In the previous chapter, we talked about currency futures. We discussed about things such as basic definitions relating to futures, types of market participants in the currency futures segment, contract specifications of currency futures on Indian exchanges, and lastly about the mathematical part of currency futures. The focus of this chapter is to talk about currency options that are traded on the Indian bourses. These include options on USD/INR, EUR/INR, GBP/INR, and JPY/INR pair. We will focus mostly on USD/INR options, given that options on the other three pairs are quite illiquid as of today.Having said that, before reaching there, we will start with the basic definitions related to options and then proceed to talk about the contract specifications and the mathematics of currency options.

Basic Options Terminologies

Option: An options contract is a contract that gives the buyer the right, but not an obligation, to buy or sell an asset at a specific time in the future for a specific price, called the strike price. Options are of two types: call options and put options.

Call option: A call option gives the buyer the right to buy the underlying asset in the future for a specific strike price

Put option: A put option gives the buyer the right to sell the underlying asset in the future for a specific strike price.

Strike price:Strike price is an agreed upon price at which the underlying asset will be bought (in case of a call option) or sold (in case of a put option) on the expiration day.

Option price: Also known as option premium, option price is the price that an option buyer must pay to an option seller for acquiring the right to the contract. It comprises of two components – intrinsic value and time value.

Option Price (or premium) = Intrinsic Value + Time Value

Moneyness of an Option: Moneyness of an option tells where the position of the spot price is relative to the strike price. At any point in time, an option could be in-the-money, at-the-money, or out-of-the-money.

In-the-money (ITM) option: A call option is said to be ITM if the current price of the underlying is above the strike price, while a put option is said to be ITM is the current price of the underlying is below the strike price.

At-the-money (ATM) option: A call/put option is said to be ATM if the current price of the underlying is equal to the strike price.

Out-of-the-money (OTM) option: A call option is said to be OTM if the current price of the underlying is below the strike price, while a put option is said to be OTM if the current price of the underlying is above the strike price.

Intrinsic value of an option: This refers to the amount an option contract is ITM. If the option is OTM, intrinsic value is zero. For a call/put option that is ITM, intrinsic value is calculated as the absolute value of the difference between the current price of the underlying and the strike price.

Time value of an option: This is the difference between the option price and the intrinsic value. If an option is OTM, option price is equal to time value (as intrinsic value is zero). The greater the time to expiration, the higher will be the time value, and vice versa.

Breakeven price: This is the price at which the buyer of an option will be at breakeven, i.e. neither making a profit nor a loss. For a call option, the breakeven price is equal to strike price plus the premium paid by the buyer; while for a put option, the breakeven price is equal to strike price minus the premium paid by the buyer.

Breakeven Price for Call Option = Strike price + option premium

Breakeven Price for Put Option = Strike price - option premium

Contract Specification of USD/INR options

The table below shows the contract specifications for USD/INR options contract:

| Trade Timing | 9:00 AM to 5:00 PM, Monday to Friday |

| Option Type | European Call and Put options |

| Option Premium | Quoted in INR |

| Trading Unit | 1 contract = $1,000 |

| Tick size | ₹0.0025 |

| Strike Price intervals | ₹0.25 |

| # of strikes | Minimum 25 Calls and 25 Puts at any point in time (12 ITM, 12 OTM, and 1 near-the-money) |

| Contract Cycle | 3 monthly contracts followed by 3 quarterly contracts |

| Settlement | Daily Settlement: T+1 basis, Final Settlement: T+2 basis |

| Mode of Settlement | Cash Settled, in INR |

| Last Trading Time & Day | 12:30PM, 2 working days before the expiry date of the contract |

| Final Settlement Date | Last working day of the expiry month |

| Final Settlement Price | RBI Reference Rate on the expiry date |

Let us now describe talk about some of these aspects in more details

Option Type

The currency options that are available for trading on the Indian exchanges are European-style options. These are options that can be squared off at any time during the life of the contract but can be exercised only on the expiry date. The counterpart of the European-style option is the American-style option, which can be exercised by the buyer at any time. These options are, however, not traded on Indian exchanges.

Strike price intervals

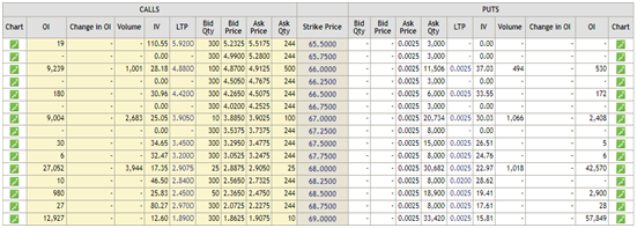

Currency options that are traded on Indian exchanges have a strike price interval of 25 paise. For example, USD/INR option contracts would have strike prices such as 70.0000, 70.2500, 70.5000, 72.7500 etc. Look at the table below (source: www.nseindia.com) wherein the centre column shows the strike price intervals for one series of USD/INR options.

Number of strikes: At any point in time, there would be 12 ITM options, 12 OTM options and 1 near-the-money option on both calls and puts, for a total of at least 25 call and put options.

Contract Cycle:The USD/INR options contract cycle consists of 3 serial monthly contracts that are then followed by 3 quarterly contracts. For instance, as of October 2019, the three serial monthly options contract listed are October 2019, November 2019, and December 2019 contracts; while the three quarterly options that are listed are March 2020, June 2020, and September 2020 contracts.

Hedging using USD/INR options

Let us now present a few hedging examples using USD/INR options contract.

Example 1: Hedging by an importer (Long Call)

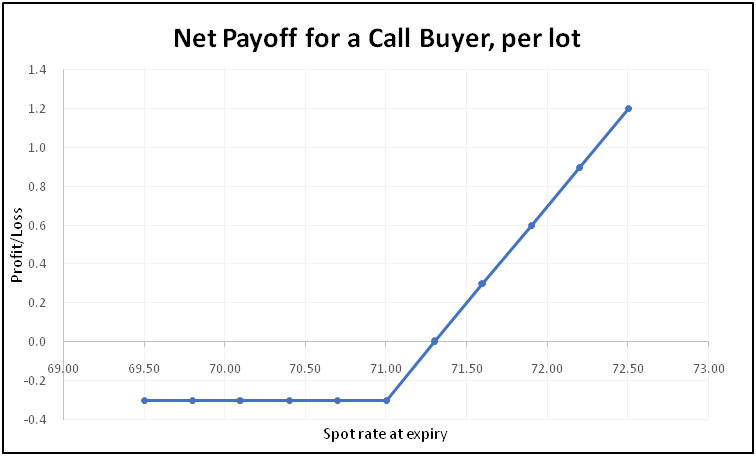

Let us assume an importer must pay $100,000 1-month from today. Let us assume that today is 1st November 2019 and that the payment would be made on 30th November 2019. Because the importer will have to make payment in US Dollars, he is exposed to the risk of dollar strengthening over the next one month. In order to safeguard against this risk, the importer decides to buy 100 lots of USD/INR November call options contract. Let us assume that the importer decides to buy at-the-money call options having strike price of 71 at the prevailing rate of ₹0.3 per option. As the importer would be buying 100 lots of call options, his total investment upfront would be ₹30,000 (option price of ₹0.30 per lot * lot size of 1,000 * number of lots of 100). The total that the importer stands to lose is his investment that he has made upfront, which is ₹30,000. Meanwhile, the Breakeven price for the importer would be 71.30 (strike price of 71.00 + option premium paid 0.30). The table below shows the per lot payoff of the importer.

| USD/INR spot price at Expiry | Net Payoff on long Call |

| 69.50 | -0.3 |

| 69.80 | -0.3 |

| 70.10 | -0.3 |

| 70.40 | -0.3 |

| 70.70 | -0.3 |

| 71.00 | -0.3 |

| 71.30 | 0.0 |

| 71.60 | 0.3 |

| 71.90 | 0.6 |

| 72.20 | 0.9 |

| 72.50 | 1.2 |

Notice from the above table that the maximum that the importer would stand to lose per lot is limited to the extent of premium that he has paid upfront. He achieves breakeven at 71.30, above which he starts making profit. The higher the spot rate goes above the breakeven rate, the greater would be the profit potential of the importer. From this, it can be seen that for a call buyer, losses are limited to the extent of premium paid, while profits are potentially unlimited. The chart below shows the visual representation of the long call payoff. Above the breakeven point, observe how the profit potential keeps rising for every up move in the underlying rate, or the spot rate.

Example 2: Hedging by an exporter (Long Put)

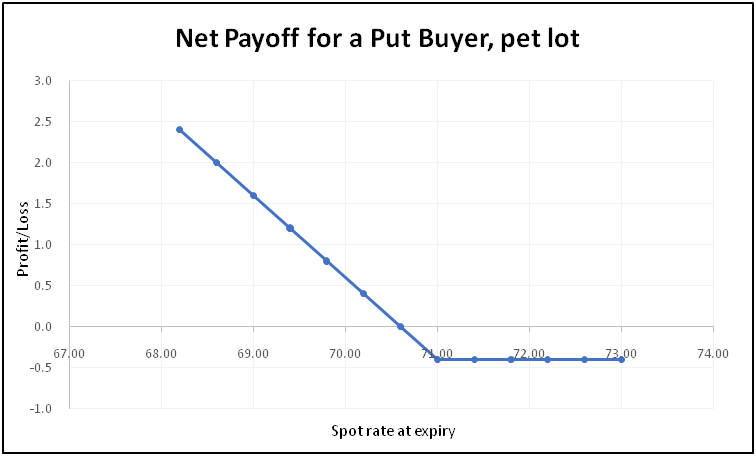

Let us assume an exporter will receive $100,000 1-month from today. Let us assume that today is 1st November 2019 and that the payment would be received on 30th November 2019. Because the exporter will receive payment in US Dollars, he is exposed to the risk of dollar weakening over the next one month. In order to safeguard against this risk, the exporter decides to buy 100 lots of USD/INR November put options contract. Let us assume that the exporter decides to buy at-the-money put options having strike price of 71 at the prevailing rate of ₹0.4 per option. As the exporter would be buying 100 lots of put options, his total investment upfront would be ₹40,000 (option price of ₹0.40 per lot * lot size of 1,000 * number of lots of 100). The total that the exporter stands to lose is his investment that he has made upfront, which is ₹40,000. Meanwhile, the breakeven price for the exporter would be 70.60 (strike price of 71.00 - option premium paid 0.40). The table below shows the per lot payoff of the exporter.

| USD/INR spot price at Expiry | Net Payoff on long Put |

| 68.20 | 2.4 |

| 68.60 | 2.0 |

| 69.00 | 1.6 |

| 69.40 | 1.2 |

| 69.80 | 0.8 |

| 70.20 | 0.4 |

| 70.60 | 0.0 |

| 71.00 | -0.4 |

| 71.40 | -0.4 |

| 71.80 | -0.4 |

| 72.20 | -0.4 |

| 72.60 | -0.4 |

| 73.00 | -0.4 |

Notice from the above table that the maximum that the exporter would stand to lose per lot is limited to the extent of premium that he has paid upfront. He achieves breakeven at 70.60, below which he starts making profit. The lower the spot rate goes below the breakeven rate, the greater would be the profit potential of the exporter. From this, it can be seen that for a put buyer, losses are limited to the extent of premium paid, while profits are potentially unlimited (theoretically, until price drops to zero). The chart below shows the visual representation of the long put payoff. Below the breakeven point, observe how the profit potential keeps rising for every down move in the underlying rate, or the spot rate.

Example 3: Short Call

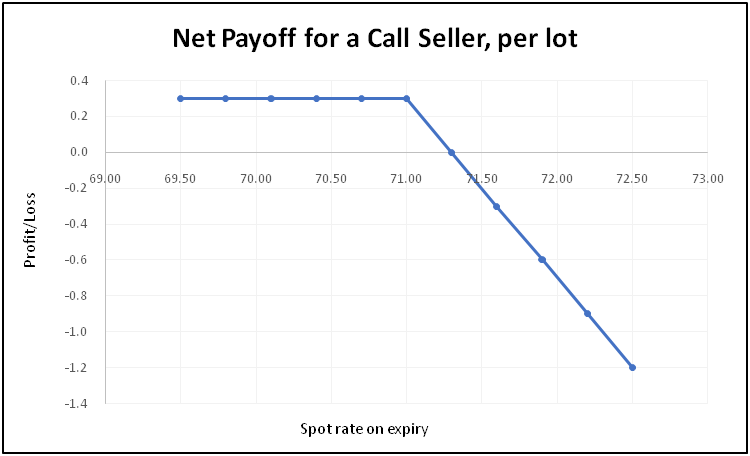

In case of a short call position, the profit would be limited to the extent of the premium received. That is the maximum the seller of a call option can earn. The loss to an option seller, on the other hand, would be potentially unlimited. So, taking the same example that we spoke above in case of a long call position, the maximum the writer of a call option could make is ₹0.3 per option contract, or ₹30,000 on 100 lots. As long as the spot price until expiration is below the breakeven price (strike price + premium received), the seller would make money. When the spot price, however, goes above the breakeven price, the seller would start incurring losses. Let us understand this with the help of a table.

| USD/INR spot price at Expiry | Net Payoff |

| 69.50 | 0.3 |

| 69.80 | 0.3 |

| 70.10 | 0.3 |

| 70.40 | 0.3 |

| 70.70 | 0.3 |

| 71.00 | 0.3 |

| 71.30 | 0.0 |

| 71.60 | -0.3 |

| 71.90 | -0.6 |

| 72.20 | -0.9 |

| 72.50 | -1.2 |

Notice from the above table that the seller would make money as long as the spot price is below the breakeven price. Once the spot price crosses above the breakeven price, the seller will start making losses, which could be potentially unlimited.The chart below shows the visual representation of the short call payoff.

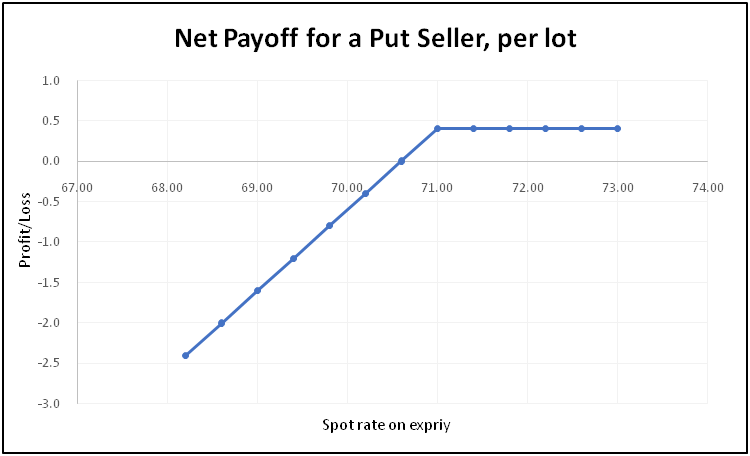

Example 4: Short Put

In case of a short put position, the profit would be limited to the extent of the premium received. That is the maximum the seller of a put option can earn. The loss to an option seller, on the other hand, would be potentially unlimited (theoretically limited as the spot price cannot drop below zero). So, taking the same example that we spoke above in case of a long put position, the maximum the writer of a put option could make is ₹0.4 per option contract, or ₹40,000 on 100 lots. As long as the spot price is above the breakeven price (strike price - premium received), the seller would make money. When the spot price, however, goes below the breakeven price, the seller would start incurring losses. Let us understand this with the help of a table.

| USD/INR spot price at Expiry | Net Payoff |

| 68.20 | -2.4 |

| 68.60 | -2.0 |

| 69.00 | -1.6 |

| 69.40 | -1.2 |

| 69.80 | -0.8 |

| 70.20 | -0.4 |

| 70.60 | 0.0 |

| 71.00 | 0.4 |

| 71.40 | 0.4 |

| 71.80 | 0.4 |

| 72.20 | 0.4 |

| 72.60 | 0.4 |

| 73.00 | 0.4 |

Notice from the above table that the seller would make money as long as the spot price is above the breakeven price. Once the spot price crosses underneath the breakeven price, the seller will start making losses.The chart below shows the visual representation of the short put payoff.

Some basic formulas to keep in mind

In the four examples that we presented above, it would help if certain formulas are kept in mind. These are as follows:

Long call option:

Breakeven point = strike price + premium paid

Payoff = Maximum of [(spot price - strike price), 0] - premium paid

Long Put option:

Breakeven point = strike price - premium paid

Payoff = Maximum of [(strike price -spot price), 0] - premium paid

Short call option:

Breakeven point = strike price + premium paid

Payoff = Premium received - Maximum of [(spot price - strike price), 0]

Short Put option:

Breakeven point = strike price - premium paid

Payoff = Premium received - Maximum of [(strike price -spot price), 0]

Capital required to trade currency options

Buyer of an option

The buyer of an option must pay the entire premium upfront when buying the option contract. This is calculated as follows:

Total premium payable by the option buyer = option price per lot * lot size * number of lots

So for instance, if the option price is ₹0.3 for a call having a strike of 71, a buyer who wants to buy 1 lot would have to pay a total premium of ₹300 (₹0.3 * 1,000 * 1); while a buyer who wants to buy 500 lots would have to pay a total premium of ₹150,000 (₹0.3 * 1,000 * 500).

Seller of an option

Selling an option is similar to selling a futures as far as the cash outflows at the time of selling the option are concerned. For instance, selling a call option means the seller will have to pay the initial margin upfront, the calculation of which is more or less similar to the initial margin that is paid when initiating a position in the futures segment. The only exception is that in case of options, the value of the premium received by the option seller is adjusted for in the initial margin.

Options vs. Futures

Let us conclude this topic by talking about the differences between an exchange-traded futures contract and an exchange-traded options contract. The differences are highlighted in the table below:

| Futures | Options |

| Buyer is obliged to honour the contract | Buyer has a right, but not an obligation to honour the contract |

| Selleris obliged to honour the contract | Seller has an obligation to honour the contract, if the buyer exercises his right |

| Profit potential for a buyer is unlimited | Profit potential for a buyer is unlimited |

| Profit potential for a seller is unlimited | Profit potential for a seller is limited to the extent of premium received |

| Buyer is exposed to unlimited risk | Buyer’s risk is limited to the extent of premium paid |

| Seller is exposed to unlimited risk | Seller is exposed to unlimited risk |

One advantage that an option contract has over a futures contract is that it allows the hedger to participate during favourable moves too, something which is not possible in case of a futures contract. For instance, let us assume that an importer would need to pay $100,000 1-month down the line. He has two options in front of him: buy 100 lots of futures contract or buy 100 lots of call options.

In case of options position, if the Dollar depreciates, the importer would lose to the extent of the option premium that he has paid, but he would gain on the spot segment, in which he would be making the payment. On the other hand, if the Dollar appreciates, the importer would gain in the options segment, which would help him offset the losses that he would make in the spot segment. So, as we can see, while options limit the losses, they do not limit the profit potential.

In case of futures position though, if the Dollar depreciates, the gains that the importer would make in the spot segment would be offset by the losses that he would suffer in the futures segment. Thus, the investor would stand a chance of making little to no gains when he hedges using futures. Put it simply, hedging using futures position would not only limit losses but would also limit gains; whereas hedging using options would limit losses but would not restrict gains in case of favourable price moves.

Next Chapter

Comments & Discussions in

FYERS Community

Bharath commented on July 3rd, 2020 at 5:26 PM

What is the underlying for usdinr options, spot or future? If spot, where do we get real time charts of spot for currencies?

Abhishek Chinchalkar commented on July 4th, 2020 at 8:24 AM

Hi Bharath, it is spot. You can check out the live spot rate for USD/INR on our FYERS Forex Widget platform. Meanwhile, Tradingview provides real time FX spot charts.