So far, we have talked about the global Forex markets. We have covered aspects such as the evolution of the Forex market, key factors that drive the Forex markets, and some of the key currency pairs of the world -i.e. the ones that belong to the Majors, the Crosses, and the BRICS region. Now, it is time to focus on the Indian Forex market. In this chapter, we will briefly talk about the four currency pairs that are traded in India, with special emphasis on USD/INR,given that it is the most tracked and traded currency pair of India while also heavily influencing the movements among the other three pairs, namely EUR/INR, GBP/INR, AND JPY/INR.The major agenda of the chapter is, however, to speak how the two-way exchange rates are calculated and how the futures price for a currency pair is derived from the spot price.

Keep in mind that the objective of this chapter is to just introduce the currencies that are traded in India and to lay foundations for the currency derivatives and other chapters that will be covered later.

Introduction to Rupee and its crosses

In the last chapter, we briefly spoke about USD/INR. We talked about the key factors that impact the direction of the pair, including interest rate differential between India and the US, the direction of the monetary policies of the RBI and the Federal Reserve, risk appetite prevailing in the global market, economic health of India and the US etc.

The chart shows movement in the USD/INR pair since 2000. It can be seen from the chart that the pair bottomed out towards the end of 2007 and has since steadily appreciated for more than a decade.Put it in other words, the Rupee over the past 10 years has depreciated markedly against the Dollar. Back towards the end of 2007, it took a little under 40 INR to buy 1 USD. Today however, it takes more than 70 INR to buy 1 USD. Various factors are responsible for the Rupee’s underperformance against its US counterpart. The key amongst these are the steady appreciation of the Dollar against not only the G7 currencies but also the emerging market currencies and widening import bill and trade deficit of India because of surging oil and other imports.

The weakness of the Rupee against the Dollar has caused the former to underperform against the Euro and the Sterling too, despite the remarkable weakness seen in each of these currencies against the Dollar. For instance, since 2007, the Euro and the Sterling have weakened 30% and 40%, respectively, against the Dollar. Despite this, the Euro and the Sterling have strengthened 24% and 7%, respectively, against the Rupee. This has been largely down to the fact that the Rupee has depreciated nearly 80% against the Dollar during this period. Remember that in one of the previous chapters, we saw how cross currency values are calculated. EUR/INR is calculated as the product of EUR/USD and USD/INR, while GBP/INR is calculated as the product of GBP/USD and USD/INR. As the fall in each of EUR/USD and GBP/USD has been more than offset by the surge in USD/INR, EUR/INR and GBP/INR have appreciated over the past decade.Meanwhile, the value of JPY/USDhas moved higher from its value a decade ago. This coupled with the fact that the Rupee has depreciated around 80% against the Dollar over the past decade has caused JPY/INR to massively outperform during this period.

The table below will make these concepts easy to understand:

|

Currency Pair

|

Value in 2008

|

Value today

|

% Change

|

| EUR/USD | 1.58 | 1.10 | 30% down |

| USD/INR | 40 | 70.8 | 77% up |

| EUR/INR | 62.8 | 77.9 | 24% up |

| Currency Pair | Value in 2007 | Value today | % Change |

| GBP/USD | 2.08 | 1.23 | 40% down |

| USD/INR | 39.4 | 70.8 | 80% up |

| GBP/INR | 81.5 | 87.2 | 7% up |

| Currency Pair | Value in 2007 | Value today | % Change |

| JPY/USD | 0.0086 | 0.0093 | 8% up |

| USD/INR | 39.4 | 70.8 | 80% up |

| JPY/INR | 0.34 | 0.66 | 94% up |

Things to keep in mind

There aretwo important lessonsto learn from this. One is that when analysing the trend of, say, EUR/INR, besides looking directly into the charts of EUR/INR, it would greatly help if one analyses the trend of EUR/USD as well as USD/INR. This would help in better understanding the possible direction of the move in EUR/INR. Same is the case in analysing the trend of GBP/INR and JPY/INR.

The second lesson to learn is that explosive moves in Rupee crosses occur when both the dollar pairs move in the same direction. For instance, look at the table of JPY/INR above. Both the dollar crosses, i.e. JPY/USD and USD/INR, moved in the same direction - up, over a ten year period. This led to an even bigger move in JPY/INR. Hence, always be on the lookout for such occurrences, as the returns often tend to be significant.

Another thing to keep in mind is that the Rupee crosses tend to be quite volatile compared to USD/INR. This is because the Rupee crosses are a combination of two currency pairs - USD/INR on one side and one of EUR/USD, GBP/USD, or USD/JPY on the other side. While the Indian currency market closes at 5:00 PM IST, global currency markets are open for most parts of the day. Movements among the Majors tend to be quite volatile during the US session. This often causes the Rupee crosses to open with gaps during the following session. For instance, if USD/INR closes at 70.8 today and if EUR/USD is trading at 1.10 at 5.00 PM IST, EUR/INR should be closing somewhere around 77.88 (70.8 * 1.10). If on the following day, USD/INR opens at 70.7 and if EUR/USD is trading at 1.12 at that time, EUR/INR should be opening somewhere around 79.18. Notice that despite USD/INR opening slightly lower than the previous close, EUR/INR opened with a huge gap up because of the significant overnight rally in EUR/USD. Also, movements in the Rupee crosses can get volatile during the afternoon session, i.e. the time when the European sessionopens and a lot of news and economic data come out from the region.One needs to be aware of all these when trading Rupee crosses. We will talk about these in a greater detail later.

Two-way cross currency calculation

Before we get into currency derivatives, let us first understand how cross rates are derived. Forex quotes are expressed as two-way quotes, with the left side representing the “bid” side and the right side representing the “ask” side. The bid price is the maximum price that buyers are willing to pay to buy the base currency against the quoted currency, while the ask price is the minimum price that sellers are willing to accept to sell the base currency against the quoted currency. The difference between the bid and ask price is called the “spread”.

A USD/INR two-way quote would look something like this: 71.1850/71.2150.

Here, 71.1850 represents the bid price, while 71.2150 represents the ask price.

Now, let us see how two-way cross-currency rates can be calculated using two dollar pairs.

Case 1: Calculating the value of EUR/INR

In order to calculate the value of EUR/INR, we need the values of two dollar pairs i.e. EUR/USD and USD/INR.

Let us assume the following:

EUR/USD = 1.0973/1.0975

USD/INR = 71.1850/71.2150

In case of EUR/INR, EUR is the base currency while INR is the quoted currency. As EUR is also the base currency in EUR/USD and INR is also the quoted currency in USD/INR, we can just multiply the bid side of EUR/USD with the bid side of USD/INR to get the bid side of EUR/INR. So, 1.0973 * 71.1850 = 78.1113. Similarly, we can just multiply the ask side of EUR/USD with the ask side of USD/INR to get the ask side of EUR/INR. So, 1.0975 * 71.2150 = 78.1585.

So, EUR/INR = 78.1113/78.1585

Case 2: Calculating the value of GBP/INR

In order to calculate the value of GBP/INR, we need the values of two dollar pairs i.e. GBP/USD and USD/INR.

Let us assume the following:

GBP/USD = 1.2203/1.2206

USD/INR = 71.1850/71.2150

In case of GBP/INR, GBP is the base currency while INR is the quoted currency. As GBP is also the base currency in GBP/USD and INR is also the quoted currency in USD/INR, we can just multiply the bid side of GBP/USD with the bid side of USD/INR to get the bid side of GBP/INR. So, 1.2203 * 71.1850 = 86.8671. Similarly, we can just multiply the ask side of GBP/USD with the ask side of USD/INR to get the ask side of GBP/INR. So, 1.2206 * 71.2150 = 86.9250.

So, GBP/INR = 86.8671/86.9250

Case 3: Calculating the value of JPY/INR

In order to calculate the value of JPY/INR, we need the values of two dollar pairs i.e. USD/JPY and USD/INR.

Let us assume the following:

USD/JPY = 107.55/107.58

USD/INR = 71.1850/71.2150

In case of JPY/INR, JPY is the base currency while INR is the quoted currency. As INR is also the quoted currency in USD/INR, no changes are needed here. However, in case of USD/JPY, JPY is the quoted currency. Hence, we first need to convert JPY into base currency in USD/JPY. To do that, just flip the fraction, so that it becomes JPY/USD. Now, to calculate the bid side of JPY/USD, we need to divide 1 by the ask side of USD/JPY, which is 107.58. So, the bid side of JPY/USD becomes 0.009295. Similarly, to calculate the ask side of JPY/USD, we need to divide 1 by the bid side of USD/JPY, which is 107.55. So, the ask side of JPY/USD becomes 0.009298.

So,

JPY/USD = 0.009295/0.009298

USD/INR = 71.1850/71.2150

Now that we have all the values, we can do the necessary calculations to find out the two-way quote for JPY/INR. We simply multiply the bid side of JPY/USD with the bid side of USD/INR to get the bid side of JPY/INR. So, 0.009295 * 71.1850 = 0.6617. Similarly, we multiply the ask side of JPY/USD with the ask side of USD/INR to get the ask side of JPY/INR. So, 0.009298 * 71.2150 = 0.6622.

So, JPY/INR = 0.6617/0.6622

Things to keep in mind

When calculating the Rupee crosses, we need two dollar currency pairs. Things are simple when USD is a base currency in one pair and a quoted currency in the other pair (such as in case 1 and case 2 above). In such cases, we just multiply the bid side of one pair with the bid side of the other pair to get the bid side of the Rupee cross as well as multiply the ask side of one pair with the ask side of the other pair to get the ask side of the Rupee cross. Things, however, get a little tricky when USD is on the same side of both the currency pairs i.e. either on the bid side of both the pairs or on the ask side of both the pairs (such as in case 3 above). In such cases, there is a need to flip one of the dollar pairs, aligning it with the cross currency whose value we are trying to establish. After this, we just proceed with multiplying the two bids and the two asks to get the bid-ask price of the cross.

As a small exercise, try to find out the two-way currency quote for the EUR/JPY cross and the EUR/GBP cross, assuming:

EUR/USD = 1.0980/1.0984

USD/JPY = 107.30/107.33

GBP/USD = 1.2210/1.2214

Interest Rate Parity

Before we proceed to the next chapter, wherein we will be discussing in detail about currency derivatives that are traded on Indian exchanges, let us first try to understand a crucial concept called “interest rate parity”. For this, we will take the example of USD/INR.

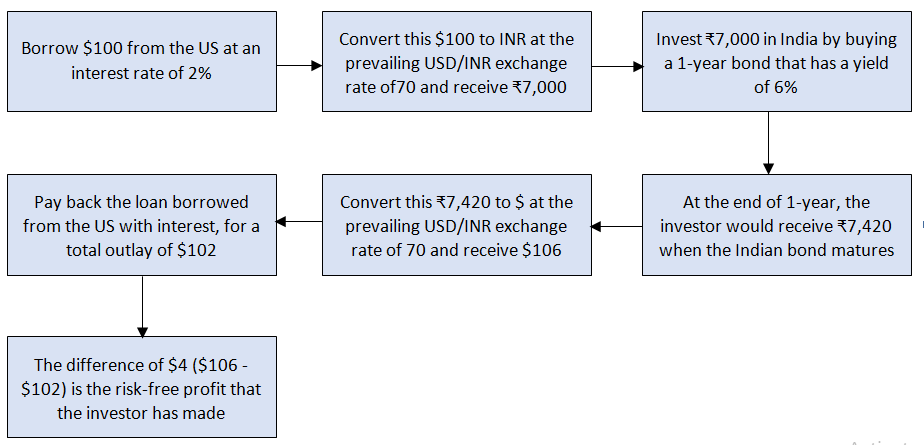

As we saw in an earlier chapter, international investors are always in search of higher, attractive yields. They tend to invest their capital in countries that have high interest rates. To fund such transactions, they tend to borrow money from countries that have low interest rates. If everything else remains constant till maturity, they would earn a risk-free profit on their investment, which would be the interest rate differential between the two countries. Let’s explain this concept using an example.

Let us take the case of India and the US. Let us assume that a 1-year loan in the US has an interest rate of 2%, while a 1-year bond in India has a yield of 6%. Let us also assume that an investor wants to invest $100 in India. To do this, he would borrow $100 from the US at a rate of 2%. At the end of one year, he would have to pay back the principle of $100 along with the interest of $2, for a total outlay of $102. Meanwhile, the $100 that he has received would be deployed to buy India’s 1-year bond. Before doing this, he would covert his $100 to INR. Let us assume that USD/INR is quoting 70 today in the spot market. So, by exchanging $100, he would receive ₹7,000. He would then use this ₹7,000 to buy 1-year Indian bond. At the end of one year when the bonds mature, he would receive the principle of ₹7,000 along with the interest of ₹420, for a total receipt of ₹7,420. Then, assuming the exchange rate remains constant at 70, he would exchange ₹7,420and get $106 (7420/70). Out of this $106, he would pay off his $102 debt for the loan taken from the US. The balance, which is $4, is his profit. This $4 is nothing but the interest rate differential between India and the US for a period of 1 year. The representation flow below would make this concept easy to understand.

Such a risk-free profit is nothing but an arbitrage opportunity. In reality however, the market very quickly corrects such opportunities, as and when they do appear. Hence, to prevent such arbitrage opportunities from arising, the difference between the proceeds received from investing in a high-yielding country (in the case above, India)and the proceeds paid for the loan taken from a low-yielding country (in the case above, the US) must equal the difference between the spot exchange rate and the forward exchange rate. This concept is called interest rate parity.

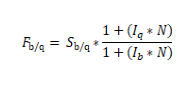

Notice that in the example above we assumed exchange rates would remain constant over a one year period. This, however, seldom happens. To prevent arbitrage opportunities, the forward exchange rate will either behigher than the spot exchange rate (when interest rate of the quoted currency is higher than interest rate of the base currency) or lower than the spot exchange rate (when interest rate of the quoted currency is lower than interest rate of the base currency). The below formula of calculating forward exchange rate would help to understand this concept better.

Such a risk-free profit is nothing but an arbitrage opportunity. In reality however, the market very quickly corrects such opportunities, as and when they do appear. Hence, to prevent such arbitrage opportunities from arising, the difference between the proceeds received from investing in a high-yielding country (in the case above, India)and the proceeds paid for the loan taken from a low-yielding country (in the case above, the US) must equal the difference between the spot exchange rate and the forward exchange rate. This concept is called interest rate parity.

Notice that in the example above we assumed exchange rates would remain constant over a one year period. This, however, seldom happens. To prevent arbitrage opportunities, the forward exchange rate will either behigher than the spot exchange rate (when interest rate of the quoted currency is higher than interest rate of the base currency) or lower than the spot exchange rate (when interest rate of the quoted currency is lower than interest rate of the base currency). The below formula of calculating forward exchange rate would help to understand this concept better.

Where,

F = the forward exchange rate

S = the spot exchange rate

Iq = interest rate of the quoted currency, per annum

Ib = interest rate of the base currency, per annum

N = number of years

Note that in the formula above, if Iq is less than Ib, the numerator would be smaller than the denominator and hence, the forward rate would be lower than the spot rate. Meanwhile, if Iq is greater than Ib, the numerator would be greater than the denominator and hence, the forward rate would be higher than the spot rate. Hence, it can be stated that if the base currency has a higher interest rate than the quoted currency, the forward rate will be at a discount (called forward discount); while, if the base currency has a lower interest rate than the quoted currency, the forward rate will be at a premium (called forward premium).

Using the above formula in the example above, we can see that,

Ib= 2%

Iq= 6%

S = 70

N = 1

Hence, F = 70 * [{1+(6%*1)}/{1+(2%*1)}] = 70 * [1.06/1.02] = 70 * 1.0392 = 72.7450

As such, the 1-year USD/INR forward rate is 72.7450.

There is an alternative way of calculating this. In the example above, we saw that after maturity, the investor would receive ₹7,420. Meanwhile, to clear his USD loan, he would have to pay $102. To prevent arbitrage opportunity, post maturity, this ₹7,420 must equal $102. For that to happen, the one-year forward at time t=0 must be ₹7,420 divided by $102, i.e. 72.7450, which is the same value that was derived from the formula above. This is what interest rate parity is all about. If interest rates between two countries are different, the currency pair of these two nations would move in such a way that it would lead to parity in interest rates, to eliminate risk-free gains.

Now, the next question one might ask is what does this all mean? Well, put it in simple words, what this means is, when the investor borrows money from a low-interest rate country and deploys it in a high-interest rate country, he would lock in the exchange rate at the then prevailing forward rate. When the investment that was made in high-yielding country matures and the investor receives the investment proceeds, he would convert the proceeds back at the forward exchange rate which he had locked in earlier. This ensures that no risk-free profit ismade from the investment.

For instance, in the example above, at the time of investing, the investor would lock-inat the USD/INR 1-year forward rate of 72.7450. Post maturity, when the investor receives ₹7,420, he would convert it back into USD at the locked-in rate of 72.7450. That is, he would receive $102, which he will then use to pay his USD loan. So, his $100 initial investment grew to $102, one year down the line, which is essentially the same amount had he invested $100 in the US directly for a period of one year.

Next Chapter

Comments & Discussions in

FYERS Community

Vinay commented on October 18th, 2019 at 4:09 PM

Very detailed. Thank you for sharing this useful information.

tejas commented on October 24th, 2019 at 5:56 PM

Thx Vinay. Make sure to read it completely.

Ranganath Murthi commented on October 18th, 2019 at 4:33 PM

As per the world market, EUR/USD is the highest traded contract, for the Indian market is it USD/INR or EUR/USD?

tejas commented on October 24th, 2019 at 5:56 PM

It's USDINR. EUR/USD contracts that were recently introduced by NSE are in the nascent stage and volumes cannot be compared to USDINR.

Saurab commented on October 18th, 2019 at 4:49 PM

What is the normal average volatility in Currency trading, Can you please give an example USD/INR?

tejas commented on October 24th, 2019 at 6:20 PM

Currencies are not as volatile as stocks or commodities. When the do move, they move in a one-sided trend. At least that's what I have observed.

Bhupathi commented on October 18th, 2019 at 5:06 PM

If Base Currency is improving than price of the pair will go down?

For example If USD become stronger what will be the impact on the INR?

Similarly for the Cross Currency pair how will the movement takes place?

tejas commented on October 24th, 2019 at 6:22 PM

Bhupati, If USD is going up, then INR will weaken obviously. It's the same with cross currencies. If one strengthens, the other weakens proportionately.

Kiran commented on October 18th, 2019 at 5:16 PM

What determines the forwards premium in Forex Market?

tejas commented on October 24th, 2019 at 6:23 PM

Interest rates until the expiration date or the cost of carry.

karthik commented on October 18th, 2019 at 5:30 PM

Thank you for the useful information. It's very useful to know about forex market.

tejas commented on October 24th, 2019 at 6:24 PM

Glad you like the content Karthik. So share it with your friends if you think they will benefit from it.

Vicky commented on October 18th, 2019 at 5:45 PM

I learn new information from your article, very useful content

tejas commented on October 24th, 2019 at 6:24 PM

Thx Vicky. :-)

Bikash commented on October 18th, 2019 at 9:31 PM

As we know, trading or investing in the currency market is a different kind of art.What factors one should consider before taking a position on Intraday as well as Swing trade?

tejas commented on October 24th, 2019 at 6:26 PM

I have written all about them in the currency module. I encourage you to read through all the chapters to get a proper understanding.

Swoorup Singh commented on October 18th, 2019 at 9:37 PM

Can I beat the inflation, if I will invest in USA market for 10 years, and send that maturity amount back to India?

tejas commented on October 24th, 2019 at 6:27 PM

It depends on:

- The inflation rate.

- Performance of the US market.

- Performance of the US dollar. If the dollar appreciates, it's a bonus.

Meenakshi commented on October 18th, 2019 at 9:59 PM

Nice article with forward exchange rate calculation.

tejas commented on October 24th, 2019 at 6:27 PM

Thanks, Meenakshi.

Priyanka commented on August 3rd, 2020 at 4:46 PM

Sir,

Can Indians trade in EUR/USD pair?

This is not listed in Fyers.

How can Indian trade above pair?

Abhishek Chinchalkar commented on August 5th, 2020 at 10:54 AM

Hi Priyanka, EURUSD, GBPUSD, and USDJPY are available for trading on Indian exchanges and they are listed on our platform as well. However, volumes and liquidity among these pairs tend to extremely low. Instead, one could gain exposure to these currencies indirectly by trading EURINR, GBPINR, and JPYINR, each of which tend to be quite liquid.

Mohan commented on August 12th, 2020 at 6:23 PM

hai, sir i need to know why you are allowing to trade spot currence market as they are open for the rest of the days.

Abhishek Chinchalkar commented on August 13th, 2020 at 12:03 PM

Hi Mohan, only currency futures and options are available for trading on exchanges and not spot.