In the first part of the Currency module, we talked about the fundamentals of currencies wherein we discussed about aspects such as factors that impact currencies, analysing economic data and reports, the major, cross, and BRICS currencies, and an introduction to the Indian Forex market. Then in the second part of the Currency module, we talked about currency futures and currency options that are traded on Indian exchanges. Now, in the third part of the Currency module, we will be covering the intermarket, technical, and other aspects of currencies. Speaking of this chapter, we would be introducing and talking about intermarket analysis i.e. how movements across other classes affect currencies. For this, we will be discussing about how bonds, commodities, and equities impact the Forex market. But let us first classify currencies based on their risk profile, i.e. risk-on versus risk-off currencies.

Risk-on versus Risk-off currencies

Currencies that are traded around the world can be classified into two groups: risk-on currencies and risk-off currencies. Risk-on currencies are those that tend to appreciate when the risk sentiment is positive and depreciate when the risk sentiment is negative. These currencies usually belong to countries that offer high interest rates. A positive outlook on the health of the world economy benefits these currencies, as capital often tends to move from countries that have low interest rate to countries that have high interest rates during times of economic prosperity. Examples of such currencies include the commodity currencies (Australian dollar, Canadian dollar, New Zealand dollar, Russian Ruble, Brazilian Real etc.), currencies belonging to emerging market nations (Indian Rupee, Chinese Yuan, South Korean Won) etc. It is common for these currencies to strengthen against their Dollar during times of strengthening risk appetite and weaken against the Dollar during times of weakening risk appetite.

On the other hand, risk-off currencies are those that tend to appreciate when the risk sentiment is negative and depreciate when the risk sentiment is positive. These currencies usually belong to countries that offer a low interest rate and have economic stability as well. During times of positive global outlook, capital tends to move out of countries that offer low interest rates into those countries that offer high interest rates. As such, it is common for risk-off currencies to underperform their risk-on counterparts during times of global economic strength. Similarly, during times of global uncertainty and weakness, risk-off currencies tend to outperform their risk-on counterparts as there is a flight towards safety. Two of the most renowned risk-off currencies are the Japanese Yen and the Swiss Franc. The US dollar is another currency that can be considered risk-off, as it tends to strengthen against its counterparts during times when the global economic outlook is shaky.

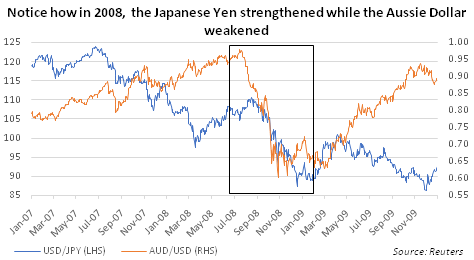

Notice in the chart above how the Australian Dollar depreciated against the US Dollar (declining AUD/USD line) in 2008. During this same period, observe how the Japanese Yen strengthened against the US Dollar (falling USD/JPY line). As the global financial crisis intensified during this period, capital flows shifted from high yielding countries, such as Australia, to low-yielding, haven countries, such as Japan. As a result, currencies of such high-yielding countries attracted strong selling pressure; while those of low-yielding countries were in relentless demand. While 2008 was an exceptional event, there is a tendency for currencies to behave in a similar manner during most of the times. Periods when the global economic prospects are bright tend to benefit risk-on, high-yielding currencies; while periods when the global economic prospects are bleak tend to benefit risk-off, low-yielding currencies.

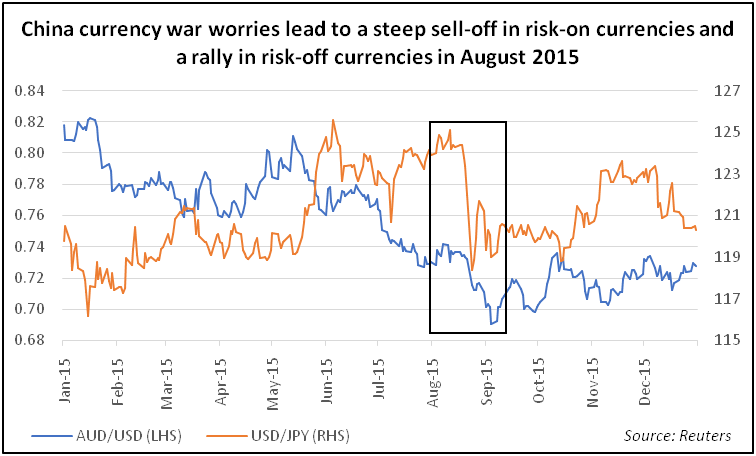

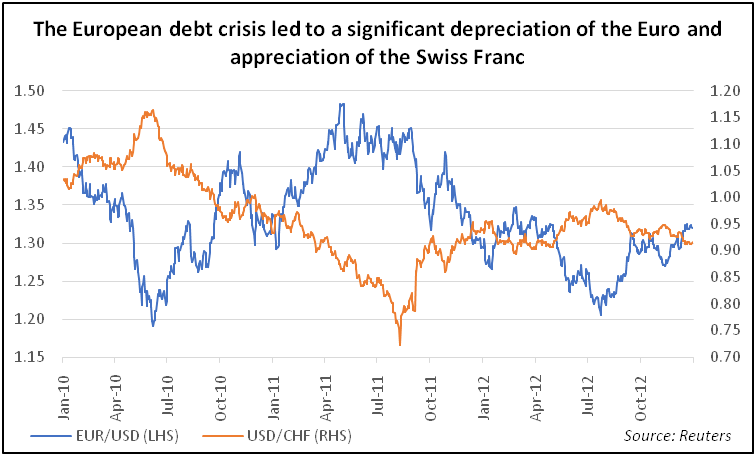

Notice in the chart above the behaviour of risk-on currencies and risk-off currencies during times of global economic uncertainties - one during the time of the sovereign debt crisis in Europe in 2010 and the other during a time when China unexpectedly devalued its currency in 2015. Movements in Japanese Yen, Swiss Franc, and the commodity majors (Australian Dollar, New Zealand Dollar, and Canadian Dollar) can often provide vital clues on the risk sentiment prevailing in the world. The former two currencies (JPY and CHF) tend to outperform during times of weak risk sentiment, while the latter three currencies (AUD, NZD, and CAD) tend to outperform during times of strong risk sentiment.

Interplay between currencies and bonds yields/spreads

Currency and government bond yields are closely connected. As we have studied in an earlier chapter, movement in one currency against the other is heavily influenced by the direction of interest rates prevalent among the two economies. This is because one of the major factors that influence the direction of global capital flows is interest rates across countries. A bulk of international investments goes into fixed income securities followed by investments into equities. As we already know, one of the major factors that influence inflows into fixed income securities is the coupon rate that they offer, which is directly influenced by the level of interest rates in the economy. Higher the interest rates, higher would be coupon rates. And higher the coupon rates, higher would be the allure for fixed income securities from international investors. Hence, as interest rates move up, so do bond yields. And as bond yields move up, so does the currency of that country. Hence, rising bond yields usually cause the currency of that country to appreciate. Similarly, lower the interest rates, lower would be coupon rates. And lower the coupon rates, lower would be the allure for fixed income securities from international investors. Hence, as interest rates move south, so do bond yields. And as bond yields move south, so does the currency of that country. Hence, falling bond yields usually cause the currency of that country to depreciate.

An important thing to keep in mind is that markets are always forward looking. They tend to react more to expectations rather than waiting for the event to occur. For instance, if interest rates are expected to go up, bond yields would price in these rate hikes by the central banks well ahead of time. Hence, it is quite common for yields to rise ahead of an increase in interest rates itself. Once the interest rate is hiked, markets start anticipating what the next move by the central bank could be. If the next move is anticipated to be another rate hike, yields would reflect them and continue moving higher. However, if the next move is anticipated to be a pause to rate hike, the upward movement in yields could slowdown. Similarly, if interest rates are expected to go down, bond yields would price in these rate cuts, causing yields to decline ahead of a decrease in interest rates itself. Once the interest rate is cut, markets would start anticipating what the next move by the central bank could be. If the next move is anticipated to be another rate cut, yields would reflect them and continue moving lower. However, if the next move is anticipated to be a pause to rate cuts, the downward movement in yields could abate. Currencies would also be impacted by such anticipated moves in yields. Hence, when using yields to analyse currency trends, it is very important to understand what the markets are anticipating about the future interest rate trajectory.

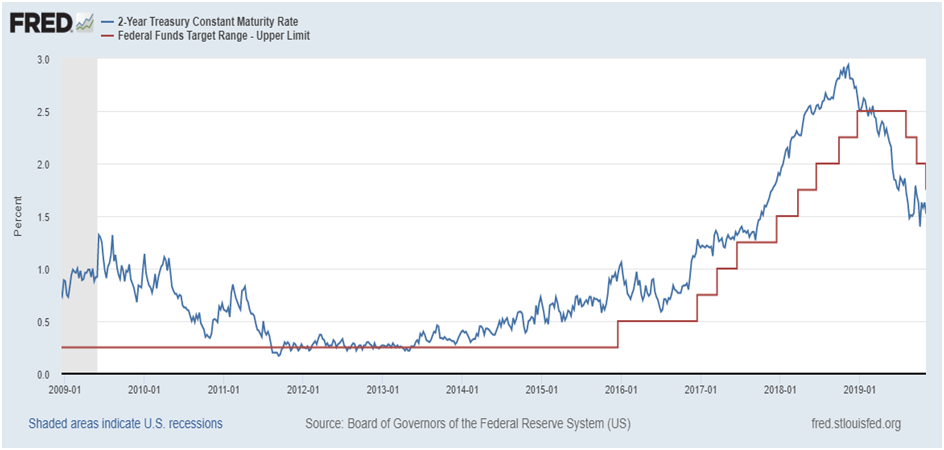

The above chart compares the 2-year treasury yield (blue line) with the Federal Funds rate (red line), which is the benchmark interest rate in the US set by the Federal Reserve. Observe in the chart that the first rate hike after the 2008 financial crisis came in December 2015. However, markets started pricing in the likelihood of a potential rate hike from as early as January 2014. By the time the first hike occurred, the 2-year yield had already rallied to nearly 1% from around 0.4% in January 2014. Anticipation of further rate hikes continued lifting the 2-year yield higher until the end of 2018. Towards the end of that year however, markets started pricing in the likelihood that the rate hike cycle could end and the Federal Reserve might actually reverse the hike cycle and start embarking on a series of rate cuts. As such, the yield started heading south. Notice that the first rate cut in this cycle came in August 2019, almost 8-9 months after the yield topped out and started declining. This chart is a classic example of how markets price in events well ahead of time.

The chart above now compares the 2-year US yield (blue line) and the trade-weighted Dollar Index (red line). Notice how the dollar started strengthening at essentially the same time that the yield started moving higher. Expectations that the US central bank would be the first among the G7 central banks to tighten its monetary policy caused yields in the US to shoot higher, making US investments more attractive to foreign investors. This in turn led to an increase in foreign inflows into the US, increasing demand for the Dollar and thereby causing it to appreciate against the G7 basket of currencies. Since late 2018 however, there has a slight decoupling between US yields and the Dollar. While US yields have headed lower, the Dollar has not weakened much against its G7 counterparts. One of the reasons for this is weakness among G7 currencies, as most of the central banks in Europe, Japan, and Asia-Pacific have themselves been cutting rates at a faster pace than the rate cuts by the Federal Reserve. This in turn has prevented the Dollar from weakening, and hence the decoupling between US yields and the Dollar. This latter portion of the chart highlights why it is crucial to keep a track of economic developments that are taking place not just in one country (such as the US) but across other important countries as well (especially the ones that belong to the G20 group). The Dollar is not just impacted by developments in the US but is also influenced by the developments taking place in other parts of the world, especially among the major trading partners of the US.

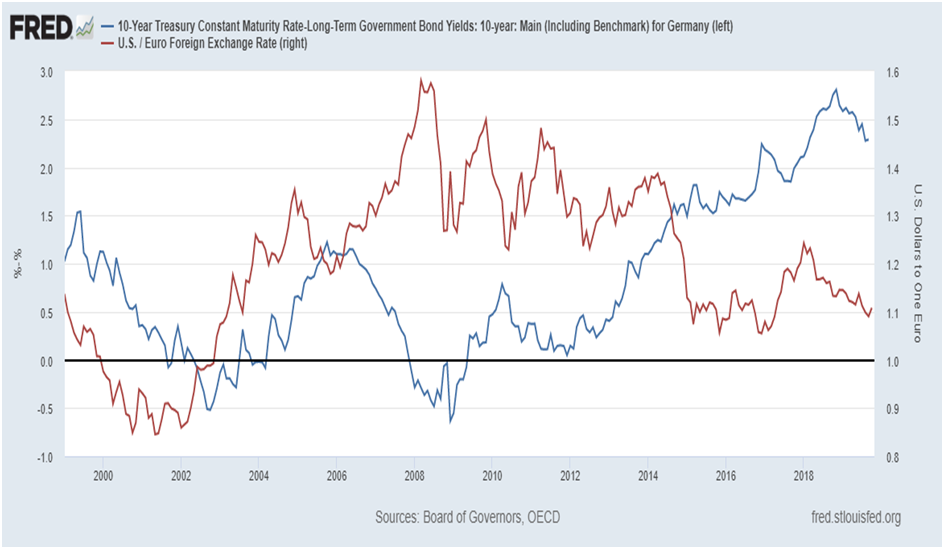

The chart above compares the spread between the US 10-year and German 10-year yield (blue line) with the EUR/USD exchange rate (red line). The spread is calculated as the US 10-year yield minus the German 10-year yield. Rising spread usually indicates that the markets are possibly anticipating the US monetary policy to be either more hawkish or less dovish than the Euro area monetary policy. This is positive for the dollar and negative for the euro. Similarly, falling spread usually indicates that the markets are possibly anticipating the US monetary policy to be either less hawkish or more dovish than the Euro area monetary policy. This is negative for the dollar and positive for the euro. Simply put, rising spread is negative for EUR/USD; while falling spread is positive for EUR/USD. Notice from the chart that since 2009, the spread between US 10-year and German 10-year yield has been widening as the Fed policy has generally been more hawkish than the ECB policy. As a result of the widening spread, the EUR/USD has steadily headed lower over the course of the past one decade. As long as markets expect the Fed to be more hawkish (or very recently, less dovish) than the ECB, the Euro could continue under pressure against the Dollar as capital shifts from euro area to the US in search of relatively higher yields.

.png)

The chart above compares the spread between the US 10-year and Japan 10-year yield (blue line) with the USD/JPY exchange rate (red line). The spread is calculated as the US 10-year yield minus the Japan 10-year yield. Rising spread usually indicates that the markets are possibly anticipating the US monetary policy to be either more hawkish or less dovish than the Japanese monetary policy. This is positive for the dollar and negative for the Japanese Yen. Similarly, falling spread usually indicates that the markets expect the US monetary policy to be either less hawkish or more dovish than the Japanese monetary policy. This is negative for the dollar and positive for the Yen. Simply put, rising spread is positive for USD/JPY; while falling spread is negative for USD/JPY. Notice from the chart how closely the two have moved with each other. From 2000 to 2012, the declining spread dragged down USD/JPY; while from 2012 to present, rising spread has lifted USD/JPY. Observe that since the end of last year, anticipation that the Fed will reverse its monetary policy from hawkish to dovish has caused the spread to shrink. This in turn has capped the gains in USD/JPY, despite the risk-on environment seen over the said period (which should ideally have benefited USD/JPY. Remember, Japanese Yen tends to weaken in a risk-on environment).

Interplay between currencies and commodities

Commodities do not equally impact all the currencies. In fact, some currencies influence commodity prices. This is especially true in case of the US Dollar. Generally speaking, a strong dollar makes it more expensive for holders of international currency to buy commodities, in turn hurting demand for commodities. As such, periods when the dollar is strengthening usually cause commodity prices to head south. Similarly, a weak dollar makes it cheaper for holders of international currency to buy commodities, in turn bolstering demand for commodities. As such, periods when the dollar is weakening usually cause commodity prices to head higher.

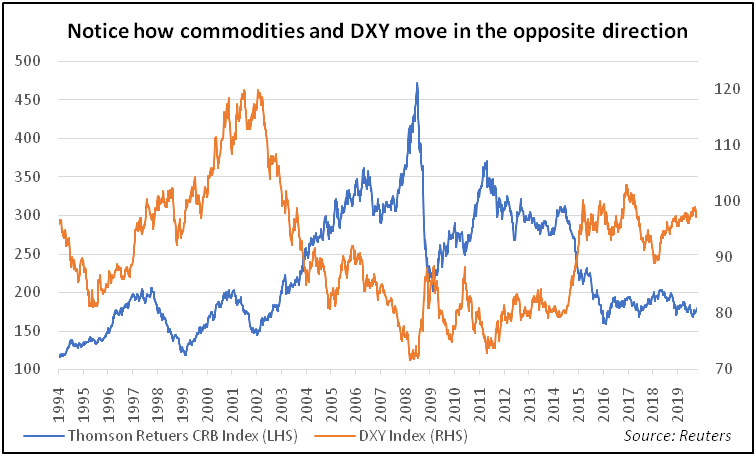

Notice in the above chart how commodities, as represented by the Thomson Reuters CRB Index (blue line), tend to move in the opposite direction of the dollar, as represented by the Dollar Index (orange line). The major downtrend in DXY index between 2002 and 2008 coincided with a major uptrend in the CRB index. Since then, the DXY index has recovered from its losses, causing the CRB index to pare a significant portion of its gains. As already stated, a strong dollar is negative for commodities, as it makes them more expensive to buy for holders of foreign currency. Similarly, a weak dollar is positive for commodities, as it makes them cheaper to buy for holders of foreign currency. Keep in mind that most of the major commodities that are traded around the world are priced in dollars. As a result, the direction of the dollar has a strong bearing on commodity prices.

Having said that, while the dollar has a strong influence on commodities, there are several currencies that are impacted by the trends in commodity prices as well. This is especially true in case of countries that are major exporters or importers of commodities. Put it in other way, there are nations whose exports are largely comprised of commodities as well as nations whose imports are heavily composed of commodities. The currencies of such countries are very sensitive to trends in commodity prices.

The currencies of countries whose major source of export revenue is earned via the export of commodities tend to appreciate during times of rising commodity prices. This is because rising commodity pricesboost export revenues, in turn strengthening the trade balance and government revenues. This leads to a higher GDP, all of which eventually causes the currency of such countries to strengthen. On the other hand, during times when commodity prices are falling, the currencies of such countries tend to depreciate as export revenues and GDP are negatively impacted.

Similarly, the currencies of countries that rely heavily on commodity imports and where commodity imports form a major portion of the trade bill tend to appreciate during times of falling commodity prices. This is because falling commodity prices reduce the import bill, in turn improving the trade balance. This in turn causes the currency of such countries to strengthen. On the other hand, during times when commodity prices are rising, the currencies of such countries tend to depreciate as import bill rises, increasing the outflow of the home currency.

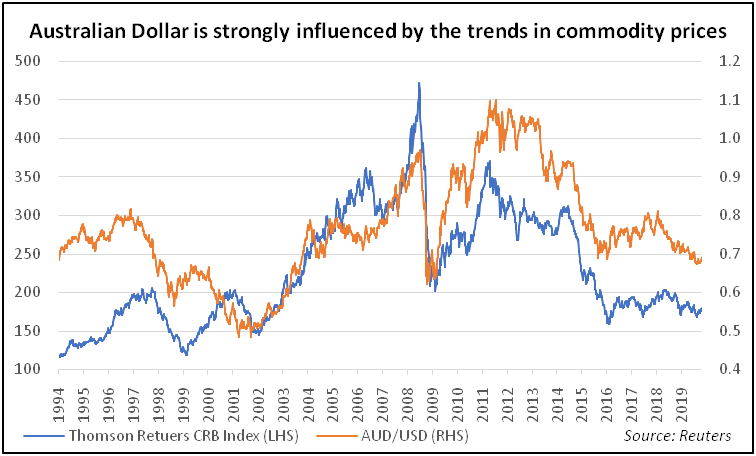

Notice in the chart above how closely the Australian Dollar tracks commodity prices, in general. The Aussie tends to move in the same direction in which the commodity prices are moving. The reason for the existence of this correlation is because Australia is a major producer and exporter of several commodities that range from metals to agricultural produce.

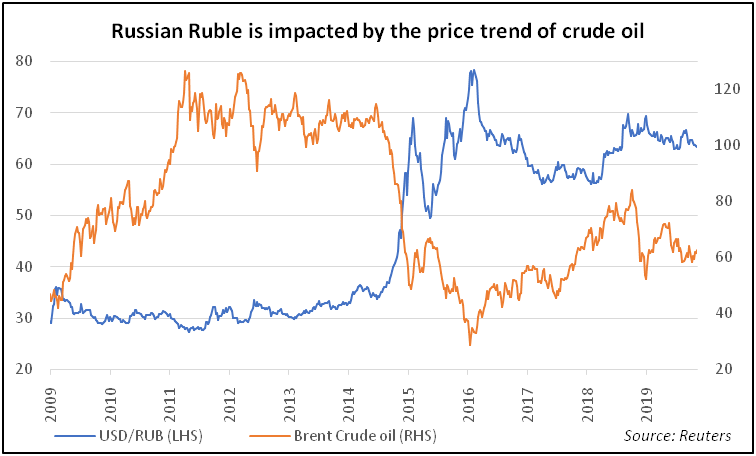

Meanwhile, notice in the chart below how closely the Russian Ruble is linked to the price of crude oil. Just like Australia, Russia is a major producer of several commodities. This is especially true in case of crude oil, with Russia being the second largest producer as well as exporter of crude oil in the world. As a result, the nation’s currency is closely tied to the price of oil. Notice in the chart how the steep sell-off in crude oil from 2014 to 2016 caused the Ruble to plummet to a record low against the Dollar. Since then, the recovery in oil prices has stabilized the Ruble and prevented it from sliding further.

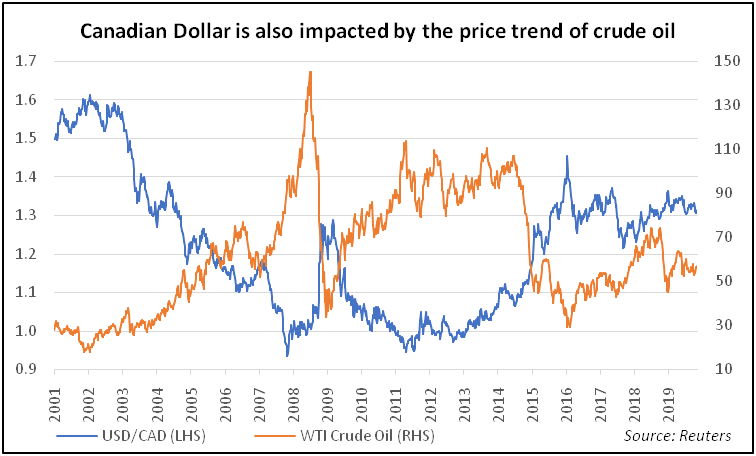

Just like Russia, Canada is also a major producer and exporter of crude oil. In fact, a significant portion of Canada’s export revenue comes by way of crude oil exports to other countries, most notably to the US. Hence, oil prices benefit the Canadian Dollar, while falling oil prices pressurizes the Canadian Dollar. It may be noted from the above chart how the Canadian Dollar strengthened from 2001 to 2008, due to the unprecedented surge in oil prices. However, as oil prices peaked out and remained under stress from the 2008 peak to 2016, the Canadian Dollar weakened notably. Since then, the modest recovery in oil prices has stabilized the Canadian Dollar.

Interplay between currencies and equities

While most currencies are heavily influenced by bond yields and some areevenheavily impacted by commodity prices, the impact of equities on currencies is complicated to establish. The reason why this is so is because, over time, the relationship between the two hasn’t been quite steady. Sometimes, the two move in the same direction, sometimes the two move in the opposite direction, and sometimes the two do not show any relationship at all. Hence, it is quite difficult to establish a generic impact that equity markets have on currency markets. As such, it is important that one is flexible in identifying the kind of impact equities are having on currencies at the present juncture.

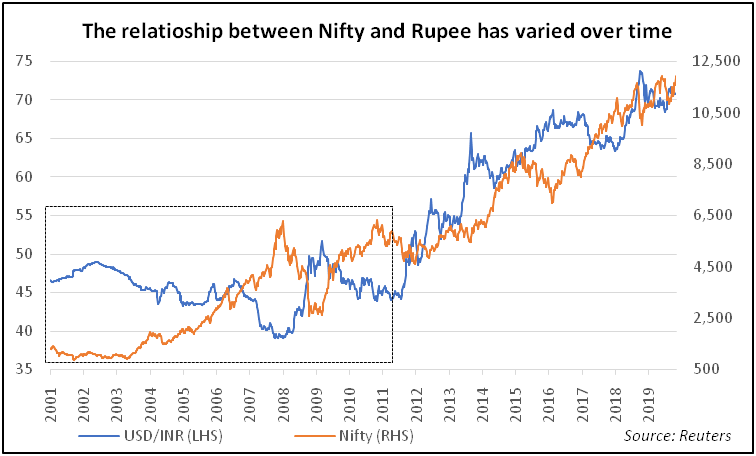

The above chart compares movements in Nifty with that in USD/INR exchange rate. Notice the dotted rectangular box. During the period 2001 to 2011, Nifty and USD/INR moved in the opposite direction. In other words, an up move in Nifty led to a strengthening Rupee (i.e. a weakening USD/INR), while a down move in Nifty led to a weakening Rupee. This correlation is understandable given that strengthening equity markets tend to increase the inflows of foreign money into the country whose markets are strengthening. This in turn increases the demand for the currency of that country, causing it to strengthen in value. The opposite is also true when equity markets weaken. That said, post 2011, the correlation between Nifty and USD/INR has changed. Since 2011, both the Nifty and USD/INR have been in an uptrend (meaning the Rupee has weakened over time despite the general up move in Nifty). One possible reason for this change in correlation has been that post the 2008 financial crisis, Asian and Emerging market currencies have depreciated notably against the Dollar. This in turn has more than offset the strength in Indian equity markets and caused the Rupee to gradually weaken.

Things to keep in mind

-

Currencies can be split into two categories: risk-on and risk-off currencies. Risk-on currencies are those that appreciate during times of positive risk sentiment and depreciate during times of negative risk sentiment. Examples include the commodity and the Emerging-market currencies. Risk-off currencies are those that appreciate during times of negative risk sentiment and depreciate during times of positive risk sentiment. Two of the most prominent examples include the Japanese Yen and the Swiss Franc.

-

Currency and bond yields tend to move in the same direction most of the times. Rising bond yields make fixed income securities more attractive to international investors, causing the currency of that country to strengthen. Similarly, falling bond yields make fixed income securities less attractive to international investors, causing the currency of that country to weaken.

-

The Dollar has a strong influence on the price of commodities. Rising dollar is negative for commodities, while falling dollar is positive for commodities. However, there are several currencies that are impacted by swings in commodity prices. This is especially true in case of countries that are major exporters or importers of commodities. Rising commodity prices benefit commodity exporting nations at the expense of commodity importing nations, while falling commodity prices benefit commodity importing nations at the expense of commodity exporting nations.

-

The relationship between currencies and equities is rather complex to interpret, given that this not remained constant over the years. Sometimes, the two move in the same direction, sometimes the two move in the opposite direction, and sometimes the two do not show any relationship at all. Hence, it is quite difficult to establish a generic impact that equity markets have on currency movements. As such, it is important that one is flexible in identifying the kind of impact equities are having on currencies at the present juncture.

Next Chapter

Comments & Discussions in

FYERS Community