Risk and Money Management are arguably the most important aspects of trading and investing. Every financial instrument has an inherent risk, and it is imperative that each investor is aware of the risks and is well prepared to minimize their impact when things turn out different from their expectation. Having a strong understanding of various aspects of risk and deploying a strategy to control risks is extremely critical in protecting one’s capital, and in achieving long-term success in trading and investing. The objective of this module is to equip all readers with various aspects and strategies of Risk and Money Management.

In this elementary chapter, we will familiarize the reader with an understanding of risk and variability of risk from one person to another, as well as from an asset class to another. Lastly, we will introduce the concept of Risk and Money Management, which forms the crux of this module.

What is Risk?

Risk is omnipresent and in every facet of life, irrespective of whether we realize it or not. A few commonly known risks which we encounter in our day to day lives are:

-

Stepping out of home and onto the streets (Risk: We may meet with an accident)

-

Doing financial transactions online (Risk: We may come under a phishing attack)

-

Eating junk food (Risk: It could gradually take a toll on health)

-

Exercising in a gym or playing a sport (Risk: We may get injured)

-

Watching TV for prolonged periods (Risk: It could gradually affect eyes)

-

Cooking food (Risk: It may not turn out to be as tasty as one would have hoped for)

-

Appearing for an exam (Risk: One might not fare well or even fail)

And so on... the list could continue, but you get the point. For any activity that we do in our day-to-day lives, there is always an element of risk involved. Now, let us try to understand risk. For this, look at the highlighted and italicized words in each of the above examples. You will notice that these words indicate probability and not certainty on the outcome of an event. Well, that is nothing but risk. Risk arises when there could be a deviation from an expected outcome. Put it in other words, Risk arises when there is an element of uncertainty regarding the outcome of a particular event. The concept of risk is applicable in trading and investing too. This is because when capital is deployed in financial markets, there is a possibility that one might suffer a loss of capital. In short, there is uncertainty about the outcome.

Generally, risk is often perceived with a negative connotation. However, not all risks are bad. In fact, certain risks must be taken to achieve happiness and/or success in life. For instance, to pass an exam, you need to take the risk of appearing for the exam; to see different countries, you need to take the risk of travelling around the world; to build a successful business, you need to understand the associated risks, and so on. Even in trading and investing, you need to assume risk if you intend to create wealth over time. If no risks are taken, then it is safe to say that there will be no rewards as well (On a lighter note, that reminds me of the phrase from the TV Series – Scam 1992: Risk hai toh Ishq hai). Having said that, risks must not be taken randomly and carelessly, but must rather be tackled logically and in a calculated manner. Before taking a risk, it is pivotal to ensure that the potential reward adequately compensates for the risk being taken. If not, it might not be worth taking the risk. We will talk briefly about this later in the chapter when discussing Risk and Return.

Trading and Investing are subject to Risk:

Trading and investing in the financial markets involve some element of risk. For instance, if I buy a stock at the current price of ₹100, I am exposed to the likelihood of the stock price dropping below ₹100 in the future (an unfavourable scenario), in which case I would be in a loss-making position. However, there is also a possibility of the stock price rising above ₹100 (a favourable scenario), in which case I would be in a profitable position. It is this element of uncertainty surrounding the outcome that gives rise to risk.

The level of Risk varies with each financial instrument:

The quantum of risk exposure depends on the financial instrument being chosen. Debt instruments tend to be relatively safe, equities and commodities tend to be relatively risky, while derivatives tend to be one of the riskiest choices. Furthermore, within financial instruments too, the level of risk varies. For instance, debt instruments issued by the government tend to be safer than those issued by corporates; large cap stocks tend to be safer than midcap stocks, which in turn tend to be safer than small cap stocks, and so on.

Various factors influence the Risk-taking ability of a trader/investor:

What factors influence the risk-taking ability of a person? Well, a trader or an investor’s willingness to take risk depends on several factors, internal and external.

A few decisive internal factors include: age of the individual, financial goals, personality, tenure of trade/investment, capital deployed, and size of disposable income. Meanwhile, some of the key external factors include market and economic conditions, and behaviour of other investors. Based on these, the risk-taking ability of a person tends to vary. As an example, a 55 year old person is likely to be more risk averse than a 25 year old person; a person with an income of ₹50 lacs is likely to be more open to assuming greater risks on a trade than a person with an income of ₹5 lacs; a person is likely to be willing to take greater risks during times when markets are rising than during times when markets are falling or are volatile, and so on.

It is crucial to identify the risks involved in each financial instrument (Equity, Commodity, Fixed Income, Derivatives, Mutual Funds, Exchange-Traded Funds etc.) and to thoroughly assess your risk-taking ability depending on various internal and external factors. Doing so will allow you to gauge:

i). Whether a particular asset class is suited to your trading/investing style, goals, and risk profile

ii). How much of your savings can you reasonably deploy for the purpose of trading/investing, and

iii). Whether to split capital across asset classes? If yes, in what proportion

Over the next few chapters, we will elaborate in greater detail about various types of risks that exist in financial markets, the statistical measures of quantifying risks, and the ways to mitigate or minimize risks.

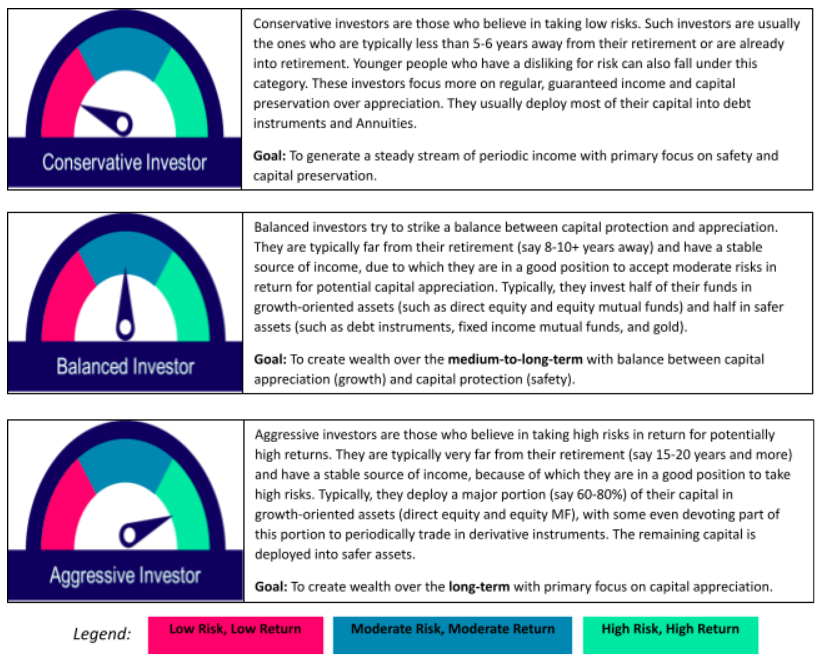

Categorizing Investors (and Traders) based on their Risk profile:

Broadly speaking, depending on the risk-taking ability, an investor can be bucketed into any one of the following three categories:

-

Conservative

-

Balanced

-

Aggressive

Within these three broad categories, there can be sub-categories too. For instance, within aggressive investor, there could be some who are very aggressive and some who are moderately aggressive. Similarly, within conservative investors, there could be some who are very conservative and some who are moderately conservative. Before you deploy capital with the objective of building wealth over time, it is essential to find out the applicable category. This will help in determining the optimum asset allocation based on each investor’s tolerance of risk and expectations of reward.

In a similar way, traders could also be classified as being aggressive or conservative. An aggressive trader is one who would be willing to take higher risks for potentially higher returns, while a conservative trader is one who would be more risk averse in nature, preferring capital protection first and foremost. As an example, a trader who is aggressive would prefer taking a higher exposure in derivatives, with the objective of earning higher profits per trade within a short-time span. On the other hand, a trader who is conservative might prefer taking more exposure in cash segment, with the foremost objective of limiting losses.

Dividing Assets based on their Risk and Reward potential:

As said earlier, not all asset classes traded on the financial markets possess the same level of risk. Some asset classes tend to be riskier, while some tend to be relatively safer. Moreover, within asset classes, the risk can vary between instruments. Broadly, there are several types of asset classes available for trading/investing, some of which offer a direct way to trade/invest (equities, commodities, debt, and derivatives) and some offer an indirect way (mutual funds and exchange-traded funds). The categorization below shows these key asset classes.

Meanwhile, the graph below shows the risk and reward potential among stocks, debt instruments, and derivatives. Kindly note that these are just general guidelines and not hard and fast rules. The actual risk and return can vary, depending on market conditions and the business cycle.

As can be seen in the chart above, certain instruments tend to be riskier than others. Depending on your risk profile, risk tolerance, financial capabilities, and investment goals, you need to decide the type and proportion of asset classes to deploy money. Although diversification will not help much in safeguarding against systematic risks, it will nonetheless ensure that you are insulated from security-specific or asset-specific risks.

Risk and Return go hand-in-hand:

Although the human mind is designed to focus more on rewards, risk is one aspect that should not be neglected at any cost. Trading or Investing is all about striking a balance between Risk and Return. In fact, there is always a trade-off between the two. As indicated in the graph earlier, the higher the risk an instrument poses, the higher the potential reward tends to be, and vice versa. For instance, parking funds in a fixed deposit can keep one’s capital safe, but the return potential will be quite low (at least when adjusted for inflation). On the other hand, deploying funds in equities increases the risks, but so would the potential for higher returns.

This concept of Risk and Return is applicable even when determining Entry and Exit levels. For instance, let us say that you are considering entering a trade at the prevailing market price of ₹100 and decide to place a stop loss for this trade at ₹90, which is 10% below the entry price. This trade will make sense only if you expect the price to rise by at least 10% from the entry level. Anything less and the trade is not worth considering as the risk would outweigh the potential reward. In fact, the higher the potential return relative to the risk being taken, the better would be the trade from a risk-reward standpoint. We shall talk in detail about this critical aspect of Risk and Return in a later chapter.

Why Risk and Money Management?

By now, we understand:

-

What risk is?

-

That trading and investing involves an element of risk

-

That the level of risk varies with each financial instrument

-

The three categories of investors (and traders) based on their tolerance for risk

-

Risk and reward go hand-in-hand

Let us now briefly talk about the crux of this module - Risk Management. Well, Risk Management is all about identifying, analysing, and managing individual and portfolio risks efficiently and effectively. Risk Management is arguably one of the most important, yet an often overlooked aspect of trading and investing. Why is risk management so critical?

Well, one thing to keep in mind is that, no matter how good your analysis and conviction are, your trade or investment can still go wrong. Losses are an inevitable part of trading/investing in the financial markets. What is important is how you manage your losses and ensure that they do not spiral out of control. Hence, before entering a position, you must have in place a proper exit strategy. That is, you must know at what point you will pull the trigger and exit the trade, in case the price of the security is moving against you. If no such plan is in place and you continue holding on to a losing position, it could seriously dent your capital and in some cases, erode it entirely. In fact, trading or investing without a proper risk management strategy is akin to gambling with your capital. On the other hand, by combining your knowledge of trading and investing with a proper risk management strategy, you will know how to control your losses. This in turn will enable you to stay in the markets for the long-term.

After all, keep in mind that Return of your Capital is more important than Return on your Capital. Once you deploy your capital in the financial markets, be it for the purpose of trading or investing, your foremost objective should be to protect the capital deployed. Everything else comes next. Over the course of this module, we will talk about several aspects of Risk Management. Before proceeding, let me mention a famous quote of Warren Buffett on Risk Management:

Meanwhile, Money Management is not the same as Risk Management, but the two are very intricately linked to one another and are often inseparable. As the name suggests, Money Management is all about efficiently managing your Money. Once you have a proper Risk Management strategy in place, Money Management strategies are then implemented to decide various aspects such as entry level, exit level (stop loss and target), position sizing, diversification and hedging etc. We will talk about these aspects in great detail over the course of this module.

Let us conclude this chapter by highlighting the key objectives of risk and money management:

-

To determine the optimal level of risk exposure one could possibly take

-

To safeguard against capital erosion and financial ruin

-

To maximize potential returns while keeping risks under control

-

To decide on position sizing

Always remember, understanding of risks is more important than expectation of rewards. Manage your risks, not returns.

Over the next couple of chapters, we will discuss the various types of risks that investors are exposed to.

Next Chapter

Comments & Discussions in

FYERS Community