenarios in terms of where Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 6000 | Loss of ₹5,250 | Payoff = [maximum of (6000-8100,0)-470]+[230- maximum of (6000-8600,0)] + [170- maximum of (6000-8800,0)]. As the underlying price at expiration is below the lower breakeven price, the trader will incur a loss |

| 7000 | Loss of ₹5,250 | Payoff = [maximum of (7000-8100,0)-470]+[230- maximum of (7000-8600,0)] + [170- maximum of (7000-8800,0)]. As the underlying price at expiration is below the lower breakeven price, the trader will incur a loss |

| 8000 | Loss of ₹5,250 | Payoff = [maximum of (8000-8100,0)-470]+[230- maximum of (8000-8600,0)] + [170- maximum of (8000-8800,0)]. As the underlying price at expiration is below the lower breakeven price, the trader will incur a loss |

| 8100 | Loss of ₹5,250 | Payoff = [maximum of (8100-8100,0)-470]+[230- maximum of (8100-8600,0)] + [170- maximum of (8100-8800,0)]. As the underlying price at expiration is below the lower breakeven price, the trader will incur a loss |

| 8150 | Loss of ₹1,500 | Payoff = [maximum of (8150-8100,0)-470]+[230- maximum of (8150-8600,0)] + [170- maximum of (8150-8800,0)]. As the underlying price at expiration is below the lower breakeven price, the trader will incur a loss |

| 8170 | No profit, No loss | Payoff = [maximum of (8170-8100,0)-470]+[230- maximum of (8170-8600,0)] + [170- maximum of (8170-8800,0)]. As the underlying price at expiration is at the lower breakeven price, the trader will neither profit nor incur a loss |

| 8500 | Profit of ₹24,750 | Payoff = [maximum of (8500-8100,0)-470]+[230- maximum of (8500-8600,0)] + [170- maximum of (8500-8800,0)]. As the underlying price at expiration is above the lower breakeven price and below the upper breakeven price, the trader will make a profit |

| 8600 | Profit of ₹32,250 | Payoff = [maximum of (8600-8100,0)-470]+[230- maximum of (8600-8600,0)] + [170- maximum of (8600-8800,0)]. As the underlying price at expiration is above the lower breakeven price and below the upper breakeven price, the trader will make a profit |

| 8800 | Profit of ₹32,250 | Payoff = [maximum of (8800-8100,0)-470]+[230- maximum of (8800-8600,0)] + [170- maximum of (8800-8800,0)]. As the underlying price at expiration is above the lower breakeven price and below the upper breakeven price, the trader will make a profit |

| 9000 | Profit of ₹17,250 | Payoff = [maximum of (9000-8100,0)-470]+[230- maximum of (9000-8600,0)] + [170- maximum of (9000-8800,0)]. As the underlying price at expiration is above the lower breakeven price and below the upper breakeven price, the trader will make a profit |

| 9230 | No profit, No loss | Payoff = [maximum of (9230-8100,0)-470]+[230- maximum of (9230-8600,0)] + [170- maximum of (9230-8800,0)]. As the underlying price at expiration is at the upper breakeven price, the trader will neither profit nor incur a loss |

| 10000 | Loss of ₹57,750 | Payoff = [maximum of (10000-8100,0)-470]+[230- maximum of (10000-8600,0)] + [170- maximum of (10000-8800,0)]. As the underlying price at expiration is above the upper breakeven price, the trader will incur a loss |

| 12000 | Loss of ₹207,750 | Payoff = [maximum of (12000-8100,0)-470]+[230- maximum of (12000-8600,0)] + [170- maximum of (12000-8800,0)]. As the underlying price at expiration is above the upper breakeven price, the trader will incur a loss |

Notice in the above table that as long as the underlying price is below the lower breakeven price, the trader incurs a loss, which is limited to the extent of the net debit of the strategy. Also observe that the trader starts to gain once the underlying price rises above the lower breakeven price, with the profit potential stretching to its maximum when the underlying price is in between the middle and the higher strike price. Once the underlying price rises above the higher strike price, the trader’s profitability starts reducing until the price reaches the upper breakeven point. Observe that beyond this point, the trader starts suffering losses again, which can get catastrophic, the higher the underlying price moves beyond the upper breakeven price.

BEAR CALL LADDER

| Strategy Details | |

| Strategy Type | Sideways to moderately Bearish when initiated, but bullish after a certain point |

| # of legs | 3 (Shortslightly OTMCall + Long OTM, Middle Strike Call + Long OTM, Higher Strike Call) |

| Maximum Downside Reward | Net premium received |

| Maximum Upside Reward | Potentially unlimited, once the underlying price crosses the upper breakeven point |

| Maximum Risk | Limited to the extent of middle strike price - lower strike price - Net premium received |

| Lower Breakeven Price | Lower Strike price + Net Premium received |

| Upper Breakeven Price | Higher Strike price + Middle Strike price - Lower Strike price - Net Premium received |

| Payoff Calculation | Payoff of short Call + Payoff of middle,long Call + Payoff of higher,long Call |

In the above equations, we have assumed the strategy as being a net credit strategy. However, in reality, a Bear Call Ladder can be either a net debit strategy or a net credit strategy, depending on the strikes that have been chosen.

Explanation of the Strategy

A Bear Call Ladder is an extension of a Bear Call Spread, but with one additional leg that is added into the equation. Remember that in a Bear Call Spread, the trader sells a slightly OTM Call and buys a Call that has an even higher strike price. Meanwhile, in a Bear Call Ladder, the trader would sell a slightly OTM Call, buy a Call that has a higher strike, and buy another Call that has an even higher strike. So, in a Bear Call Ladder, there will be a total of 3 legs at three different strikes - one short at the lowest strike and two long at the middle and the higher strike. While the short Call will have the highest premium of the three, the combined premium of the two long Calls relative to the short Call determines whether this is a net debit or a net credit strategy. For the rest of our discussion, we will assume this to be a net credit strategy.

At the time of initiation, this is a moderately bearish strategy wherein the trader benefits as long as the underlying price stays below the lower breakeven point. In this case, the trader gets to keep the net premium that he/she has received upfront. Hence, at initiation, this strategy can be thought of as a moderately bearish strategy that benefits when the underlying price either stays sideways or declines modestly.Meanwhile, this strategy has two breakeven points: lower and upper. The trader suffers a loss when the underlying price is between the two breakeven points. Maximum loss under this strategy occurs when the underlying price is between the middle strike and the higher strike.

One might think that the sweetest spot of this strategy is when the underlying price is below the lower strike price. In reality however, the sweetest spot occurs when the underlying price rises above the upper breakeven point. This is because beyond the upper breakeven point, the profits are unlimited. The higher the underlying price rises above the upper breakeven price, the higher would be the trader’s profitability. Hence, a trader would either prefer the underlying price staying below the lower strike as this will enable him/her to keep the net premium or prefer the underlying price rising sharply to explode past the upper breakeven point to maximise the profit potential of the strategy.

Benefits of the Strategy

-

Potential for unlimited profit if the underlying price rises sharply

-

Potential to retain the net premium received if the underlying price stays below the lower strike

-

The strategy has limited risk

Drawbacks of the Strategy

-

If the underlying price stays between the two breakeven points, the trader will suffer a loss

-

If the underlying price stays between the middle and the higher strike, the trader will suffer maximum loss that is possible under this strategy

-

Sometimes, the strategy could be a net debit strategy

Strategy Suggestions

-

Ensure to maintain the ratio of lots that are transacted at initiation. In other words, for every X number of Calls you sell, you also buy X number of Calls with middle strike and X number of Calls with higher strike.

-

When choosing the two strikes for buying the Calls, don’t just randomly select any strike. Remember, if the underlying price rallies, you would want it to surge past the upper breakeven point. Hence, choose the long Call strikes accordingly.

-

The difference between the lower strike and the two higher strikes will be a trade-off between net premium received and risk

-

The larger the difference between the lower strike and the two higher strikes, the larger would be the net premium received but so would be the risk, and vice versa

-

Because this strategy involves buying two Calls and attains its maximum profit potential once the underlying crosses the upper breakeven point, ensure that there is sufficient time left in the life of the option contract, for the strategy to work in your favour

-

Ensure that there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Bear Call Ladder

At the time of strategy initiation, the sign of Greeks can vary depending upon the distance between the strike price of a short Call (lower strike) and those of the two long Calls (middle and higher strike). Hence, we shall be talking about Greeks in general without discussing about the sign of each Greek at initiation.

| Greek | Notes |

| Delta |

Because this strategy is bearish at the time of initiation, Delta is initially negative and benefits the option position when the underlying price falls, and vice versa. However, Delta turns positiveonce the underlying price moves upwards and towards the strikes of the long Calls. When this happens, rising underlying price benefits the option position, and vice versa. |

| Gamma |

Gamma is usually positive for this strategy, lifting the Delta as the underlying price rises, and vice versa. Gamma peaks out at the higher strike and then starts to taper off, in turn reducing the rate of Delta’s ascent, which is usually at its steepest around the higher strike. |

| Vega |

When the underlying price is below the lower breakeven point or above the upper breakeven point, Vega is negative, because of which rising volatility hurts the position, and vice versa. On the other hand, when the underlying price is between the two breakeven points, Vega is positive, because of which rising volatility benefits the position, and vice versa. |

| Theta |

When the underlying price is below the lower breakeven point or above the upper breakeven point, Theta is positive, because of which time decay benefits the position. On the other hand, when the underlying price is in between the two breakeven points, Theta is negative, because of which time decay hurts the position. |

| Rho |

Rising interest rates can hurt the position initially, and vice versa. However, once the underlying price approaches the higher strike price, rising interest rates start benefiting the position, and vice versa. That said, this is the least significant of the Greeks, especially in case of short-dated options. |

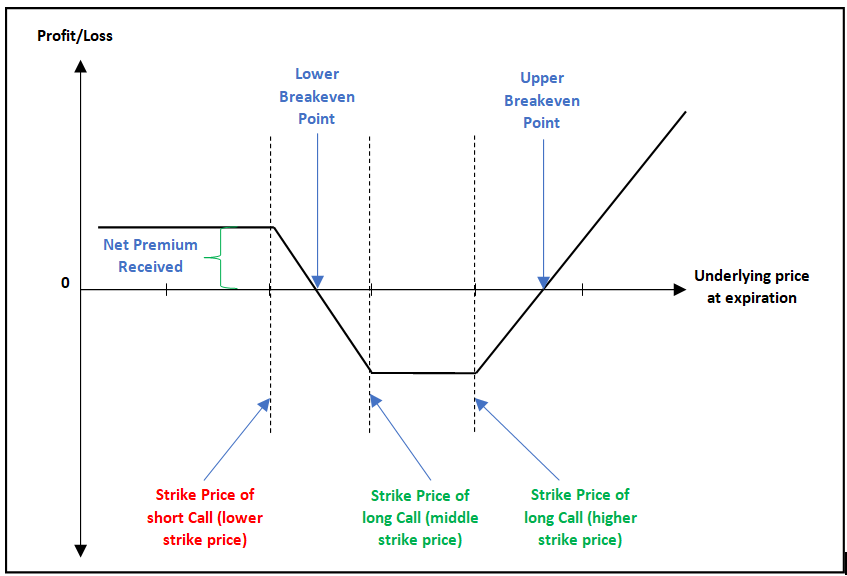

Payoff of Bear Call Ladder

There are two ways in which a Bear Call Ladder can make money for the trader. First is when the underlying price stays below the lower strike price, which enables the trader to retain the entire net premium. The position is also profitable in case the underlying price rises above the lower strike price but is below the lower breakeven point. While this reduces the trader’s profitability, it nonetheless enables him/her to retain some part of the net premium. Second is when the underlying price surges above the upper breakeven point. This is the sweetest position that a trader could be in because, beyond the upper breakeven point, profits are unlimited. In between these two extremes, i.e. in between the lower breakeven point and the upper breakeven point, the trader incurs a loss, which reaches its maximum when the underlying price is between the middle and the higher strike.

Example of Bear Call Ladder

Let us say that Mr. ABC has analysed the chart of Bank Nifty and has decided to execute a Bear Call Ladder option strategy. Because of elevated volatility, Mr. ABC has also decided to buy Calls that are relatively far OTM. Under this strategy, Mr. ABC will sell one 17200 Call at ₹1,400, buy one 18500 Call at ₹750 and another 19000 Call at ₹575. Let us summarize the details of the strategy below:

-

Strike price of shortCall = 17200

-

Strike price of middle longCall = 18500

-

Strike price of higher longCall = 19000

-

ShortCall premium (lower strike) = ₹1,400

-

Long Call premium (middle strike) = ₹750

-

Long Call premium (higher strike) = ₹575

-

Net Credit = ₹75 (1400 - 750 - 575)

-

Net Credit (in value terms) = ₹1,500 (75 * 20)

-

Lower breakeven point = 17275 (17200 + 75)

-

Upper breakeven point = 20225 (19000 + 18500 - 17200 - 75)

-

Maximum downside Reward = ₹1,500

-

Maximum upside Reward = unlimited

-

Maximum Risk = ₹24,500 ((18500 - 17200 - 75) * 20)

Now, let us assume a few scenarios in terms of where Bank Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 15000 | Profit of ₹1,500 | Payoff = [1400-maximum of (15000-17200,0)]+[maximum of (15000-18500,0)-750] + [maximum of (15000-19000,0)-575]. As the underlying price at expiration is below the lower breakeven price, the trader will earn a profit |

| 16000 | Profit of ₹1,500 | Payoff = [1400-maximum of (16000-17200,0)]+[maximum of (16000-18500,0)-750] + [maximum of (16000-19000,0)-575]. As the underlying price at expiration is below the lower breakeven price, the trader will earn a profit |

| 17200 | Profit of ₹1,500 | Payoff = [1400-maximum of (17200-17200,0)]+[maximum of (17200-18500,0)-750] + [maximum of (17200-19000,0)-575]. As the underlying price at expiration is below the lower breakeven price, the trader will earn a profit |

| 17250 | Profit of ₹500 | Payoff = [1400-maximum of (17250-17200,0)]+[maximum of (17250-18500,0)-750] + [maximum of (17250-19000,0)-575]. As the underlying price at expiration is below the lower breakeven price, the trader will earn a profit |

| 17275 | No profit, No loss | Payoff = [1400-maximum of (17275-17200,0)]+[maximum of (17275-18500,0)-750] + [maximum of (17275-19000,0)-575]. As the underlying price at expiration is at the lower breakeven price, the trader will neither profit nor incur loss |

| 18000 | Loss of ₹14,500 | Payoff = [1400-maximum of (18000-17200,0)]+[maximum of (18000-18500,0)-750] + [maximum of (18000-19000,0)-575]. As the underlying price at expiration is between the lower and upper breakeven price, the trader will incur a loss |

| 18500 | Loss of ₹24,500 | Payoff = [1400-maximum of (18500-17200,0)]+[maximum of (18500-18500,0)-750] + [maximum of (18500-19000,0)-575]. As the underlying price at expiration is between the lower and upper breakeven price, the trader will incur a loss |

| 19000 | Loss of ₹24,500 | Payoff = [1400-maximum of (19000-17200,0)]+[maximum of (19000-18500,0)-750] + [maximum of (19000-19000,0)-575]. As the underlying price at expiration is between the lower and upper breakeven price, the trader will incur a loss |

| 20000 | Loss of ₹4,500 | Payoff = [1400-maximum of (20000-17200,0)]+[maximum of (20000-18500,0)-750] + [maximum of (20000-19000,0)-575]. As the underlying price at expiration is between the lower and upper breakeven price, the trader will incur a loss |

| 20225 | No profit, No loss | Payoff = [1400-maximum of (20225-17200,0)]+[maximum of (20225-18500,0)-750] + [maximum of (20225-19000,0)-575]. As the underlying price at expiration is at the upper breakeven price, the trader will neither profit nor incur loss |

| 21000 | Profit of ₹15,500 | Payoff = [1400-maximum of (21000-17200,0)]+[maximum of (21000-18500,0)-750] + [maximum of (21000-19000,0)-575]. As the underlying price at expiration is above the upper breakeven price, the trader will earn a profit |

| 23000 | Profit of ₹55,500 | Payoff = [1400-maximum of (23000-17200,0)]+[maximum of (23000-18500,0)-750] + [maximum of (23000-19000,0)-575]. As the underlying price at expiration is above the upper breakeven price, the trader will earn a profit |

| 25000 | Profit of ₹95,500 | Payoff = [1400-maximum of (25000-17200,0)]+[maximum of (25000-18500,0)-750] + [maximum of (25000-19000,0)-575]. As the underlying price at expiration is above the upper breakeven price, the trader will earn a profit |

Notice that in a Bear Call Ladder, profits occur when the underlying price is at an extreme. That is, when the underlying price is either below the lower breakeven price of the strategy or above the upper breakeven price. However, notice the extent of the profits for both the zones and compare it to the maximum risk involved in the strategy. From the example, it can be seen that the risk-reward ratio is highly unfavourable when comparing maximum downside profit (₹1,500) to the maximum risk (₹24,500). Hence, for the given set of information in the example above, it is highly unlikely that the trader would initiate this strategy with the primary objective of earning the maximum downside profit. Instead, the trader would by all means want the underlying price to surge past the upper breakeven point, as this would make the risk-reward ratio highly attractive. For instance, note in the example above that if Bank Nifty were to rally to 25000, the trader would make a profit of ₹95,500, which is nearly four times the maximum risk. Hence, the primary objective of this strategy is usually capital appreciation, which occurs when the underlying price surges above the upper breakeven price. Meanwhile, also observe that in between the two breakeven zones, the trader would suffer a loss, which maximizes when the underlying price is between the middle and the higher strike.

Next Chapter

Comments & Discussions in

FYERS Community

Santosh Kumar Panda commented on May 13th, 2020 at 3:01 PM

Sir please add this strategy in Fyers One platform.

Shriram commented on May 14th, 2020 at 8:31 PM

Hi Santosh, we shall look into this

Prasanth P commented on May 14th, 2020 at 8:10 AM

SIR

PLEASE SEND STRATEGIES TO MY EMAIL

Shriram commented on May 14th, 2020 at 8:32 PM

Hi Prasanth, at present, we have the strategies on our website only.

shashanka commented on July 11th, 2020 at 10:00 AM

hello Tejas,

Thanks for all the effort.

Regards,

Shashanka

Abhishek Chinchalkar commented on July 11th, 2020 at 5:22 PM

Hi Shashanka, thank you for the valuable feedback!