BEAR PUT SPREAD

| Strategy Details | |

| Strategy Type | Moderately bearish |

| # of legs | 2 (Long ATM Put + Short OTM Put) |

| Maximum Reward | (Strike price of longPut - Strike price of short Put) - (Premium of long Put - Premium of short Put) |

| Maximum Risk | Premium of long Put - Premium of short Put |

| Breakeven Price | Strike price of long Put-(Premium of long Put- Premium of short Put) |

| Payoff Calculation | Payoff of Long Put+ Payoff of Short Put |

Explanation of the Strategy

A Bear Put Spread is an option strategy wherein the trader would buy an ATM or slightly OTM Put option and simultaneously sell an OTM Put option on the same underlying instrument and having the same expiration. Because this strategy involves buying a higher strike Put and selling a lower strike Put, this is a moderately bearish strategy. The lower strike Put option that is sold reduces the overall cost of the transaction, but this comes at a price: the maximum profit gets capped at the lower strike price. Compare this strategy to a naked long Put. An advantage of Bear Put Spread over a naked long Put is that the former costs less. On the other side, a disadvantage of Bear Put Spread over a naked long Put is that the former limits the profit potential at the lower strike while the latter does not restrict the profit potential. Hence, whether to initiate a Bear Put Spread or a naked long Put depends completely on the view as well as on the risk profile of the trader.

This strategy not only has a limited profit potential, but it also has a limited loss potential. The maximum that the trader stands to lose is the net premium that he/she has paid on this strategy. This occurs when the underlying price trades at or above the higher strike price. So, while the lower strike restricts the profit potential, the higher strike restricts the loss potential. In between these two is the breakeven price, which is the point of no profit and no loss. The position is profitable when the underlying price is below the breakeven price and loss-making when the underlying price is above the breakeven price.

Benefits of the Strategy

-

Maximum loss is limited to the extent of net premium paid

-

Shorting an OTM Put reduces the overall cost of the strategy

-

The breakeven point of this strategy is smaller as compared to that of a naked long Put.

Drawbacks of the Strategy

-

Put that is sold at the lower strike limits the maximum profit that can be earned

-

Because this is a net debit strategy, the trader will lose money even if the underlying consolidates

-

If the underlying price is above the breakeven price as expiration approaches, Theta would work against the trader

Strategy Suggestions

-

Ensure that price of the underlying is trending lower and is below a resistance level that looks difficult to crack in the near-term

-

Ensure that the options you are transacting are not closer to expiry and there is decent time left for the strategy to work out in your favour

-

While the strike price of the long Put will be either ATM or slightly OTM, be realistic when selecting the strike price of the short Put

-

Remember, you would want the underlying price to drop to the lower strike price, in order to maximize the profit potential of the strategy

-

Remember that the difference between the two strikes will be a trade off between risk/reward and the net cost of the strategy

-

If the underlying price declines to the lower strike price and if the outlook continues to look bearish, one could consider closing out the existing short Put and either write a new Put at an even lower strike or just let the long Put run in isolation

-

Ensure that there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Bear Put Spread

| Greek | Value is | Notes |

| Delta | Negative |

The overall Delta is negative at initiation. As a result, the position stands to benefit when the underlying price falls, and vice versa. |

| Gamma | Positive |

At initiation, the position Gamma is positive, causing the position Delta to rise (i.e. become less negative) as the underlying price rises, and vice versa. However, when the underlying price isbelow the breakeven price, the position Gamma is negative, which causes the position Delta to fall (i.e. become more negative) for a given rise in the underlying price, and vice versa. |

| Vega | Positive |

At initiation,the overall Vega is positive, meaning volatilityhelps the position as long as the underlying price is above the breakeven price. Once the underlying price moves below the breakeven price, Vega turns negative, meaning volatility will start hurting the position. |

| Theta | Negative |

The overall Theta is negative at initiation, meaning time decay hurts the position. However, when the underlying price is below the breakeven price, Theta is positive, meaning time decay benefits the position. |

| Rho | Negative |

The overall Rho is negative at initiation. As a result, rising interest rates hurt the position, and vice versa. However, it must be noted that this is the least significant of the Greeks, especially in case of short-dated options. |

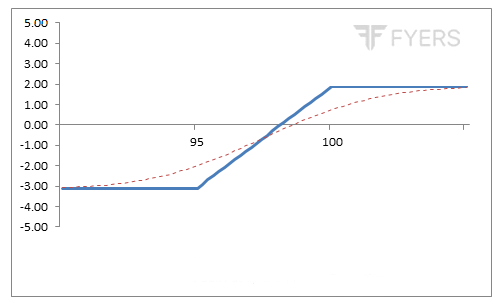

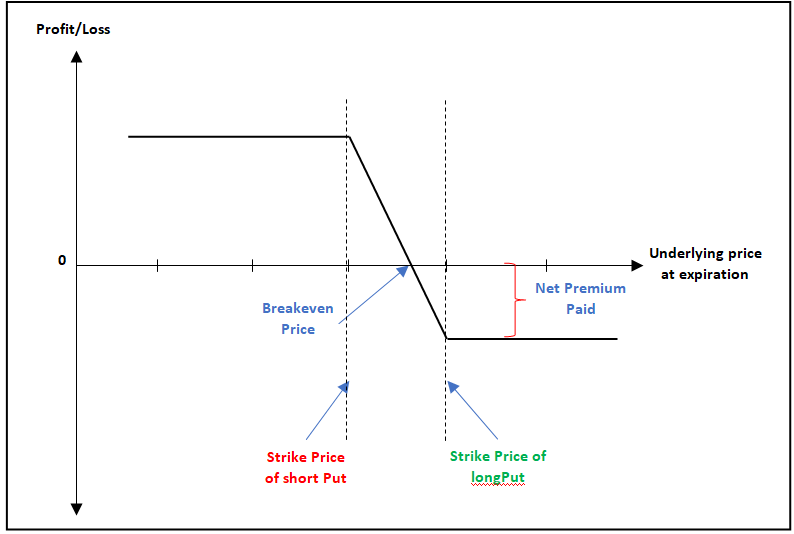

Payoff of Bear Put Spread

The chart below is the payoff chart of a Bear Put Spread strategy. Observe that the payoff structure of this strategy is quite similar to that of a Bear Call Spread. However, there are differences between the two. The most notable difference is that while a Bear Call Spread is a net credit strategy, a Bear Put Spread is a net debit strategy. As a result, there is cash inflow into your trading account when you execute a Bear Call Spread and a cash outflow from your trading account when you execute a Bear Put Spread.

It can be seen from the above chart that as long as the underlying price is above the higher strike price, the position will be suffer maximum loss. This maximum loss will be limited to the extent of net premium paid, no matter how higher the underlying price goes above the higher strike price. The quantum of loss reduces when the underlying price is between the higher strike price and the breakeven price. And once the underlying price falls below the breakeven price, the position starts making money, until the underlying price reaches the lower strike price, at which the maximum profit gets capped. No matter how lower the underlying price drops below the lower strike price, the trader will not earn anything in excess. Hence, Bear Put Spread is a limited profit, limited loss strategy. The gains/losses are made when the underlying price is in between the two strikes and flattens out when the underlying price moves beyond the two strikes.

Example of Bear Put Spread

Let us say that Mr. ABC has analysed the chart of Nifty and has concluded that the index will drop 4-5% in the short-term from the current levels. Besides, ABC has also concluded that the index is unlikely to drop any further and is likely to maintain a moderately negative tone in the short-term. Based on this, ABC decides to initiate a Bear Put Spread strategy, wherein he will buy 1 ATM 8250 Put at the prevailing price of ₹555 and simultaneously sell 1 OTM 7900 Put at the prevailing price of ₹460. Let us summarize the details of the strategy below:

-

Strike price of long Put = 8250

-

Strike price of short Put = 7900

-

Long Put premium = ₹555

-

Short Put premium = ₹460

-

Net Debit = ₹95 (555 - 460)

-

Net Debit (in value terms) = ₹7,125 (95 * 75)

-

Breakeven price of the strategy = ₹8,155 (8250 - 95)

-

Maximum Potential Loss = ₹7,125

-

Maximum Potential Profit = ₹19,125 ((8250 - 7900 - 95) * 75)

Now, let us assume a few scenarios in terms of where Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 10000 | Loss of ₹7,125 | Payoff = [maximum of (8250-10000,0)-555]+[460- maximum of (7900-10000,0)]. As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 9000 | Loss of ₹7,125 | Payoff = [maximum of (8250-9000,0)-555]+[460- maximum of (7900-9000,0)]. As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 8500 | Loss of ₹7,125 | Payoff = [maximum of (8250-8500,0)-555]+[460- maximum of (7900-8500,0)]. As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 8250 | Loss of ₹7,125 | Payoff = [maximum of (8250-8250,0)-555]+[460- maximum of (7900-8250,0)]. As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 8200 | Loss of ₹3,375 | Payoff = [maximum of (8250-8200,0)-555]+[460- maximum of (7900-8200,0)]. As the underlying price at expiration is above the breakeven price, the trader will incur a loss |

| 8155 | No profit, No loss | Payoff = [maximum of (8250-8155,0)-555]+[460- maximum of (7900-8155,0)]. As the underlying price at expiration is equal to the breakeven price, the trader will neither make a gain nor make a loss |

| 8000 | Profit of ₹11,620 | Payoff = [maximum of (8250-8000,0)-555]+[460- maximum of (7900-8000,0)]. As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 7900 | Profit of ₹19,125 | Payoff = [maximum of (8250-7900,0)-555]+[460- maximum of (7900-7900,0)]. As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 7500 | Profit of ₹19,125 | Payoff = [maximum of (8250-7500,0)-555]+[460- maximum of (7900-7500,0)]. As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 7000 | Profit of ₹19,125 | Payoff = [maximum of (8250-7000,0)-555]+[460- maximum of (7900-7000,0)]. As the underlying price at expiration is below the breakeven price, the trader will make a gain |

| 6000 | Profit of ₹19,125 | Payoff = [maximum of (8250-6000,0)-555]+[460- maximum of (7900-6000,0)]. As the underlying price at expiration is below the breakeven price, the trader will make a gain |

Notice in the above table that the maximum loss is limited to ₹7,125 no matter how lower the underlying price goes below the lower strike price of 7900. Similarly, the maximum profit is limited to ₹19,125 no matter how higher the underlying price rises above the higher strike price of 8250. That said, as this is a capital gain strategy, keep in mind that from the time of strategy initiation, the underlying price will have to drop below the breakeven price for the trader to start making gains. Until that happens, the trader would be in a loss-making position.

BULL PUT SPREAD

| Strategy Details | |

| Strategy Type | Moderately bullish |

| # of legs | 2 (Short OTM, higher strike Put + Long OTM, lower strike Put) |

| Maximum Reward | Premium of short Put - Premium of long Put |

| Maximum Risk | (Strike price of short Put - Strike price of long Put) - (Premium of short Put - Premium of long Put) |

| Breakeven Price | Strike price of short Put - (Premium of short Put - Premium of long Put) |

| Payoff Calculation | Payoff of Long Put+ Payoff of Short Put |

Explanation of the Strategy

A Bull Put Spread involves selling a slightly OTM Put option and simultaneously buying an OTM Put option with an even lower strike price. Both the options that are transacted must have the same underlying asset and the same expiration date. This is a moderately bullish strategy that benefits when the price of the underlying either remains sideways or rises moderately until the expiration of the option.The lower strike Put option that has been bought acts as an insurance to the higher strike Put option that has been sold. In case the view of the trader goes wrong and the underlying price declines, the losses will get capped at the lower of the two strike prices. So, a Bull Put Spread can be thought of as writing a naked Put but with downside protection. Because the premium received on selling the higher strike Put is greater than the premium paid on buying the lower strike Put, this is a net credit strategy.

Just like the downside of the strategy is limited, so is the upside. No matter how higher the underlying price rises, the trader will not earn a penny more than what he/she has already received in the form of net credit. While the Put that is sold is slightly OTM, there are no restrictions on the lower strike Put that is bought in terms of how lower it can be as compared to the higher strike Put that has been sold. This depends on the trader and is usually a trade-off between the net credit received and the risk involved in case the view of the trader goes wrong. Generally speaking, the wider the difference between the two strikes, the higher will be the net credit that the trader will receive, but the higher will be the loss in case the underlying price falls to the lower strike price, and vice versa. Meanwhile, the strategy is profitable as long as the underlying price is above the breakeven price and is unprofitable when the underlying price is below the breakeven price.

Benefits of the Strategy

-

The lower strike Put that is bought acts as an insurance to the higher strike Put that is sold

-

Maximum loss is capped at the lower strike price

-

The trader can profit even if the underlying price remains sideways

-

If used in correct market conditions, the strategy can be a good source of periodic income

Drawbacks of the Strategy

-

Maximum reward is limited to the extent of net credit received

-

In case the underlying price rises sharply, there would be an opportunity loss

-

In absolute value terms, the risk is usually greater than the reward

Strategy Suggestions

-

Ensure that the price of the underlying is either sideways or trending moderately higher and is unlikely to fall in the near-term

-

Ensure that the options you are transacting are not far awayfrom expiry so that there is not much time left for the underlying price to move against you

-

Having said that, also ensure that the options are not too close to expiry so that the net credit received is not too small to compensate for the risk involved

-

Be realistic when selecting the strike price of the long Put

-

Remember, you would want the underlying price to stay above the higher strike price, in order to earn maximum profit

-

Remember that the difference between the two strikes will be a trade-off between risk and the net credit that is received

-

Ensure that there is sufficient liquidity in the underlying that is being chosen to initiate this strategy

Option Greeks for Bull Put Spread

| Greek | Value is | Notes |

| Delta | Positive |

The overall Delta is positive at initiation. As a result, the position stands to benefit when the underlying price rises, and vice versa. |

| Gamma | Negative |

At initiation, the position Gamma is negative, causing the position Delta to fall as the underlying price rises, and vice versa. However, when the underlying price is below the breakeven price, the position Gamma is positive, which causes the position Delta to rise for a given rise in the underlying price, and vice versa. |

| Vega | Negative |

At initiation, the overall Vega is negative, meaning volatility hurts the position as long as the underlying price is above the breakeven price. When the underlying price is below the breakeven price, overall Vega ispositive, meaning volatility will benefit the position. |

| Theta | Positive |

The overall Theta is positive at initiation, meaning time decay benefits the position as long as the underlying price is above the breakeven price. However, when the underlying price is below the breakeven price, Theta is negative, meaning time decayhurts the position. |

| Rho | Positive |

The overall Rho is positive at initiation. As a result, rising interest rates benefit the position, and vice versa. However, it must be noted that this is the least significant of the Greeks, especially in case of short-dated options. |

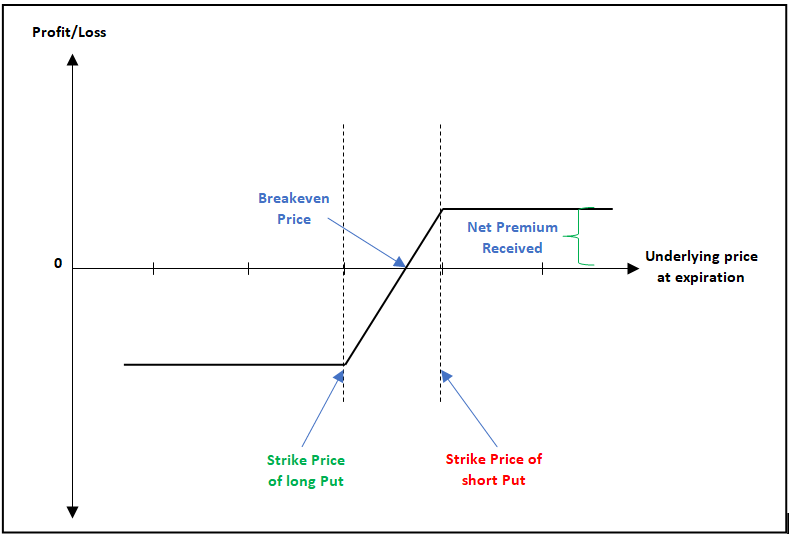

Payoff of Bull Put Spread

The chartbelow is the payoff chart of a Bull Put Spread. Notice that it is quite similar to that of a Bull Call Spread. However, there are differences between the two. The most noteworthy is that a Bull Put Spread is a net credit strategy, while a Bull Call Spread is a net debit strategy.

Notice above that the spread is unprofitable when the underlying price is to the left of the breakeven price and is profitable when the underlying price is to the right of the breakeven price. Also notice that losses and profits are capped at lower strike and higher strike, respectively. At the time of initiation of the spread, because the higher strike is usually just below the underlying price, the spread is already at the sweetest spot. In other words, at the time of initiation, the strategy is already at its maximum profit potential. Hence, the trader would want the underlying price to either remain as is or rise only moderately going forward. If there is a sharp rise in the price of the underlying, there would be an opportunity loss as the trader would not be able to advantage of that rise.

Example of Bull Put Spread

Mr. ABC is of the opinion that Nifty will maintain a range bound to moderately positive tone in the coming days. He observes strong support at 8000 which he feels would hold for the current expiry. He also feels that Nifty is unlikely to cross 8400-8500 zone in the coming days. Based on his observations, Mr. ABC decides to enter into a Bull Put Spread strategy, wherein he will sell a slightlyOTM 8200 strike Put option at ₹540 and simultaneously buy an OTM 7800 strike Put option at ₹385. Given that he would be paying a premium of ₹385 and receiving a premium of ₹540, the net credit would amount to ₹155. Let us summarize the details below:

-

Strike price of long Put = 7800

-

Strike price of short Put = 8200

-

Long Put premium = ₹385

-

Short Put premium = ₹540

-

Net Credit = ₹155

-

Net Credit (in value terms) = ₹11,625 (155 * 75)

-

Breakeven price of the strategy = ₹8,045 (8200 - 155)

-

Maximum Risk = ₹18,375 ((8200 - 7800 - 155) * 75)

-

Maximum Reward = ₹11,625

Now, let us assume a few scenarios in terms of where Nifty would be on the expiration date and the impact this would have on the profitability of the trade.

| Underlying price at Expiration | Net Profit/Loss | Notes |

| 6000 | Loss of ₹18,375 | Payoff = [maximum of (7800-6000,0)-385]+[540- maximum of (8200-6000,0)]. As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 7000 | Loss of ₹18,375 | Payoff = [maximum of (7800-7000,0)-385]+[540- maximum of (8200-7000,0)]. As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 7500 | Loss of ₹18,375 | Payoff = [maximum of (7800-7500,0)-385]+[540- maximum of (8200-7500,0)]. As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 7800 | Loss of ₹18,375 | Payoff = [maximum of (7800-7800,0)-385]+[540- maximum of (8200-7800,0)]. As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 8000 | Loss of ₹3,375 | Payoff = [maximum of (7800-8000,0)-385]+[540- maximum of (8200-8000,0)]. As the underlying price at expiration is below the breakeven price, the trader will incur a loss |

| 8045 | No profit, No loss | Payoff = [maximum of (7800-8045,0)-385]+[540- maximum of (8200-8045,0)]. As the underlying price at expiration is equal to the breakeven price, the trader will neither make a gain nor make a loss |

| 8150 | Profit of ₹7,875 | Payoff = [maximum of (7800-8150,0)-385]+[540- maximum of (8200-8150,0)]. As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 8200 | Profit of ₹11,625 | Payoff = [maximum of (7800-8200,0)-385]+[540- maximum of (8200-8200,0)]. As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 8500 | Profit of ₹11,625 | Payoff = [maximum of (7800-8500,0)-385]+[540- maximum of (8200-8500,0)]. As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 9000 | Profit of ₹11,625 | Payoff = [maximum of (7800-9000,0)-385]+[540- maximum of (8200-9000,0)]. As the underlying price at expiration is above the breakeven price, the trader will make a gain |

| 10000 | Profit of ₹11,625 | Payoff = [maximum of (7800-10000,0)-385]+[540- maximum of (8200-10000,0)]. As the underlying price at expiration is above the breakeven price, the trader will make a gain |

Notice in the table above that maximum reward is limited to the extent of net credit received, which is ₹11,625. This occurs when the underlying price is at or above the higher strike price. Observe that no matter how higher the underlying price goes above the higher strike price, profit does not increase. On the other hand, maximum risk is limited to the extent of ₹18,375. This occurs when the price of the underlying declines and touches or falls below the lower strike price. No matter how lower the underlying price falls below the lower strike price, the trader does not incur any further additional losses.

Next Chapter

Comments & Discussions in

FYERS Community