.png)

Over the course of next two chapters, we will speak about currency derivatives that are traded on Indian exchanges. These include futures and options on currencies. In this chapter, the focus would be on currency futures; while in the next chapter, the focus would be on currency options.

Basic Definitions

Before proceeding any further, let us briefly understand a few basic, yet crucial concepts.

Derivatives

A derivative instrument, as the name suggests, is an instrument whose value is derived from the value of another instrument, called the underlying asset. This underlying asset could equity, index, currency, commodity, bond, interest rate etc. There are various types of derivative instruments that are traded around the world, both in the OTC (Over-the-Counter) markets as well as on exchanges. The agenda of this (and the next) chapter is to speak about currency derivative instruments that are traded on the Indian exchanges. These instruments include futures and options.

Forward

A forward is the most basic derivative contract. It is an agreement between two parties, a buyer and a seller, to buy or sell the underlying asset at a pre-determined price on some pre-specified day in the future. While one party to a forward transaction assumes the long trade, the other party assumes the short trade.Forward contracts are Over-the-Counter (OTC) contracts, meaning they are traded outside of exchanges. A major advantage of trading a forward contract is that it can be customised as per the requirements of the two parties. A major drawback of trading a forward contract, however, is the risk of default by one of the two counterparties.Forward contracts are extremely popular in the FX market across the world. In fact, in the Forex market, the daily volumes of forward contracts are significantly higher than those of futures contracts.

Futures

A futures contract is similar to a forward contract, with one distinction - it is traded on an exchange. A futures contract is an agreement between two partiesto buy or sell the underlying asset at a certain price on or before a certain future date. The price and the date on which the contract would be settledin future is mentioned on the futures contract.Because futures contract is traded on an exchange, it is a standardized contract wherein the features of the contract, such as expiry date, settlement date, lot size, tick size, margin requirement etc. are all defined by the exchange and cannot be customized. The table below summarizes the differences between forward and futures contracts.

| Forward | Futures |

| Private contracts between two parties | Exchange traded contracts |

| Customized contracts | Standardized contracts |

| Element of counterparty risk | No element of counterparty risk |

| Settled at the end of the contract | Settled every day (mark-to-market) |

| Less regulated instruments | Highly regulated instruments |

In India, most of the retail trading on currencies usually takes place in the futures and options segment. Trading inspot and forwards is usually restricted to large corporateentities and financial institutions.

Types of participants in the currency futures segment

In the first chapter, we already talked about the various types of participants in the Forex market. Let us highlight that again, but with emphasis on the futures segment this time around. Generally speaking, there are three types of participants who trade in the currency futures market. These are hedgers, speculators, and arbitrageurs. Let us briefly talk about each of them.

Hedgers

Hedgers are entities that have an underlying Forex exposure. They hedge this exposure by taking an offsetting position in the futures segment. Hedgers can include importers and exporters as well as other entities such as businesses and corporations.

Speculators

Speculators are entities whose main objective is to earn profits. They usually place short-term bets in the movements of currencies. If they are bullish on a currency pair, they will buy the pair and sell it at a future date; and if they are bearish on a currency pair, they will sell the pair and buy it back at a future date. Speculators vary in size - some could be very small, trading just a few dollars’ worth of currencies; while some could be very large, trading millions of dollars’ worth of currencies.

Arbitrageurs

Arbitrageursare those that trade with the objective of profiting from a price discrepancy that might exist among different markets/channels. They are in the business to make risk-free profit by buying a currency pair that is under-priced in one market and then selling the same currency pair that is over-priced in another market. Until the arbitrage opportunity disappears, arbitrageurs will continue to take advantage of the price discrepancy.

Currency futures traded on Indian exchanges

As already stated in the previous chapter, there are four currency pairs that are traded on the Indian bourses. These are USD/INR, EUR/INR, GBP/INR, and JPY/INR. Let us now talk about the contract specification of each of these currency pairs.

| Currency Pair | Trading Unit | Price Quote | Lot Size | Tick Size |

| USD/INR | $1,000 | ₹/$ | 1,000 | ₹0.0025 |

| EUR/INR | €1,000 | ₹/€ | 1,000 | ₹0.0025 |

| GBP/INR | £1,000 | ₹/£ | 1,000 | ₹0.0025 |

| JPY/INR | ¥100,000 | ₹/100¥ | 1,000 | ₹0.0025 |

The above table shows the basic contract specifications for currency futures that one needs to know.

Trading Unit

The trading unit refers to the minimum contract size that an entity is permitted to trade. For instance, if someone is buying 1 lot of USD/INR futures, it means he or she is taking exposure to the tune of $1,000 (1 * $1,000); while is someone is selling 10 lots of USD/INR futures, it means he or she is taking exposure to the tune of $10,000 (10 * $1,000).

Price Quote

The price quote refers to the way in which the currency pair is expressed. For instance, in case of USD/INR, the quote is expressed as Rupees per Dollar; while in case of JPY/INR, the quote is expressed as Rupees per 100 Japanese Yen.

Lot size

Notice in the table that each of the four pairs have the same lot size - 1,000. The lot size is calculated as trading unit * price quote. When we calculate profit/loss made on a trade, we multiply the difference between entry and exit price with the lot size traded to find out the profit or loss made on each trade, in Rupee terms.

Tick Size

Tick size is the minimum size by which the value of each currency pair can change at any point in time. For instance, the value of USD/INR futures, whenever it moves, changes by at least 0.25 paise (₹0.0025), or in multiples thereof. It cannot change by, say, 0.40 paise or 0.57 paise. Let us explain this using an example. If,

USD/INR October futures = 70.2025/70.2050

A 1 tick up move would cause the pair to rise to 70.2050/70.2075, while a 1 tick down move would cause the pair to drop to 70.2000/70.2025. Meanwhile, a 2 tick up move would cause the pair to rise to 70.2075/70.2100.

Each pair is quoted up to 4 decimal places

Notice how USD/INR is quoted above. Each of the four currency pairs traded on the Indian exchanges are expressed up to 4 decimal places, which is similar to the way other currency pairs in the world are expressed.

Let us now talk about the other contract specifications for the four currency futures pairs that are traded on Indian exchanges. Notice that as each of these specifications are same for each of the four pairs, we will just be talking about them in common rather than talking separately for each pair.

| Trade Timing | 9:00 AM to 5:00 PM, Monday to Friday |

| Contract Trading Cycle | Monthly, up to 12 month trading cycle |

| Last Trading Time &Day | 12:30PM, 2 working days before the expiry date of the contract |

| Final Settlement Day | Last working day of the expiry month |

| Margin | Initial + Maintenance |

| Settlement | Daily settlement on T+1 basis, Final settlement on T+2 basis |

| Mode of Settlement | Cash settled, in INR |

| Daily Settlement Price | Weighted average price for the last half hour of the trading session |

| Final Settlement Price | RBI reference rate on the final settlement day |

Let us now talk about these contract specifications in more detail:

Trade timing

The Indian currency markets are open between 9:00 AM and 5:00 PM from Monday to Friday. Trading does not take place over the weekends and on public holidays, which are disclosed by the exchange from time to time.

Contract Trading Cycle

The currency futures contracts are monthly contracts and follow a 12-month trading cycle. Hence, at any point in time, there would be 12 futures contracts that would be open on each of the four currency pairs. The near-month contracts, usually the first three months, are quite liquid; while the distant-month contracts are relatively less liquid. Generally speaking, as we move forward in time, the liquidity tends to decrease.

Last Trading Day

Each contract will expire two working days before the last working day of the month. For instance, if the last working day of October is the 31st, the October USD/INR futures contract would expire two working days prior to October 31st. Meanwhile, on the last trading day, the currency futures contracts would trade until 12:30 PM.

Final Settlement Day

The final settlement day is the last working day of the month. If any positions are open on this date for the contract that is expiring, the open positions would be closed out at the RBI reference rate of that day, and differences, if any, would be settled in cash.

Margin

There are two types of margin in the currency futures segment - initial and maintenance. Initial margin is the margin that is needed in the trading account when establishing a new position. Maintenance margin is the margin that must be maintained in the trading account post the creation of a new position. This is done for the purposes of marking-to-market, to ensure that none of the counterparties default.

How much margin is needed to open and maintain a position in currency futures can be found by clicking this link: https://fyers.in/margin-calculator/currency-futures/

Daily Settlement Price (DSP)

As the name suggests, DSP is the closing price for the day. It is calculated as the weighted average price for the last half hour of the trading session. The daily settlement, which occurs on a T+1 basis, is calculated using the DSP.

Final Settlement Price (FSP))

FSP is the settlement price for a futures contract on the last working day of the expiry month, which is also known as the Final Settlement Day. The RBI reference rate on the final settlement day is the Final Settlement Price of the expiring futures contract.

Calculating Profit/Loss on currency futures positions

Now that we have seen the contract specifications for each of the four currency futures contracts that are traded on Indian exchanges, let us see how profits/losses can be calculated for long/short positions in currency futures.

Calculating profit/loss on long positions

Let us take the example of USD/INR futures contract first. Let us assume that a trader is bullish on the pair and decides to buy 1 lot of USD/INR futures contract at 69.6575. In the next few days, the pair rose to, say, 70.0525, and the trader decided to close out his position. In this case, as the trader is closing out his long position at a higher price than the entry price, he has made a profit. This profit is calculated as follows:

(70.0525 - 69.6575) * 1,000 * 1 = ₹395

On the other hand, had the pair declined to, say, 69.0000, and had the trader closed out his long position at that rate, he would have made a loss. This loss can be calculated as follows:

(69.0000 - 69.6575) * 1,000 * 1 = -₹657.5

Let us now take another example. Let’s assume that a trader went long on 5 lots of JPY/INR futures at 65.0000. Let us say a week down the line, JPY/INR rallied to 67.0000 and the trader decided to exit the trade. In this case, the trader has profited:

(67.0000 – 65.0000) * 1,000 * 5 = ₹10,000

On the other hand, if the pair declined to, say, 64, and the trader decided to exit his long position. In this case, he would make a loss, which is calculated as follows:

(64.0000 – 65.0000) * 1,000 * 5 = -₹5,000

From this, we can generalize a formula to calculate profit/loss made on long positions in currency futures as follows:

Profit/loss on long position = (Exit rate – Entry rate) * lot size * number of lots

Notice here that the lot size is a fixed value of 1,000. What is variable is the entry rate, exit rate, and number of lots.

A positive figure indicates a profit, while a negative figure indicates a loss.

Calculating profit/loss on short positions

Let us take the example of EUR/INR futures contract first. Let us assume that a trader is bearish on the outlook of the pair and hence decides to short 7 lots of EUR/INR futures contract at 78.0000. In the next couple of days, the pair declines to, say, 75.0550, and the trader decided to close out his short positions. In this case, the trader’s profit can be calculated as follows:

(78.0000 - 75.0550) * 1,000 * 7 = ₹20,615

On the other hand, had the pair rallied to, say, 80.0000, and had the trader closed out his short position at that rate, he would have made a loss. This loss can be calculated as follows:

(78.0000 – 80.0000) * 1,000 * 7 = -₹14,000

From this, we can generalize a formula to calculate profit/loss made on short positions in currency futures as follows:

Profit/loss on short position = (Entry rate – Exit rate) * lot size * number of lots

A positive figure indicates a profit, while a negative figure indicates a loss.

Calculating the initial margin

Previously, we talked about how to calculate the profit/loss on currency futures positions. Let us now see how to calculate the initial margin that is needed in the account before building any new positions. As stated earlier, how much margin is needed to open and maintain a position in currency futures can be found by clicking this link: https://fyers.in/margin-calculator/currency-futures/

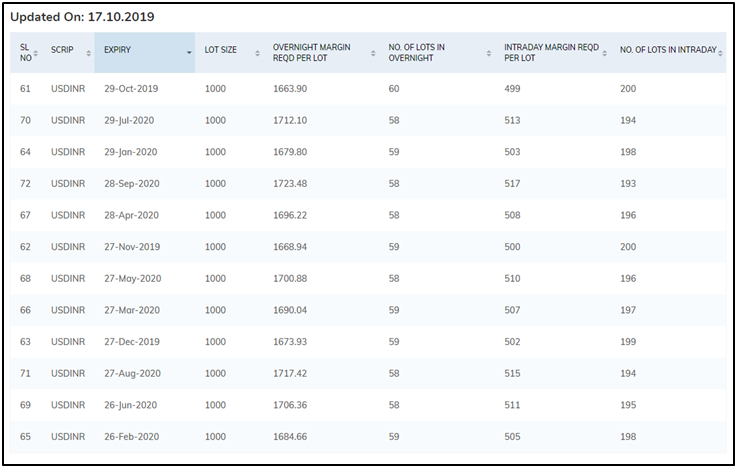

On this page, we can see that the margins are different for intraday positions (entry and exit on the same day) and for overnight positions (entry and exit on different days). Let us assume that a trader intends to keep his position open beyond the day when he or she entered the position. In that case, the overnight margin needed to trade 1 lot of USD/INR October futures is ₹1,663.90, as can be seen from the screenshot below taken from our margin calculator page.

Let us assume USD/INR October futures is currently trading at 71.50. In that case, the total value of the contract is 71.50 * 1,000 = ₹71,500. The overnight margin that is needed to open the position, as we saw in the table above, is ₹1,663.90. On a percentage basis, this turns out to be 1,663.90/71,500*100 = 2.33% of the total contract value.

So, the trader’s initial investment upfront is ₹1,663.90 per lot. His profit/loss on each lot can be expressed as a percent of the initial investment upfront. For instance, let us say that a trader initiates a long position by buying 5 lots of USD/INR October futures at 71.50. So, his total margin at the time of opening the position is ₹1,663.90 * 5 = ₹8,319.50. If on the next day, the pair rises to, say, 71.65 and he exits his position, he has made a total profit of ₹750 [(71.65 - 71.50) * 1,000 * 5]. His percentage return on the trade would be 9% (750/8,319.50*100). On the other hand, if on the next day, the pair declines to, say, 71.20 and he decides to close out his position at a loss, his total loss would amount to ₹1,500 [(71.20 - 71.50) * 1,000 * 5]. His loss on the trade as a percent of the capital deployed would be 18% (1,500/8,319.50*100).

Currency futures strategies

Earlier in the chapter, we said that there are three types of participants in the currency futures segment. These are hedgers, speculators, and arbitrageurs. Each of these participants have different set of objectives and risk profile. For instance, a hedger participates in currency futures segment not to make a profit but to hedge the underlying Forex exposure. On the other hand, a speculator trades in the currency futures segment with the only objective of making a profit by taking a directional view on currency. Meanwhile, an arbitrageur participates in the currency futures segment in order to profit from price discrepancy that exists between two segments, such as between spot and futures.

Let us now talk about some strategies using currency futures.

Hedging using currency futures

Ahedgerin the Forex market is someone who has an underlying currency exposure, such as someone who needs to pay foreign currency some point in the future or someone who would receive foreign currency some point in the future. To safeguard against the potential fluctuations in currency, a hedger takes an offsetting position in the derivatives segment, to eliminate or minimize the risk. The objective of the hedger is to safeguard against currency fluctuations rather than trying to profit from them.

Example 1: Hedging by an importer (Long Hedge)

Let us assume that there is a company in India, ABC Ltd, which is in the business of producing industrial equipments. To make these equipments, ABC Ltdimports certain parts from its US supplier. Let us suppose that the next import would take place on October 31st, 2019 to the tune of $1 million, the payment for which would be made 3 months down the line, i.e. on January 31st, 2020.What is the risk here? One of the biggest risk is the Forex exposure risk. Because ABC Ltd would be making payment in US Dollars a few months down the line, it is exposed to currency risk. It stands to lose if the Dollar appreciates in value over the next three months. Let’s see how this happens.

At the time of receiving the delivery (October 31st, 2019), let us suppose that USD/INR spot rate is 70. This means, as on October 31st,2019, ABC Ltd will be required to pay ₹7 crores ($1 million * 70) in order to receive $1 million from its bank, which would then be paid to the US supplier. But what if three months down the line, on January 31st, 2020, USD/INR has appreciated to 75? In that case, ABC will now have to pay ₹7.5 crores to receive the same $1 million ($1 million * 75). Hence, ABC Ltd would be paying an additional ₹50 lacs, because of the adverse movement in currency.

In order to safeguard against such risks, ABC Ltd could hedge its exposure using currency futures. As we already know, three months down the line, ABC Ltd would need $1 million, which translates to 1,000 lots of USD/INR futures (remember, 1 lot is $1,000; so, 1,000 lots are 1,000 * $1,000 = $1 million). As ABC Ltd needs to make payment on January 31st,2020 and hence is exposed to the risk of USD/INR appreciating till then, it could hedge by going long 1,000 lots of USD/INR January 2020 futures. Let us suppose that, currently, January 2020 USD/INR futures is trading at 71. By buying 1,000 lots at an average rate of 71, ABC Ltd has hedged itself against currency risk. Let us now see what could happen on January 31st, 2020.

If USD/INR appreciates to, say 75, as we have already seen earlier, ABC Ltd would lose ₹50 lacs in the spot segment [(70 - 75) * $1 million]. In the futures segment however, ABC Ltd would gain ₹4,000 per lot [(75 - 71) * 1,000 * 1], for a total gain of ₹40 lacs (₹4,000 per lot * 1,000 lots). In this case, its net loss would be ₹10 lacs (₹40 lacs gain in futures - ₹50 lacs loss in spot). On the other hand, if USD/INR depreciates to, say, 65, ABC would gain ₹50 lacs in the spot segment [(70 - 65) * $1 million]. In the futures segment though, ABC Ltd would lose ₹6,000 per lot [(65 - 71) * 1,000 * 1], for a total loss of ₹60 lacs (₹6,000 per lot * 1,000 lots). In this case, its net loss would be ₹10 lacs (₹50 lacs gain in spot - ₹60 lacs loss in futures).

As we can see, the loss is the same in both the cases (₹10 lacs).This is because ABC Ltd is essentially locking in the future exchange rate at 71 when the spot rate is 70. No matter where the currency heads till January 31st, 2020, ABC Ltd will make a fixed loss of ₹10 lacs, which is nothing but the difference between the spot price (70) and the futures price (71) at the time of initiation times the underlying exposure ($1 million).

Example 2: Hedging by an exporter (Short Hedge)

Let us say XYZ Ltd is in the business of exporting precious stones and one of its clients is in the US. XYZ has received an order from this US client to deliver certain stones on October 31st, 2019, the payment for which would be received by XYZ in US Dollars 2 months down the line, i.e. on December 31st, 2019. Let us assume that the value of USD/INR on October 31st is 70 in the spot market and that total value of the contract is $0.5 million. As the payment would be received 2 month down the line, XYZ is exposed to the risk of USD/INR depreciating over the next two months. For instance, if USD/INR drops to 66 by December 31st, ABC would realize ₹3.3 crores when it converts Dollars to Rupees on December 31st, as opposed to realizing ₹3.5 crores had USD/INR stayed unchanged at 70.

In order to safeguarding against Rupee appreciation, XYZ decides to short 500 lots of December 2019 USD/INR futures. Let us assume that the prevailing futures exchange rate is 70.50. Let us now see what could happen on December 31st, 2019.

If USD/INR appreciates to, say 75, XYZ Ltd would gain ₹25 lacs in the spot segment [(75 - 70) * $0.5 million]. In the futures segment however, ABC Ltd would lose ₹4,500 per lot [(70.50 - 75) * 1,000 * 1], for a total loss of ₹22.5 lacs (₹4,500 per lot * 500 lots). In this case, its net gain would be ₹2.5 lacs (₹25 lacs gain in spot - ₹22.5 lacs loss in futures). On the other hand, if USD/INR depreciates to, say, 65, XYZ would lose ₹25 lacs in the spot segment [(65 - 70) * $0.5 million]. In the futures segment though, XYZ Ltd would gain ₹5,500 per lot [(70.50 - 65) * 1,000 * 1], for a total gain of ₹27.5 lacs (₹5,500 per lot * 500 lots). In this case, its net gain would be ₹2.5 lacs (₹27.5 lacs gain in futures - ₹25 lacs loss in spot).

Again, the gain is the same in both the cases (₹2.5 lacs). This is because XYZ Ltd is essentially locking in the future exchange rate at 70.50 when the spot rate is 70.

Speculating using currency futures

Unlike a hedger, a speculator does not have any underlying exposure in the Forex market. Instead, a speculator trades with the sole objective of trying to make money by taking a directional view on the currency and assuming risk thereon. Let us try to understand how a speculator trades using currency futures.

Example 1: Long position in USD/INR futures

Let us assume that Mr. A is bullish on the outlook of USD/INR due to his expectations that the interest rate differential between India and US will shrink, leading to Dollar outflows from India. As a result, he decides to initiate a long position on 50 lots of USD/INR futures contract at CMP 70.0000 and hold it till the expiry of the contract. If his view holds true and USD/INR futures rallies to, say, 72.0000 by expiry, he would exit his long position and profit ₹100,000 [(72.0000 - 70.0000) * 1,000 * 50]. However, if his view does not materialize and USD/INR futures drops to, say, 69.0000 by expiry, he would exit his long position and lose ₹50,000 [(69.0000 - 70.0000) * 1,000 * 50].

Example 2: Short position in USD/INR futuress

Let us assume that USD/INR has given a technical breakdown on the daily chart, because of which Mr. B has turned bearish on the short-term outlook of USD/INR. As a result, he decides to initiate a short position on 10 lots of USD/INR futures contract at CMP 70.0000 and hold it over the next few days. If his view holds true and USD/INR futures declines to, say, 68.8000 in the next few days, he would exit his short position and profit ₹12,000 [(70.0000 - 68.8000) * 1,000 * 10]. However, if his view does not materialize and USD/INR futures rises to, say, 70.5000 in the next few days, he would exit his short position and lose ₹5,000 [(70.0000 - 70.5000) * 1,000 * 10].

So, as we can see, a speculator takes a view on the currency pair, assumes all the risk involved, and takes position(s) depending on whether he or she is bullish (in which case a long position would be taken) on the pair or bearish (in which case a short position would be taken) on the pair.

Next Chapter

Comments & Discussions in

FYERS Community

Pragya commented on October 24th, 2019 at 7:25 PM

How does Forex market differ from other markets?

Shriram commented on January 28th, 2020 at 10:23 PM

Hi Pragya, to understand the difference between Forex market and other markets, we suggest that you go through the earlier chapters in this module.

Gajanan commented on October 24th, 2019 at 11:02 PM

If we trade in CNY/INR profit and loss will be calculated based on Dollar price or Not?

tejas commented on November 6th, 2019 at 11:31 PM

Hi Dasharath, Your P&L will be obviously calculated in INR.

Dasharath Singh commented on October 24th, 2019 at 11:11 PM

For normal retail currency traders, is there any hedging options for USD/INR positions with any other currency pairs? Please explain about hedging options/strategies for normal traders.

Shriram commented on January 28th, 2020 at 10:24 PM

Hi Dasharath, kindly go through the next chapter, which is on Currency Options. Also, we will soon be coming out with Options Strategy module. So stay tuned...

Bikash commented on October 29th, 2019 at 4:32 PM

USDINR appreciating and equity market as well. How to analyze the future of the equity market under this situation.This Divergence raises some question, whether there is any relation between INR strength and equity market over a long period.

Shriram commented on January 28th, 2020 at 10:28 PM

Hi Bikash, there are times when the two diverge. Remember that there are various factors that impact USDINR, and equities is just one of them. In fact, FX trends in emerging markets, global interest rates, and central bank policy actions often tend to have more impact on USDINR than just the Indian equity markets.

tejas commented on November 6th, 2019 at 11:30 PM

Hi Pragya, Make sure to read the first three chapters in the Currencies Module. I am sure you will understand the difference :-)

ABHISHEK commented on January 5th, 2020 at 5:54 PM

While going through NSE website I found this interesting table.. in the row of calander spreads I found few rates, does this mean that these are the average rates of calenders spread and we can take this as a guideline for futures bull/bear spread. Please find the link

https://www1.nseindia.com/products/content/derivatives/curr_der/cd_contract_specifications.htm

ABHISHEK commented on January 5th, 2020 at 5:54 PM

While going through NSE website I found this interesting table.. in the row of calander spreads I found few rates, does this mean that these are the average rates of calenders spread and we can take this as a guideline for futures bull/bear spread. Please find the link

https://www1.nseindia.com/products/content/derivatives/curr_der/cd_contract_specifications.htm