In this chapter, we shallstudy the correlation that exists between the dollar and commodities. Thegeneral correlation between these two asset classeshas stood the test of time, although at times its strength and magnitude has varied. From an intermarket perspective, it is important to understand the correlation between the dollar and commodities and to then monitor the trajectory of these two asset classes on a real time basis, given the influence they can have on the trends of other asset classes, namely bonds and stocks.

The inverse correlation between Dollar and Commodities

Historically, the dollar and commodities have exhibited an inverse correlation between them. In other words, a rising dollar has typically coincided with falling commodities prices, and vice versa. Of course, it goes without saying that this correlation need not necessarily hold every single day, as there would be several other factors that would individually be impacting the dollar and commodities. That said, if you compare the general price trajectory of these two asset classes, you will notice the existence of an inverse correlation between them.

The question that you might ask is what impacts what? Is it the dollar that impacts commodity prices, or is it commodity prices that impact the dollar? Well, most of the times, it is the dollar that impacts the general trajectory of commodity prices. However, after a certain point in time, the roles can reverse. That is, commodity prices could start influencing the trajectory of the dollar. Let us now understand each of these aspects, one at a time.

International commodities are priced in Dollar terms

Allcountries import/export commodities. Nations import commodities when they need them for consumption but are either unable to produce them locally or the production is falling short of consumption. On the other hand, nations export commodities when they have surplus of them after meeting the domestic consumption and as such want to earn export revenue from these surpluses. When nations import commodities, they need to make payment for theseimports. Similarly, when nations export commodities, they would receive payment for the same. As these are international transactions, things would be much simpler if:

-

There was a common currency in which two countries could transact, and

-

Commodities were priced in a common currency

Let’s go back in history now. By the end of World War 1, the US had become a major economic and military power. It had overtaken England as the world’s largest economy, had the largest reserves of gold in the world, and had a stable currency and a stable monetary system. Also, by the end of World War 1, the US had become a net creditor nation, meaning other nations owed more to the US than the US owed to them. As a result, the dollar became a dominant global currency. A lot of nations who had abandoned the Gold Standard system back then started pegging the value of their currency to the Dollar rather than to gold.Over time, the dollar become the world’s reserve currency, a position that it still holds today and is likely to do so in the foreseeable future. As such, when it comes to international transactions, the dollar is a common currency that is on one side of all trades in a vast majority of cases. For the very same reason, a vast majority of international commodities are priced in dollar terms, be it precious metals, industrial metals, energy complex, or agro-commodities.

The dollar's influence on the trend of commodity prices

Now that we knowwhyglobalcommodities are mostly priced in dollars and why global transactions are settled in dollars, let us understand why the dollar’s trajectory influences commodity prices.

When the dollar strengthens, it means other currencies, in general, are weakening. This makes it more expensive for holders of foreign currencies to import commodities. For instance, let us assume that I am a commodity importer from India.If the dollar has strengthened against the rupee while commodity prices have not fluctuated much, it means to import the same quantity of the commodity, I will have to exchange more rupees to buy dollars (remember, global payments are mostly done in dollars). As a result, my purchasing power has reduced because of the dollar’s strength. Hence, as the dollar strengthens, other things constant, demand for commodities from holders of foreign currencies can decline. Due to such expectations, commodity prices, in general, tend to fall during times when the dollar is strengthening.

On the other hand, when the dollar weakens, it means other currencies, in general, are strengthening. This makes it less expensive for holders of foreign currencies to import commodities. Taking the same example as above, if the dollar has weakened against the rupee while commodity prices have not fluctuated much, for an Indian commodity importer to import the same quantity of the commodity, fewer rupees need to be exchanged to buy dollars. As a result, the purchasing power of the Indian importer would increase because of the dollar’s weakness. Hence, as the dollar weakens, other things constant, demand for commodities from holders of foreign currencies tends to increase. Due to such expectations, commodity prices, in general, tend to rise during times when the dollar is weakening.

Looking at it the other way, you will notice that when the dollar strengthens, all else constant, commodities that are priced in foreign currency terms will become more expensive to buy, and vice versa. As a result, as the dollar strengthens, the demand for commodities locally in foreign countries tends to weaken, and vice versa. To understand this better, let us talk about dollar-priced gold and rupee-priced gold. Back in August 2011, when the dollar-priced gold hit a record high of $1,920/oz, the rupee-priced gold was quoting around₹29,000/10gms. Fast forwarding to today, the dollar-priced gold is at $1,800/oz while the rupee-priced gold is at ₹49,000/10gms. Notice the difference? See that while the dollar-priced gold is still 5-10% below its 2011 highs, the rupee-priced gold is 70% above the corresponding period high! The reason why the rupee-priced gold has become so expensive relative to the dollar-priced gold is because the dollar has strengthened remarkably against the rupee during this period – from below 45 back then to above 75 today, which is a gain of over 65%.

Let us now summarize the dollar’s impact on commodities

-

As the dollar strengthens, all else constant, demand for commodities from holders of foreign currency can be expected to weaken. As a result, commodity prices tend to soften

-

As the dollar weakens, all else constant, demand for commodities from holders of foreign currency can be expected to pick up. As a result, commodity prices tend to strengthen

We will talk more about this in the coming sections, wherein we will present historical charts to show the inverse correlation between the dollar and commodities.

Late in a cycle, commodities could start influencing the dollar's trend

Till now, we have talked about how the dollar impacts the price trends of commodities. Can commodities impact the dollar? The answer to this question is yes. Late in a business cycle (either the late expansionary stage or the mid-to-late contractionary stage), commodity prices can start influencing the dollar’s trend. Let us explain how this can happen. In the mid-to-late expansionary stage of a business cycle, as economic activity starts accelerating, commodity prices tend to strengthen sharply because of high demand for them. An important thing to keep in mind is that there is a positive link between commodity prices and inflation.Rising commodity prices are generally considered inflationary, especially because food and energy prices are a key component of various price indices such as the Consumer Price Index (CPI). Late in the expansionary stage of a business cycle, as commodity prices heat up because of excess demand, inflationary pressures mount. This in turn raises expectations that, at some stage, the Federal Reserve (aka the Fed), which is the US central bank, could increase interest rates to tame in price pressures and prevent the US economy from overheating. Such expectations can eventually start exerting upward pressure on the dollar. Hence, late in an expansionary business cycle, it should not come as a surprise to see the dollar starting to strengthen, which indirectly stems from higher commodity prices.

The opposite is also true during mid-to-late contractionary stage. During this period, as economic activity slows down, demand for commodities starts declining, because of which commodity prices decline.As commodity prices decline and economic activity reduces, inflation starts decelerating as well. Slowing economic activity and decelerating inflation raises expectations that, at some stage, the Fed could start cutting rates to revive economic activity. Such expectations can eventually start dragging the dollar southwards. Hence, in a mid-to-late contractionary stage, it shouldn’t come as a surprise to see the dollar starting to soften, which indirectly and partly stems from commodity prices.

Let us now summarize the impact commodities can indirectly have on dollar late in a business cycle:

-

In the late expansionary stage of a business cycle, commodity price uptrend tends to accelerate, which coupled with an overheating economy raises interest rate hike expectations from the Fed. This in turn can cause the dollar to strengthen

-

In the mid-to-late contractionary stage of a business cycle, commodity price downtrend tends to accelerate, which coupled with deceleration in economic activity raises interest rate cut expectations from the Fed. This in turn can cause the dollar to weaken

This loop of commodities being impacted by dollar’s trend for most parts of the business cycle before eventually influencing the dollar towards the end of business cycle often tends to keep repeating.

Dollar and the S&P GSCI

In the previous section, we talked about how and why the dollar impacts the price trends of commodities. Let us now graphically see this correlation between the dollar and commodities.

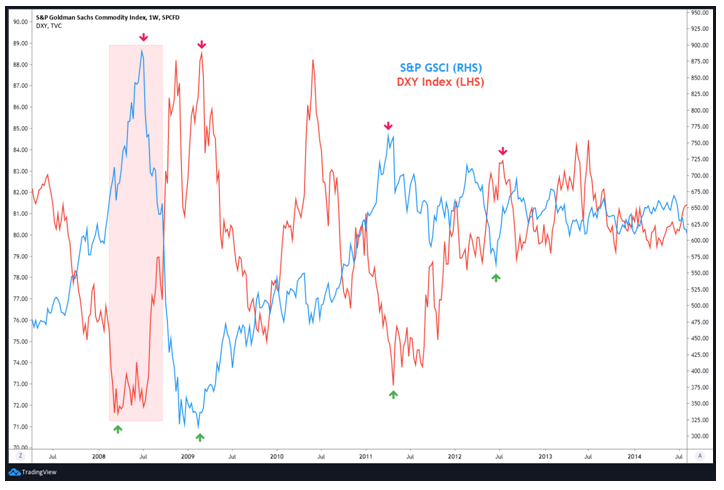

The chart below compares the price action of the Dollar Index (represented by the orange line) and S&P GSCI (represented by the blue line) between 2001 and 2008. Prior to July 2001, see that the DXY was in an uptrend and S&P GSCI was in a downtrend. Later, notice that the DXY made a major top in July 2001 and then a slightly lower top in January 2002. After the second top, the DXY started its major decline. Observe that the second top in DXY in January 2002 precisely coincided with a bottom in S&P GSCI. Post January 2002, the DXY entered a major downtrend, which caused S&P GSCI to enter a major uptrend. This trend between the dollar and commodities continued from early-2002 to mid-2008. Meanwhile, notice the price action in 2005. During this year, the DXY trended higher but so did S&P GSCI. This brings us to an important point. The inverse correlation between the dollar and commodities need not necessarily hold at all points in time. Occasionally, the correlation could break and the two could move in the same direction for a certain period, as there are various factors in play that could be affecting the individual trends of the dollar and commodities. One must always keep this in mind when looking at correlations between two asset classes.

The chart below compares the price action of the DXY (represented by the orange line) and S&P GSCI (represented by the blue line) between 2008 and 2014. Notice that the DXY ended its 6-year downtrend and bottomed out in March 2008. After a minor 2-3-month consolidation, the DXY started trending higher. This bottom in DXY eventually caused S&P GSCI to peak out and end its 6-year uptrend in June 2008. Post this, S&P GSCI entered a steep and a swift downtrend. See that this downtrend in S&P GSCI ended in February 2009, which coincided with the DXY toppingout and starting to trend lower. From February 2009 till April 2011, the DXY was in a downtrend, which caused S&P GSCI to strengthen during this period. Later, from April 2011 to July 2012, the DXY was in an uptrend, which caused S&P GSCI to weaken during this period. Between July 2012 and June 2014, notice that the sideways movement in DXY coincided with a sideways movement in S&P GSCI. Overall, observe how well the inverse correlation stood between the dollar and commodities during this 6-year period.

The chart below compares the price action of the DXY (represented by the orange line) and S&P GSCI (represented by the blue line) from 2014 till date. See that after a 2-year consolidation, the DXY bottomed out in April 2014 and started trending higher. The S&P GSCI topped out in June 2014 and started trending lower. The rally in DXY continued till November 2015 before it topped out and started trending lower. Eventually, S&P GSCI bottomed out in January 2016 before it started trending higher. The region that is highlighted inside the shaded box represents the period when the inverse correlation between the dollar and commodities broke. During this period, notice that the dollar and commodities rose simultaneously and then fell simultaneously. Eventually however, the dollar’s decline started benefiting commodities, as S&P GSCI resumed it rally from June 2017 till October 2018. Observe that the DXY bottomed out in February 2018 and started trending higher. Initially, S&P GSCI wasn’t impacted by the dollar’s strength as both continued to rise simultaneously. However, as the DXY continued to trend higher, S&P GSCI eventually succumbed to the dollar’s strength and topped out in October 2018. From October 2018 till March 2020, the DXY was in an uptrend, which caused S&P GSCI to trend lower. The DXY topped out in March 2020 and has been trending lower since then. This in turn caused S&P GSCI to bottom out in April 2020, which has been in an uptrend since then.

Notice how strongly the inverse correlation between the dollar and commodities has played out since the turn of the century. Occasionally, the correlation tends to break, and one needs to be aware of this. However, broadly speaking, the inverse correlation between the two tends to hold very well. From this, it can be concluded that:

-

A rising dollar, as it tends to exert downward pressure on commodity prices, is disinflationary

-

A falling dollar, as it tends to exert upward pressure on commodity prices, is inflationary

Dollar and Crude oil

Earlier, we talked about the correlation between the dollar and commodities using S&P GSCI. In the next few sections, we shall look at how the correlation holds between the dollar and individual commodities. Of course, there are various commodities that are traded around the world. We won’t be looking at each one of them. Instead, we will just look at four key commodities, one from each of the four groups, and compare them with the dollar. These four commodities are crude oil, copper, soybean, and gold. In this section, we shall look at the correlation between the dollar and crude oil.

Crude oil is one of the most watched, most used, and most traded commodities in the world. It is also one of the most important commodities of all as it affects the livelihood of virtually everyone on this planet. It is a commodity whose price is closely monitored by central banks and governments around the world, given the widespread impact it has on inflation and a nation’s trade balance. Rising oil prices could suggest that global economic conditions are strengthening. However, too high a price can pose problems and lead to a surge in price pressures. On the other hand, falling oil prices are beneficial to consumers as well as to several countries, especially those who rely on oil imports to meet the demand requirements. However, too low a price can pose problems to exporting nations while also raising worries over the health of the global economy. Hence, a stable oil price is usually preferred by most nations. Let us compare how oil priceand the dollar correlate to each other.

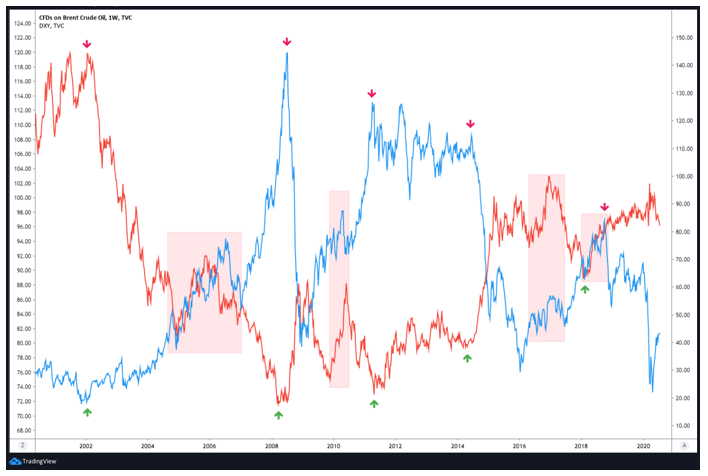

The chart above compares the price action of the DXY (represented by the orange line, LHS) and Brent crude oil (represented by the blue line, RHS) from 2000 till date. The objective of this chart is to show the major trend turning points between the two. See that the major top in DXY in January 2002 coincided with a major bottom in oil during the same period. From here on until June 2008, DXY fell while oil rose. The bottom in DXY in June 2008 and its subsequent rally coincided with a top in oil and its subsequent decline. From March 2009 to April 2011, see that the decline in DXY benefited crude oil, which ended its steepest fall in history and rallied strongly during this period. Between April 2011 and April 2014, notice that the higher low in DXY coincided with a lower high in oil. From April 2014, the DXY started a powerful and a swift rally, which coincided with oil prices plummeting during this period. An interesting thing to note here is that oil prices bottomed in January 2016, which was much earlier than the peak in DXY, which topped out later that year in December. This highlights that the lead-lag times can occasionally vary. From December 2016 till February 2018, the DXY fell, which benefited oil prices. The DXY eventually bottomed in February 2018 and started rallying. This rally in DXY subsequently ended the oil price rally in October 2018 (again notice the lead-lag time). From here on until March 2020, DXY rose while oil fell. Since March 2020, observe that the fall in DXY has coincided with a rise in oil prices.Meanwhile, also noticethe shaded regions. These refer to periods when the inverse correlation between DXY and oil broke and the two moved in the same direction.

It can be seen from the price action over the past two decadesthat the dollar and crude oil share a nice inverse correlation between them. That is, a strengthening dollar has a negative impact on oil prices, and vice versa. Occasionally, as we saw above, the correlation between the two can break for a certain period. Another thing we observed was that the lead-lag time between a top in one and a bottom in the other can at times vary, which is very important to keep a note of. That said, from a longer-term perspective, the inverse correlation between the dollar and crude oil holds strong.

Dollar and Copper

Just like crude oil, copper is also a bellwether commodity. It is often called as ‘Dr. Copper’ because of its widespread usage across industries as well as in the construction and home building sector. The price of copper can tell a lot about the health of the global economy. Rising copper prices usually coincide with strengthening economy. This is because when economic conditions strengthen, industrial and construction activity tend to pick up, which boosts demand for copper, thereby lifting its price. Similarly, falling copper prices usually coincide with weakening economy. This is because when economic conditions weaken, industrial and construction activity tend to slowdown, which reduces demand for copper, thereby dragging down its price. Supply-side factors can also influence the price trajectory of copper. For instance, any unexpected labor unrest issue or natural disastersin major copper-mining regions could hamper production and thereby lift prices. Let us compare how copper price and the dollar correlate to each other.

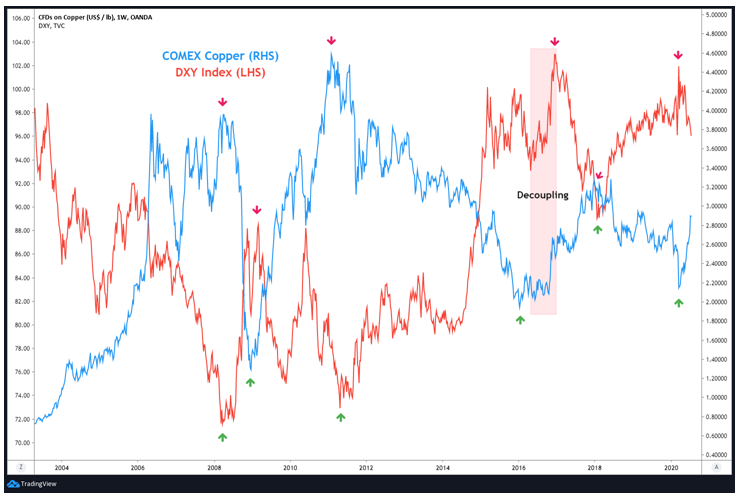

The chart above compares the price action of the DXY (represented by the orange line) and US Copper (represented by the blue line) from 2000 till date. The objective of this chart is to show the major trend turning points between the two. Observe that the DXY bottomed in March 2008, precisely in the same month when copper topped out. From March 2008 till February 2009, the DXY strengthened, causing copper prices to head south during this period. However, copper prices bottomed a couple of months prior to the peak in the DXY. From February 2009 till April 2011, the DXY was in a downtrend. During this 2-year period, copper prices rallied sharply before topping out in January 2011. See yet again that copper prices turned three months before the dollar turned. Then, from April 2011 to December 2016, the DXY trended higher. During this period, copper prices were in a steady downtrend, which ended in January 2016. See that copper bottomed out nearly a year before the DXY topped out and see the decoupling in the second half of 2016 – both DXY and copper mostly headed higher during this period.The decline in DXY from December 2016 continued till January 2018, during which time copper prices headed higher. The DXY then bottomed in January 2018 and rallied until March 2020. See this this 2-year rally in DXY precisely coincided with a 2-year decline in copper prices. Since March 2020, the DXY has inched lower, which has helped copper prices to recovery strongly.

Overall, we could observe from the above chart that there is a strong inverse correlation between the dollar and copper prices as well. Interestingly, sometimes, there is a tendency for copper to turn ahead of the dollar, as we saw above.

Dollar and Soybean

Soybean is one of the most traded as well as one of the most watched agricultural commodities. It is widely used across the world both for human consumption and as a source of protein for animal feeds. As it is priced in dollars, the price of soybean is impacted by the dollar’s strength. Let us compare how soybean price and the dollar correlate to each other.

The chart above compares the price action of the DXY (bottom panel) and CBOT Soybean (top panel) from 2000 till date. The objective of this chart is to show the major trend turning points between the two. Observe that the major downtrend in the dollar from January 2002 till March 2008 coincided with a major uptrend in soybean prices during this same period. The DXY bottomed out in March 2008 and rallied for the next one year till March 2009. During this 1-year bull market in DXY, soybean prices corrected sharply, retracing a significant portion of their 2002-2008 advance. After topping out in March 2009, the DXY was in a downtrend till April 2011, albeit with a great bout of volatility. During this 2-year downtrend in DXY, soybean prices headed higher, recovering entirely from the prior fall. From April 2014 till December 2016, the DXY strengthened notably, causing soybean prices to fall sharply during this period.

Meanwhile, notice in the chart the shaded regions. These indicate periods when the inverse correlation between the DXY and soybean did not hold. An important this to keep in mind is that as soybean is an agro-commodity, it is at times heavily influenced by supply-side factors and global weather patterns. As a result, during these periods, the inverse correlation between the two may not hold very well. That said, from a longer-term perspective, the inverse correlation between the dollar and soybeanhas held strongly.

Dollar and Gold

Gold is one of the most eyed commodities of all. In fact, it wouldn’t be wrong in saying that gold is as much of a currency as it is a commodity. Before currency notes and coins came into circulation, gold was a standard medium of exchange for several centuries. It was and still is considered an ideal store of value. While most other commodities are primarily used for consumption, gold is heavily used as an investment vehicle and in the form of jewelry. Because of its scarce supply, the value of gold has steadily appreciated over the years. Gold is often used as a hedge against inflation and tends to perform strongly when currencies are being devalued. Gold is also used as a hedge against tail risks and tends to perform well during times of heightened volatility and risk aversion in the markets. Besides equities, fixed income instruments, cash, and real estate, gold also forms an important part of an investor’s portfolio that is used to diversify risks. Because gold is priced in dollars, it tends to be extremely sensitive to dollar’s movement. In fact, gold is one of the most sensitive commodities to the dollar’s fluctuation. Major turns in the dollar usually tends to coincide with major turns in gold prices as well, precisely at more or less the same time. Unlike other commodities, where supply-side developments can strongly influence their prices and cause them to decouple from the dollar, gold is not much impacted by supply-side developments. Instead, activity on the demand-side is what tends to drive gold prices the most. Let us compare how gold and the dollar correlate to each other.

The chart above compares the price action of the DXY (bottom panel) and Gold (top panel) from 2000 till date. The objective of this chart is to show the major trend turning points between the two. Observe that the major bear market in DXY from January 2002 to March 2008 coincided with a major bull market in gold, during which time gold prices nearly quadrupled in value. The DXY bottomed out in March 2008 and rallied until March 2009. This caused gold to top out in March 2008 and decline until October 2008. Notice that gold bottomed out nearly six months before the DXY topped out. In fact, during these 6 months, gold recovered from most of its previous drop and was back near its prior highs. The breakdown in the inverse correlation between gold and DXY during this period was due to the unprecedented volatility in global markets as a result of the collapse of the Lehman Brothers in September 2008, which caused a flight to safety and subsequently benefited gold. For the next couple of years from March 2009 to April 2011, the DXY was in a bear market, which played a key role in propelling gold prices higher. During the 2.5-year period between October 2008 and August 2011, gold prices nearly tripled in value. The DXY bottomed in April 2011 and entered a bull market, which lasted until December 2016. During this 5.5-year bull market in the DXY, gold prices came under increasing pressure, nearly halving in value during this time. From December 2016 till February 2018, a weakening DXY caused gold to recover, albeit at a slower pace.

Notice the portions that are marked within the shaded regions. These reflect periods when the inverse correlation between gold and DXY broke. See that between August 2018 and March 2020, both gold and DXY moved higher. Since then however, the inverse correlation between them has resumed as gold has been heading higher since March 2020 while the DXY has been heading lower.

Of all the commodities, gold tends to have the strongest inverse correlation with the DXY. Hence, it is important to keep a track of the price trajectory of both these assets. A weakening dollar is inflationary and as gold is often used as a hedge against inflation, it tends to perform well during periods when the dollar is weakening, and vice versa.

Gold often tends to lead Commodities

As said earlier, gold is one of the most sensitive commodities to the dollar’s fluctuation. Major turns in the dollar usually tends to coincide with major turns in gold prices as well, precisely at more or less the same time. While gold usually tends to move in the same direction as other commodities in general, there is a tendency for gold to turn ahead of other commodities. That is important tops and bottoms in gold usually precede important tops and bottoms in other commodities. Let us illustrate this using the chart below:

The above chart compares the price action between gold (bottom panel) and S&P GSCI (top panel) over the past two decades. The objective of this chart is show that in vast majority of cases, gold often tends to turn before other commodities, in general, do. Notice above that gold bottomed in March 2001 and started rising. The S&P GSCI bottomed 9 months later in December 2001 and started rising. The primary bull market in gold hit its first intermediate hurdle in May 2006, causing the metal to enter a corrective mode until October 2006. The S&P GSCI followed suit 2 months later as it hit an intermediate peak in July 2006 and underwent a correction until January 2007. After rallying from October 2006, gold hit a second intermediate hurdle in March 2008 and underwent a correction that lasted till October 2008. The S&P GSCI yet again followed suit as it rallied from January 2007 till June 2008. However, unlike gold, which underwent an intermediate correction between March 2008 till October 2008, the S&P GSCI underwent a very deep correction from June 2008 till February 2009. Subsequently, as gold resumed its primary bull market from October 2008, the S&P GSCI also resumed the rally from February 2009. However, this time, the S&P GSCI topped out earlier in April 2011, whereas gold topped out a few months later in August 2011.

Notice that in February 2013, gold broke a rising trendline support, which signaled at lower prices. If history were to go by, the move lower in gold was a warning that the S&P GSCI could top out in the months ahead. This did happen in June 2014, when the S&P GSCI broke below a rising support line, signaling lower prices ahead. That said, see that there was a significant lag here. Gold price broke down in February 2013, while the S&P GSCI broke down in June 2014 – a lag of 16 months! The two fell in the subsequent months, with gold bottoming in November 2015 and the S&P GSCI bottoming in January 2016. From here on, both gold and the S&P GSCI rallied. However, notice the portion that is marked in the shaded region. It can be seen that gold and the S&P GSCI diverged during this period, when gold prices rose while other commodities, in general, fell. Post March 2020, the positive correlation between the two has resumed.

The purpose of talking about this is to show that gold often acts as a leading indicator of commodities. It is important to know the existence of such relationships when it comes to trading and investing.

Using Commodity ratios to gauge market sentiment

Now that we have talked about how the dollar influences commodity prices and how gold prices often tend to lead commodity prices, it is time to move on. Now, we shall focus on the macro-economic implications of commodities, primarily by using ratio analysis of one commodity with another.

Gold to Crude oil ratio

Here, we shall talk about how to use the gold to crude oil ratio to gauge market sentiment. Before we proceed, keep in mind the following things:

- Gold is a safe haven asset that tends to perform well during times of heightened volatility, economic uncertainty, and currency debasement. During times of economic strength, demand for gold tends to decline

- Crude oil is a commodity that rises in value during times of economic strength and falls during times of economic weakness. Sometimes however, supply-side disruptions can cause oil to spike even during times of economic weakness, though such spikes have historically not lasted for prolonged periods of time

- Because rising oil price is inflationary and because gold is often used as an inflation-hedge, rising oil price can benefit gold if inflation becomes a threat, and vice versa

- Ratio analysis tells nothing about the absolute direction of two assets, but just their relative direction (i.e. whether one is outperforming the other or underperforming)

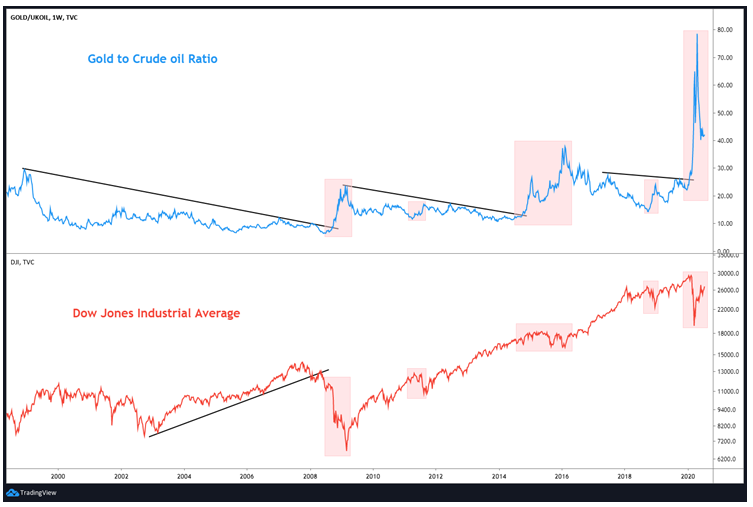

The above chart compares Gold to Crude oil ratio (top panel) with the Dow Jones Industrial Average (bottom panel). In the ratio, gold is in the numerator while crude oil (Brent) is in the denominator. At present, the ratio value is around 40, meaning 1 ounce of gold is equivalent to 40 barrels of crude oil. A rising ratio means gold is outperforming oil because of which more quantities of crude oil are needed to buy 1 ounce of gold, while a falling ratio means oil is outperforming gold because of which fewer quantities of crude oil are needed to buy 1 ounce of gold.

See that for most periods, the ratio tends to gradually trend lower. However, there is a tendency for the ratio to spike for brief periods of time. A downward trending ratio is a sign that economic conditions are strengthening, which typicallycauses crude oil to outperform gold. On the other hand, a rising ratio is a sign that economic conditions are weakening, which typically causes gold to outperform crude oil.In the above chart, notice the regions marked inside shaded boxes. These show the periods when there was a spike in the ratio, meaning gold swiftly outperformed crude oil. When the ratio spikes, risk assets usually experience strong bouts of volatility. Notice how the Dow Jones Industrial Average (DJIA), which is one of the most tracked equity indices around the world, fared during periods of strong spikes in the gold/crude oil ratio.

The above chart suggests that Gold/crude oil ratio can be used to monitor the prevailing risk appetite of market participants. A steady fall in the ratio is usually accompanied by strong risk appetite, which is generally bullish for risky assets; whereas periods when the ratio is breaking out or giving spikes is usually accompanied by risk aversion, which is generally bearish for risky assets.

Gold to Copper ratio

Now, we shall talk about how to use the gold to copper ratio to gauge market sentiment. Before we proceed, apart from what was said about gold earlier, keep in mind the following things:

-

Copper is barometer of global economic health because of its widespread usage in construction activities, electrical and electronic appliances, vehicle components etc.

-

As global economic conditions strengthen, demand for copper rises and subsequently lifts its price, and vice versa

-

China accounts for over half of the global demand for copper. Hence, economic health of China has a strong bearing on the price trends of copper

-

Sometimes, supply-side disruptions can cause copperto spike even during time of economic weakness, though such spikes have historically not lasted for prolonged periods of time

The above chart compares Gold to Copper ratio (top panel) with the Dow Jones Industrial Average (bottom panel). In the ratio, gold is in the numerator while copper (COMEX) is in the denominator. At present, the ratio value is around 625, meaning 1 ounce of gold is equivalent to 625 pounds of copper. A rising ratio means gold is outperforming copper because of which more quantities of copper are needed to buy 1 ounce of gold, while a falling ratio means copper is outperforming gold because of which fewer quantities of copper are needed to buy 1 ounce of gold.

In the above chart, notice that the ratio gradually trends lower most of the times. This indicates periods when copper is outperforming gold, which is a sign of economic strength. Notice how equities tend to rise during such periods. On the other hand, also observe the shaded regions in the ratio, which reflect periods when the ratio is spiking or is breaking out. This indicates periods when gold is outperforming copper, which is a sign of economic weakness. Notice how equities tend to come under pressure when the ratio is spiking.

The above chart suggests that Gold/copper ratio can be used to monitor the prevailing risk appetite of market participants. A gradual fall in the ratio is usually accompanied by strong risk appetite, which is generally bullish for risky assets; whereas periods when the ratio is breaking out or giving spikes is usually accompanied by risk aversion, which is generally bearish for risky assets.

Some interesting Commodity-Currency correlations

In this section, we shall talk about some interesting correlations that exist between a commodity and a currency pair. We will show the correlations using price charts wherein we shall compare movements in a commodity with that in a correlated currency pair. So, let us get started.

NYMEX Crude oil and USD/CAD

There is a very strong inverse correlation between NYMEX crude oil and USD/CAD. That is, when one rises, the other tends to fall, and vice versa. The reason for the existence of this correlation is because Canada is a major producer and exporter of crude oil, with a bulk of Canada’s oil going to the US. As per the government of Canada, a whopping 3.5 million barrels or 96% of its total oil exports went to the US alone in 2018. Because of the enormous volumes of oil exported to the US, the Canadian Dollar is verysensitive to the price trajectory of crude oil, given the strong inflows of the Canadian unit it generates. As such, rising oil prices lead to strong inflows of Canadian Dollars, thereby causing it to strengthen versus the US Dollar. On the other hand, falling oil prices reduces inflows of Canadian Dollars, thereby causing it to depreciate versus the US Dollar.

The chart above compares the price action of NYMEX Crude oil (top panel) with that of USD/CAD (bottom panel) since 1994. Observe how the two tend to move in the opposite direction. Closely observe the arrow in the top panel with the corresponding arrow in the bottom panel. You will notice that a top in one usually coincides with a bottom in the other, and vice versa. See that there is often a tendency for USD/CAD to top out or bottom out just prior to crude oil bottoming out or topping out. Hence, occasionally, movement in USD/CAD can give signals about what could happen in crude oil. One can use this correlation between the two to his/her advantage.

Gold and AUD/USD

From a long-term perspective, there has been a positive correlation between Gold and AUD/USD. The two tend to move in sync most of the time. The reason for the existence of this correlation is because Australia is a major producer and exporter of the yellow metal. Itis the second largest gold producing nation in the world and gold forms a major component of the nation’s export bill. In 2019, it produced a record 325 tons of gold, which is equivalent to around 9% of the global output. Because of this, the Australian Dollar is notably impacted by the direction of gold prices.

The chart above compares the price action of Gold (top panel) with that of AUD/USD (bottom panel) since 2000. Observe how the two tend to move in the same direction. Closely observe the arrow in the top panel with the corresponding arrow in the bottom panel. You will notice that a top in one usually coincides with a top in the other, and vice versa. Meanwhile, see the region highlighted in the shaded box. This represents a period when the positive correlation broke, as gold prices strengthened while AUD/USD weakened. A major reason for the breakdown of the correlation during this period was a slowing Chinese economy. China is Australia’s biggest trading partner and in 2019, it accounted for nearly a third of Australia’s exports revenue. Consequently, a slowdown in China has had a negative impact on the Aussie Dollar. Since March 2020 however, the correlation has again turned positive. While the correlation can break from time to time, from a longer-term perspective, it tends to hold very well. Hence, one must continue monitoring the correlation between gold and AUD/USD. If it stays positive going forward, then one can use this correlation to his/her advantage.

Gold and USD/JPY

There is a negative correlation between gold and USD/JPY. That is, a rise in one is usually accompanied by a fall in the other, and vice versa. Because the two move in the opposite direction, it means gold and the Japanese Yen usually tend to move in the same direction. The reason why this happens is because of global risk flows. We know by now that during times of risk aversion, gold tends to perform well; and during times of economic strength, gold tends to underperform. Currencies also exhibit such a relationship. There are currencies that benefit during times of economic strength because foreign money tends to flow into these nations to seek growth. Examples include commodity and emerging market currencies. Then there are some that benefit during times of economic weakness and volatility because foreign money tends to flow into these nations to seek refuge in safer assets, such as government bills and bonds. The Japanese Yen is one such currency that tends to strengthen during times of economic weakness and volatility. As a result, gold and Yen often tend to move in sync.

The chart above compares the price action of Gold (top panel) with that of USD/JPY (bottom panel) since 2000. Observe how the two tend to move in the opposite direction. Closely observe the arrow in the top panel with the corresponding arrow in the bottom panel. You will notice that a top in one usually coincides with a bottom in the other, and vice versa. Meanwhile, see the region highlighted in the shaded box. This represents a period when the inverse correlation broke, as gold prices strengthened while USD/JPYalso headed higher.

Copper and USD/CLP

There is an inverse correlation between copper and USD/CLP. That is, a rise in one is usually accompanied by a fall in the other, and vice versa. CLP stands for Chilean Peso and is the currency of Chile. The reason for the existence of this correlation is because Chile is the largest producer and exporter of copper in the world. In 2019, its copper mine production is estimated to have stood at 5.6 million tons, which is just less than a third of the global copper production. As per a report by Sustainable Copper, copper mining has accounted for an average of 10% of Chile’s GDP over the past two decades. As copper exports contribute a lot to Chile’s export revenues, the Chilean peso is notably impacted by the direction of copper prices.

The chart above compares the price action of Copper (top panel) with that of USD/CLP (bottom panel) since 2004. Observe how the two tend to move in the opposite direction. Closely observe the arrow in the top panel with the corresponding arrow in the bottom panel. You will notice that a top in one usually coincides with a bottom in the other, and vice versa.

Next Chapter

Comments & Discussions in

FYERS Community

Akshat Rohatgi commented on August 6th, 2020 at 9:00 PM

Interesting!

Abhishek Chinchalkar commented on August 7th, 2020 at 8:02 AM

HI Akshat, thank you!