Now that we have a good understanding about the basics of options, it is time to move on to an important part of the module: factors that impact the price of an option. In this chapter, we shall talk about the key factors that drive the option price.

By now, we are already aware of some of the key factors that impact the price of an option. In the previous chapter, we defined an option as a derivative contract that gives the holder of the instrument (i.e. the buyer) the right, but not an obligation, to buy or sell an underlying asset at a certain fixed price on or before a pre-determined date. From this definition itself, we can spot a few factors that impact the option price. These are:

-

Right to buy or sell (which is nothing but the type of option)

-

The Underlying asset (which includes the price of that asset as well)

-

Fixed price (which is nothing but the strike price)

-

Pre-determined date (which is nothing but the expiry date)

Besides these factors, option price is also strongly influenced by volatility, a measure that, unlike the above four elements, is not tangible but must rather be estimated. Finally, option price is also impacted by interest rates and in case the underlying is a stock, by dividends.

So, the factors that impact the price of an option are:

-

The type of option

-

The underlying price

-

The strike price

-

Time to expiration

-

Volatility

-

Interest rates

-

Dividend (in case the underlying is a stock)

Let us now understand in detail how each of these factors impact the price of an option:

1. Type of Option

Whether the option is a call option or a put option will have a noticeable impact on its price. For instance, in case of a call option, the option price will rise when the underlying price goes up and fall when the underlying price declines. On the other hand, in case of a put option, the option price will fall when the price of the underlying goes up and rise when the price of the underlying goes down. So, if a trader is long a call option or short a put option, he will benefit during times when the underlying price is rising, and vice versa. Similarly, if the trader is long a put option or short a call option, he will benefit when the underlying price is declining, and vice versa.

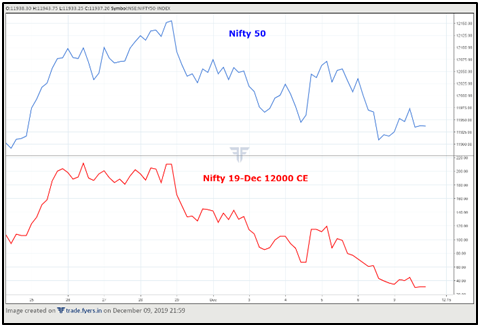

The chart above compares intraday movement in Nifty index with a corresponding movement in the Nifty 12000 Call Option (denoted as CE). Observe in the chart that as the price of Nifty (blue line) declined, so did the price of the Nifty 12000 CE (red line). Also notice the minor upticks in the option price whenever Nifty recovered from lows.

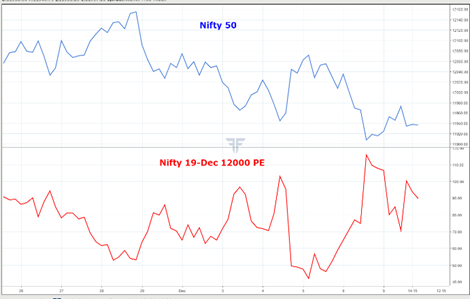

Meanwhile, the chart above compares intraday movements in Nifty index with a corresponding movement in the Nifty 12000 Put Option (denoted as PE). Notice that as the price of Nifty dropped (blue line), the price of the Nifty 12000 PE went higher (red line). Also observe that intermittent recoveries in Nifty were accompanied by a noticeable decline in option price.

From the above, we can see that the type of an option (whether a call or a put) strongly influences how the price of that option moves. For each of the factors that are mentioned below, the impact on the option price is affected by whether the option is a call or a put.

2. Underlying price

Option price is impacted by the price of the underlying asset. As we know by now, the price of the underlying asset is a variable price, as it keeps fluctuating over the life of the option contract. An increase in the price of the underlying benefits the holder of a call option (at the expense of the writer of that call option), in case the underlying price moves above the strike price of the option, and vice versa. Alternatively, a decrease in the price of the underlying benefits the holder of a put option (at the expense of the writer of that put option), in case the underlying price moves below the strike price of the option, and vice versa. In other words, the value of a call option will increase and that of a put option will decrease as the underlying price increases and moves above the strike price; while the value of a put option will increase and that of a call option will decrease as the underlying price decreases and moves below the strike price.

As an example, notice the two charts presented earlier. As the price of the underlying changes, so does the price of the option. The two charts show that as the underlying moves up, the value of a call option increases while that of a put option decreases. The opposite is also true as the underlying moves south. Hence, the underlying price has a very strong influence on the price of an option.

3. Strike price

While the underlying price is a variable price, the strike price on the other hand is a fixed price. It remains constant throughout the life of the option contract. By now, we are aware that we can measure moneyness of an option by looking at the difference between the strike price and the underlying price. We know that if the strike price is below the underlying price, the corresponding call option and put option are in-the-money and out-of-the-money, respectively. On the other hand, if the strike price is above the underlying price, the corresponding call option and put option are out-of-the-money and in-the-money, respectively. Hence, the position of the strike price relative to the underlying price has an impact on the price of an option, because it directly impacts the intrinsic value of an option, a key component of the option price. The lower the strike price is below the underlying price, the higher will be the price of a call option and the lower will be the price of a put option. Similarly, the higher the strike price is above the underlying price, the higher will be the price of a put option and the lower will be the price of a call option.

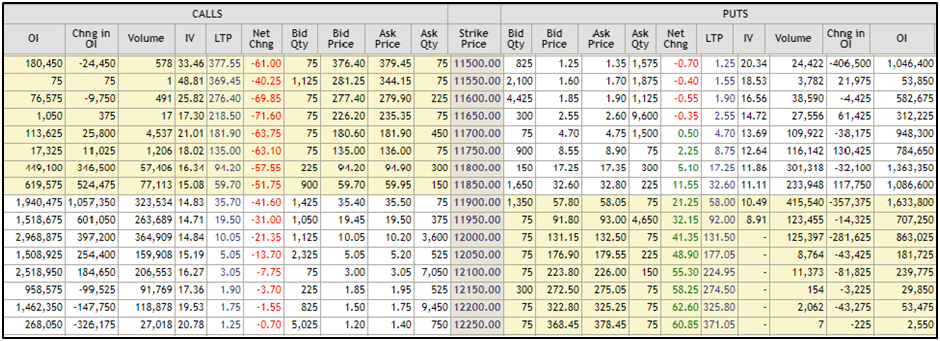

The above screenshot shows a part of the option chain data for Nifty options (Source: www.nseindia.com). At the time of writing, the prevailing price of Nifty is around 11860. If the table looks a little intimidating, don’t worry. We will talk in detail about how to read this table later. For now, just focus on two things: the strike price (which is at the exact centre of the table) and the LTP or the Last Traded Price (which is the fifth column from the left for call options and fifth column from the right for put options). It can be seen in the table that half of the rows are highlighted in yellow and the rest are in white. The ones that are in yellow indicate options that are in-the-money, while the ones that are in white indicate options that are out-of-the-money. Observe that in case of call options, the lower the strikes relative to the underlying price (11860), the higher is the option price (LTP), and vice versa. For instance, it can be seen from the table that a call option with a strike price of 11500 is much more expensive (₹377.55) that a call option with a strike price of 12250 (₹1.25). Similarly, in case of put options, the higher the strikes relative to the underlying price, the higher is the option price (LTP), and vice versa. For instance, it can be seen from the table that a put option with a strike price of 12250 is much more expensive (₹371.05) that a put option with a strike price of 11500 (₹1.25).

4. Time to Expiration

While the strike price has an impact on the intrinsic value of an option, the time to expiration has an impact on the time value of an option. The greater the time to expiration, the higher will be the probability of the option moving in favour of the buyer. Hence, the higher will be the time value of an option and subsequently, the higher will be the option price. Similarly, the lower the time to expiration, the lower will be the time value of an option and subsequently, the lower will be the option price.

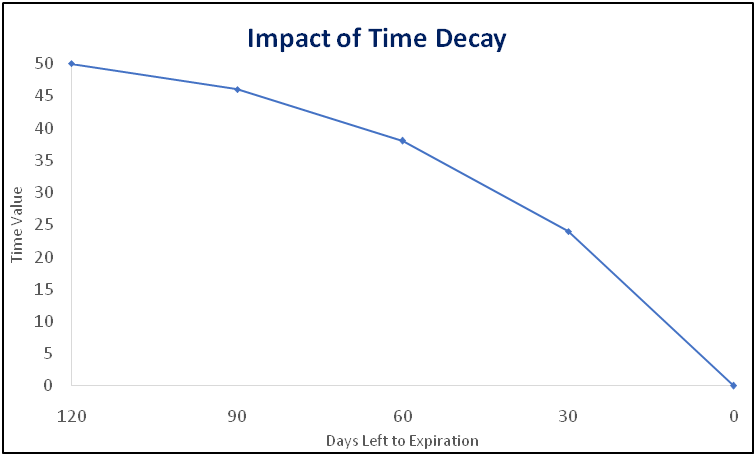

A crucial thing to remember is that as the time passes by, the time value component of the option price will decay at an exponential pace. During the initial life of an option contract, the pace of time decay will be slow. However, as the time to expiration reduces, the pace of time decay will start accelerating. During the latter stages of an option contract, the pace of time decay will be very fast. At the expiry, the time value of an option will fall to zero. To understand this better, look at the chart below.

Notice in the chart above the pace of decay in time value. Observe that initially the pace of time decay was slow; but as the time passed by, the pace of time decay started accelerating. Notice the pace of time decay from 30 days left to expiration till the expiration date. A key thing to remember is that the time decay works in favour of the option seller and against the option buyer. Understanding the concept of time decay is a very crucial part of learning Options. We will talk about this in a much greater detail in the chapter on Option Greeks. For now, keep in mind that option price is strongly influenced by the time value component.

5. Volatility

Put it in layman’s words, volatility is the rate at which the price of an asset fluctuates over time. It tells nothing about the direction in which the price of the asset is moving. Instead, volatility just tells the magnitude of fluctuation in the price of the asset. A very commonly used measure of volatility is standard deviation, which measures the amount of dispersion around the mean. Beta is another commonly used measure of volatility, especially in stock market parlance. The reason why volatility is such a vital concept in finance is because it helps to measure the “risk” involved in an investment. The greater the volatility, the greater is the risk involved in the investment, and vice versa. And the greater the risk involved in an investment, the greater is the return that an investor would expect to assume that excess risk.

As far as options are concerned, there are two types of volatility: historical and implied. Historical volatility is based on past fluctuations in the price of the underlying over a specific period, usually one year. On the other hand, implied volatility, as the name suggests, is used to measure future volatility. Unlike historical volatility (which is based on past data), implied volatility is based on what market participants imply the volatility of the underlying to be in the future. Given that implied volatility is forward-looking, it is very widely used in the pricing of options. Implied volatility is expressed as a percentage on an annualized basis. Observe the option chain screenshot that we had posted earlier in the chapter. The fourth column from the left shows the IVs or the Implied Volatility of call options, while the fourth column from the right shows the IVs of put options.

Implied volatility is reflected in the time value component of an option. In other words, the time value of an option is impacted not just by the time to expiration but also by the implied volatility. The higher the implied volatility, the higher would the time value component of an option price and subsequently, the higher would be the option price, and vice versa. Implied volatility is often used by market participants to determine whether a trade is worth taking. For instance, traders often compare the current implied volatility of an option with the average implied volatility of the past ‘n’ periods to see whether the option is cheap (undervalued) or expensive (overvalued). Given that volatility tends to revert to the mean, traders, especially the ones with greater risk appetite, often use higher-than-average IVs (indicative of overvalued options) to sell options, expecting to profit from volatility returning to normal levels. Similarly, they often use lower-than-average IVs (indicative of undervalued options) to buy options, expecting to profit from volatility returning to normal levels.

Volatility is a huge topic in itself. Given that it has a significant impact on the price of an option, it would be talked about in much greater detail in a later chapter. For now, keep in mind that the higher the volatility, the higher would be the price of an option, and vice versa.

6. Interest rates

Interest rate (risk-free) also affects the price of an option, although not as much as each of the variable talked above does. The reason why this is the case is because interest rates don’t tend to move as frequently and as much as other variables such as the underlying price, time to expiration, and volatility tend to move over the life of the option contract. That said, as interest rate has an impact on option price, it is worth talking and understanding how interest rates impact option prices.

A rise in interest rates benefits the value of a call option and hurts the value of a put option. The reason why this happens is because as interest rates go up, the opportunity cost of investing in certain financial instruments such as stocks also goes up. Why? Because a rise in interest rates makes interest-bearing investments, such as fixed deposits and T-Bills, more attractive. At the same time, it makes buying shares on borrowed money more expensive, because the cost of borrowing goes up. Hence, buying call options on stocks rather than buying stocks outright on borrowed money becomes more lucrative, given that the cash outlay on buying options is much lesser due to the greater leverage that options provide. Hence, the value of a call option tends to go up because of a potential increase in demand for them.

On the other hand, short selling a stock would lead to cash inflows into the trading account, which a trader can then use to invest in risk-free securities. This option can become more attractive during times when interest rates are high. Buying a put option on the stock, on the other hand, would lead to cash outflow from the trading account rather than inflow (because you need to pay the total cost of the option when buying one). As such, put options on stocks become relatively less attractive than short selling stocks. Hence, the value of a put option tends to go down because of a potential reduction in demand for them. Therefore, rising interest rates benefit call options and hurt put options. The opposite is also true when interest rates go down.

Of the factors impacting option price that we have studied so far, interest rates are arguably the least important factor in terms of how much they impact the option price. Other factors such as the underlying price, the strike price, the time left to expiration, and volatility are much more important inputs in valuing an option than interest rate is. We will talk more about interest rates in the chapter on Option Greeks. For now, remember that rising interest rate benefits call options and hurts put options, while falling interest rate benefits put options and hurts call options.

7.Dividend

The final factor that impacts the price of an option is dividend. This factor is only applicable to stock options and not to any other type of options. Furthermore, this factor applies to only those stocks that are expected to pay dividend during the life of an option contract. A thing to remember is that when options are priced, it is assumed that they would be exercised only on the expiration date. Also, at the time of pricing options, the dividend that a company would potentially give on the stock up to the expiration date of an option contract is taken into consideration.

But how exactly does dividend impact the price of an option? Well, on the ex-dividend date, assuming everything else is constant, the price of the stock reduces by as much as the amount of dividend that is payable by the company to its shareholders. Given that the price of the stock drops on the ex-dividend date to account for the dividend payable, the price of a call would gradually drop while that of a put would gradually rise to reflect for this drop in the value of the stock, leading up to the ex-dividend date. In other words, if a company is projected to give dividend during the life of the option contract, the price of a call option would be cheaper while that of a put option would be expensive, other things equal. The higher the dividend, the lower would be the price of a call option and the higher would be the price of a put option.

Just like the interest rate component of option pricing, the dividend component does not have much of an impact on the price of an option, unless the dividend amount or percentage is substantially large. This is because any potential dividend that would be paid on a stock during the life of an option contract is gradually reflected into the price of an option well ahead of the ex-dividend date. Of the factors influencing option price that we have studied in this chapter, dividend along with interest rate is relatively less important compared to other factors. In fact, the type of option, underlying price, strike price, volatility, and time to expiration have a much more important on the price of an option.

Let us now conclude this chapter by highlighting in a tabular format how each of the factors studied impact the price of an option.

|

Factors influencing Option Price |

Impact on the Price of a Call option |

Impact on the Price of a Put option |

|

Type of Option |

Depends on each of the other factor |

|

|

Underlying Price |

Direct |

Inverse |

|

Strike Price |

Inverse |

Direct |

|

Time to Expiration |

Direct |

Direct |

|

Volatility |

Direct |

Direct |

|

Interest Rates |

Direct |

Inverse |

|

Dividend |

Inverse |

Direct |

In the above table, direct impact means a specific factor has a direct impact on the price of an option; while inverse impact means a specific factor has an inverse impact on the price of an option. For instance, the underlying price impacts call option directly, meaning a rise in underlying price leads to a rise in the price of the call option as well. Meanwhile, the strike price impacts call option inversely, meaning the lower the strike price, the higher would be the value of a call option. In the coming chapters, we will take in detail about Option Greeks and Option Strategies. Before proceeding to these advanced topics however, a reader is advised to get a strong grip on each of the concepts that we have spoken thus far.

Next Chapter

Comments & Discussions in

FYERS Community

TAMOGHNA commented on June 11th, 2020 at 12:28 PM

Sir

When and why the both OTM/ITM option price increase at the same time. PLease let me know.

Regards

Tamoghna

Abhishek Chinchalkar commented on June 12th, 2020 at 9:09 AM

Hi Tamoghna, the price of an OTM/ATM/ITM Call tends to move in the same direction and so does the price of an OTM/ATM/ITM Put. For example, if the underlying price is rising, the price of an OTM/ATM/ITM Call belonging to the same underlying will also rise while that of an OTM/ATM/ITM Put will fall, and vice versa.

What however differs is the speed with which the price of an option is changing for every one point change in the underlying price. This is impacted by the option Greek, Delta. The larger the value of Delta in absolute terms, the larger will be the change in option price for every one point change in the underlying price.

We suggest you to read the chapters that are ahead in this Module, as doing so would help you in understanding these concepts much better.