We will now discuss about the currencies of the five major Emerging market economies of the world. Collectively, these economies as abbreviated as BRICS wherein ‘B’ stands for Brazil, ‘R’ stands for Russia, ‘I’ stands for India, ‘C’ stands for China, and ‘S’ stands for South Africa. Each of these economies are known for their high-growth rates, high inflation, high population, and relatively low labour and production costs. Because of these aspects, the BRICS economies are a major source of foreign investment, given their huge growth potential. In this chapter, we will talk about each of the currencies of these nations relative to the Dollar.

The BRICS currencies

USD/CNY

This is the currency pair that pits the world’s largest economy with the world’s second largest economy. Combined, the US and China account for nearly two-fifth of the world GDP. Hence, movements in the currency pair has a strong impact on the health of the world economy. As we mentioned in an earlier chapter, the value of USD/CNY was fixed by China between 1994 and 2005. Post 2005 however, China switched its exchange rate system from fixed to managed float, wherein it gradually permitted its currency to strengthen against the dollar for almost a decade. In 2014, the appreciation of the Yuan came to an end and since then, the currency has gradually depreciated against the dollar. Recently, the PBoC, for the first time in over a decade, permitted the Yuan to weaken beyond 7 per dollar (i.e. allowed the pair to move above 7).

Because of the huge size of the Chinese exports, the Chinese government closely monitors and manages the Yuan, in order to prevent the currency from swinging sharply which could otherwise threaten the nation’s exports. Movement in the pair has a strong influence on the global markets and on risk sentiment. A rising USD/CNY tends to put downward pressure on risk assets such as global equities. This is because a rising USD/CNY (or in other words, a weakening Yuan) can lead to capital outflows from China and make Chinese exports cheaper, which in turn tends to hurt other major exporting nations of the world, including the US. On the other hand, a falling USD/CNY tends to underpin risk assets. This is because a falling USD/CNY (or in other words, a strengthening Yuan) makes investments in China more attractive and increases the competitive advantage of other major exporting nations, in turn boosting the global trade. Hence, movements in USD/CNY tend to have a strong impact on the global money flows.

Also, the trend of USD/CNY has an influence on the trends of most emerging market currencies too. For instance, a weakening Yuan (i.e. a rising USD/CNY) leads to depreciation among other emerging market currencies as well, as global investors withdraw their capital from riskier markets and find refuge in safer currencies, such as among the JPY and the CHF crosses. As a result of all this, it is imperative to say that one must keep a close watch on this pair. A break above or below a key technical level, for instance, can have a strong impact on the world markets and on various other currency pairs too, especially the commodity-driven and emerging-market currencies.

Some of the key factors to keep a track of when monitoring the pair include:

-

The Fed meeting and its policy guidance.

-

Periodic announcements by the PBoC on monetary policy.

-

The daily fixing price of the USD/CNY, in terms of whether the PBoC is permitting the pair to strengthen or weaken.

-

Key economic data from the US and China, with special emphasis on Chinese GDP, manufacturing PMI, and trade balance report.

-

News flows and major economic development in each of the two regions.

USD/INR

The USD/INR currency pair pits the world’s largest economy with the world’s fastest growing economy. The pair is heavily impacted by global events and risk flows. Positive global risk sentiment tends to drag the pair lower, while negative global risk sentiment tends to lift the pair higher. India is an import-driven economy, with crude oil being the largest component of its import bill. Hence, rising crude oil prices increase India’s import bill, which tends to increase the nation’s current account deficit and thereby causes the pair to appreciate. Similarly, falling crude oil price decreases India’s import bill, in turn reducing the nation’s current account deficit and causing the pair to depreciate. Hence, the price trend of crude oil has a strong influence on the trajectory of the USD/INR pair.

Movement in the pair is also influenced by the trajectory of the dollar against the emerging market currencies. If the dollar is strengthening against the emerging market currencies, chances are that it will strengthen against the Rupee as well. Similarly, if the dollar is weakening against the emerging market currencies, it will usually weaken against the Rupee as well. To monitor the trends of the Dollar, one must closely monitor the economic health of the US. Strengthening US economy would cause the Dollar to strengthen and the interest rate differential between the US and emerging markets nations to reduce, which in turn would pressurize emerging market currencies and subsequently the Rupee as well. Similarly, weakening US economy would cause the Dollar to weaken and the interest rate differential between the US and emerging markets to widen, which in turn would benefit emerging market currencies and subsequently the Rupee as well.

As already stated above, interest rate differential plays a crucial role in determining the direction of the pair. If the interest rate differential between the US and India widens, India’s assets, such as bonds, become more attractive because of the relatively higher returns that they offer. This usually leads to more foreign inflows into India, leading to a depreciation in the value of USD/INR. Similarly, if the interest rate differential between the US and India narrows, Indian assets become less attractive because of the reducing risk premium of investing in India. This usually leads to foreign outflows from India, causing an appreciation in the value of USD/INR. Hence, it is necessary to monitor how the interest rate differential between the US and India is moving.

Some of the key factors to keep a track of when monitoring the pair include:

-

The RBI and the Fed monetary policy meeting.

-

The policy guidance of each of the two central banks.

-

The trajectory of the interest rate differential between the two regions.

-

Movement in the price of crude oil.

-

Key economic data from the US and India.

-

The trajectory of the Dollar against other emerging-market currencies.

-

Prevailing risk sentiment in the market. The pair tends to rally when risk appetite is weak, and vice versa.

USD/BRL

The USD/BRL pair pits the largest economy in the world with the largest economy in Latin America, Brazil. Brazil is a country that is very rich in natural resources and is known for having largedeposits of tin, iron ore, manganese, copper, bauxite, gold, diamonds, and various other minerals, making the nation a mining giant. Besides being known for mining, Brazil is known for manufacturing and agriculture too. It is an export-driven economy that is renowned for exporting several commodities including metals and agricultural produce as well as manufactured products and automobiles. The pair is known for its volatility because of very high inflation and interest rates prevalent in Brazil.

USD/BRL currency pair is quite sensitive to fluctuations in commodity prices, considering that Brazil is a major exporter of several commodities. Hence, the trend of commodities has a strong influence on the pair. Generally, rising commodity prices is bearish for the pair, while falling commodity prices is bullish. The pair is also quite sensitive to economic developments in Brazil and among Brazil’s neighbouring nations. Latin America as a region has witnessed a lot of economic and political instability over the years. This in turn has caused the currencies of nations within this region to weaken markedly against the Dollar and USD/BRL has been no exception to this. Since the start of the decade, the pair has nearly tripled in value because of political unrest in Latin America, recession in Brazil between 2015 and 2016,rising unemployment in the nation, and Brazil’s ballooning national debt, which has surged to almost 80% of the nation’s GDP. Hence, a major factor that influences the trajectory of the pair is news flows pertaining to the economic situation in Brazil and its neighbouring countries. Generally, worsening economic situation in Brazil and its neighbouring nations lifts the pair higher, while improving economic situation drags the pair lower.

Some of the key factors to keep a track of when monitoring the pair include:

-

The BCB (Banco Central Do Brazil) and the Fed monetary policy meeting.

-

The policy guidance of each of the two central banks.

-

The trajectory of the interest rate differential between the two regions.

-

Movement in the price of commodities, in general.

-

Key economic data from the US and Brazil.

-

The trajectory of the Dollar against emerging-market currencies.

-

The trajectory of the Dollar against Latin American currencies.

-

The economic and political situation in Brazil and its neighbouring countries.

Prevailing risk sentiment in the market. The pair tends to rally when risk appetite is weak, and vice versa..

USD/RUB

The USD/RUB currency pair pits the currency of the US with that of Russia. The pair is closely impacted by the price trends of crude oil and natural gas as Russia is a major producer and exporter of these commodities. In fact, Russia is the second largest producer and exporter of crude oil as well as the second largest producer and the largest exporter of natural gas in the world. These commodities together contribute to more than half of Russian exports. Hence, movement in USD/RUB is heavily influenced by the price trend of energy commodities, especially crude oil. Rising crude oil prices is negative for the pair, while falling crude oil prices is positive for the pair. Besides, Russia is known for exporting various other commodities, such as iron, steel, copper, nickel, aluminium, gold, palladium etc. Being a resource-rich country that exports various commodities, the price trajectory of commodities influences the trend of the USD/RUB pair.

The pair is also impacted by the economic health of Europe and Asia. This is because most of Russia’s exports go to these two continents. In fact, as per 2018 figures, 92% of the Russian exports went to Europe (56%) and Asia (36%). As a result, the economic health of Europe and Asia plays a key role in impacting the trajectory of USD/RUB. Stronger European and Asian economy is negative for the pair, while weaker European and Asian economy is positive for the pair. The other factor that has a bearing on the currency is geopolitical developments. For instance, in 2014, the US and the EU imposed economic sanctions on Russia following Russia’s annexation of Crimea. Thesesanctions led to a sharp appreciation in USD/RUB, with the pair more than doubling in a matter of 6 months. Because of Russia’s frequent geopolitical conflict with the US and to some extent even with the EU, movements in the currency pair can become quite volatile occasionally. Hence, geopolitics has a strong say in impacting the price trajectory of the pair.

Some of the key factors to keep a track of when monitoring the pair include:

-

The CBR (Central Bank of the Russian Federation) and the Fed monetary policy meeting.

-

The policy guidance of each of the two central banks.

-

The trajectory of the interest rate differential between the two regions.

-

Movement in the price of commodities, especially crude oil.

-

Economic health of Europe and Asia, as these continents account for more than 90% of Russian exports.

-

Key economic data from Russia and the US.

-

The trajectory of the Dollar against emerging-market currencies.

-

The geopolitical development between Russia, the US, and to some extent even the EU.

-

Prevailing risk sentiment in the market. The pair tends to rally when risk appetite is weak, and vice versa.

USD/ZAR

The last of the BRICS currency pair that we would be talking about is USD/ZAR, i.e. the currency of the US and that of South Africa. This is a quite volatile pair due to the fragile health of the South African economy. The nation has an exceptionally high unemployment rate (29% as of 2019), a very high fiscal deficit (around 60% of the nation’s GDP), and an uneven rate of economic growth. The nation relies heavily on the exports of precious metals such as gold, platinum, and palladium. Softer prices of precious metals over the past few years have hurt the nation’s trade prospects. As a result of all these, the USD/ZAR pair has been on an upward trajectory for most of this decade.

Given the precarious state of the South African economy, the pair is quite sensitive to the global risk flows. Weakening risk sentiment tends to lead to an appreciation in the pair, while strengthening risk sentiment tends to lead to a depreciation in the pair. This is because during times of global uncertainties, capital tends to move out of South Africa, while during times of global strength and a strong South African economy, capital moves into South Africa. Besides, movement in the pair is also impacted by the trend of crude oil prices, given that the nation is a net importer of oil and its products. Rising oil prices tend to put upward pressure on the nation’s inflation, which in turn reduces the allure for the nation’s assets and thereby leads to the pair moving higher. Similarly, falling oil prices tend to lower nation’s inflationary pressures, which in turn leads to the pair moving lower.

Also, the pair is impacted by the general risk sentiment that is prevailing towards the outlook of the emerging markets. If the Dollar is strengthening against the emerging market currencies, then the USD/ZAR pair tends to strengthen even more, given that the South African economy is one of the weakest among the BRICS economies.

Some of the key factors to keep a track of when monitoring the pair include:

-

The SARB (South African Reserve Bank) and the Fed monetary policy meeting.

-

The policy guidance of each of the two central banks.

-

The trajectory of the interest rate differential between the two regions.

-

Movement in the prices of precious metals, in general.

-

Movement in the price of crude oil.

-

Key economic data from the US and South Africa.

-

The trajectory of the Dollar against emerging-market currencies.

-

Prevailing risk sentiment in the market. The pair tends to rally when risk appetite is weak, and vice versa.

Historical Charts

The above chart compares USD/CNY (blue line) with S&P 500 index (orange line). Notice the three highlighted regions. Observe here that a weakening Yuan (rising USD/CNY) led to a decline in the S&P 500 index, either with a time lag or without it, on each of the three occasions. Movements in the USD/CNY pair often influence the price trajectory of risk assets, such as equities and emerging market currencies. Hence, one must monitor movements in the Yuan against the Dollar, as it tends to strongly influence the trajectory of the world markets.

The above chart compares USD/CNY (blue line) with Thomson Reuters CRB index (orange line). Notice that since 2014, the steadily declining price trend among commodities has coincided with a steady depreciation of the Yuan (i.e. appreciation of USD/CNY). Given that China is the world’s largest consumer of several commodities, a weakening Yuan tends to hurt commodity prices, and vice versa. Also notice in the chart that the brief strengthening of the Yuan from early 2017 to early 2018 coincided with a recovery in commodity prices.

The above chart compares USD/INR (orange line) with USD/CNY (blue line). Notice the strong positive correlation that exists between the two pairs. Since 2018, the Yuan has been on a depreciation trajectory against the Dollar. This in turn has led to a weakening of most of the Emerging market currencies as well, and the Rupee has been no exception. While there are various other factors that impact the Rupee, including India’s own macro-economic fundamentals, the importance of the Yuan cannot be neglected in influence the broader trend of the Rupee.

The above chart compares USD/RUB (blue line) with Brent crude oil (orange line). Notice here that the broader trend of crude oil has a strong impact on the broader trend of the Russian Ruble. Russia is the one of the largest producers and exporters of crude oil, and a significant portion of Russia’s export revenues comes from the exports of crude oil. Hence, movements in the price of oil has a strong influence of the Ruble. As can be seen above, the plunge in oil price from 2014 to 2015 caused a massive depreciation of the Ruble against the dollar. Since then, the stabilization of oil prices has led to the stabilization of the Ruble as well.

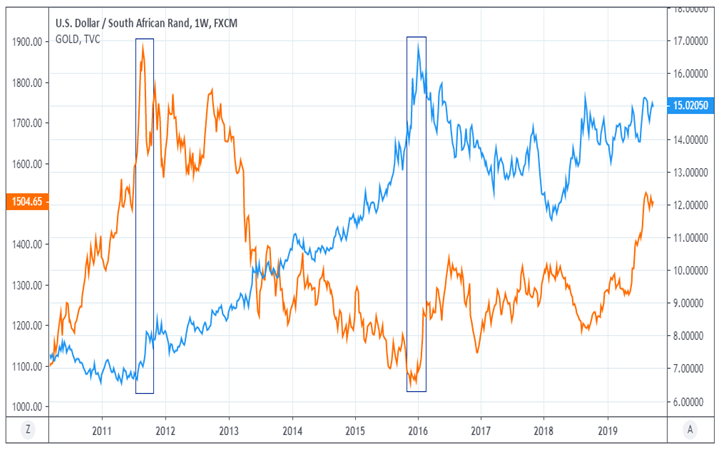

The above chart compares USD/ZAR (blue line) with the price of gold (orange line). Notice here that a major top in gold price in 2011 and a subsequent decline till 2015 coincided with a major bottom in USD/ZAR and a subsequent rally till 2015. Since then, the recovery in gold prices has caused the USD/ZAR pair to retreat. The reason for the existence of this correlation is that South Africa is a key producer and exporter of precious metals, such as gold, platinum, and palladium. Hence, a rally in the price of precious metals tends to benefit the South African Rand, while weakness in precious metals tends to pressurize the Rand.

Next Chapter

Comments & Discussions in

FYERS Community