Over the next two chapters, we shall discuss various strategies involving futures. For our discussion, we will keep our universe restricted to index and stock futures that are traded on the NSE. The objective of this chapter and the next is to enable the reader to understand various strategies that can be deployed using futures. In this chapter, we shall focus on long futures, short futures, and Calendar Spread.

Long Futures

This is the most common of all the available strategies in futures. A long futures is a trading strategy wherein the trader would initiate a long (buy) position in futures with the objective of profiting from a potential rise in the price of the instrument that underlies that futures contract. Remember what we said in one of our earlier chapters – futures is a derivative of an underlying instrument whose price tends to move in sync with the price of that underlying instrument. So, a trader establishing a long positionin futures would have a bullish outlook on the instrument that underlies that futures contract. For instance, if I am long Nifty futures, I have a bullish view on the Nifty 50 index (the underlying instrument); if I am long Infosys futures, it means I have a bullish view on Infosys (the underlying instrument), and so on.

Let us take an example now. Let us assume that Nifty futures is currently trading at 10400 and the trader expectsthe indexto rise in the coming days. Because of his bullish stance on Nifty, he could initiate a long position in Nifty current month futures at the prevailing level of 10400. Going forward, if Nifty rises above 10400, the trader would benefit; while if Nifty falls below 10400, the trader would suffer. Let us analyse both these situations as below:

Contract: Nifty July futures – current month expiry

Lot size: 75

Number of Lots: 3

Futures CMP: 10400

Position: Long at CMP

Scenario 1: After 10 days

Nifty futures CMP: 10850

As expected, Nifty has risen from the time the long position was established. The trader now see that the index is approaching a key resistance, which he believes could hold in the short-term. Based on this, he has decided to close out his long position and book profits. Remember, closing out a long position means shorting the same instrument in the same quantity and for the same expiry. So, in this case, the trader would sell (i.e. exit) 3 lots Nifty July futures at 10850. His profitability on the trade would be calculated as follows

Profit = (Exit Price – Entry price) * lot size * number of lots = (10850 – 10400) * 75 * 3 = ₹1,01,250

Here, the position is held for a period of 10 days. Recollect from the previous chapter that futures are subject to daily MTM. However, given that we understand how this mechanism works, we won’t be showing the same again in this chapter. Instead, we would directly be calculating the final profit/loss, which is nothing but the sum of all the daily MTM from the date of entry till the date of exit.

Scenario 2: After 4 days

Nifty futures CMP: 10180

Post initiation, Nifty started drifting lower. The index has broken a key support level of 10200. Based on this, the trader has decided to cut short his losses and exit the long position. His loss on the trade would be calculated as follows:

Loss = (Exit Price – Entry price) * lot size * number of lots = (10180 – 10400) * 75 * 3 = ₹49,500

A long position in futures can be established either for intraday purposes or for holding the position overnight/until expiry. As we saw in the previous chapter, futures are subject to margins. For carrying positions overnight or till expiry, the trader will need sufficient funds in his/her trading account to meet the requirements of Initial Margin and daily MTM Margin. On the other hand, margins for intraday position (i.e. entering and exiting on the same day) are usually lower, because they don’t tend to possess overnight risks. We will talk more about these in a later chapter.

If a trader holds on to the long position, as the expiration of the futures contract draws nearer, the trader must make a choice of whetherto take delivery of the underlying (assuming the futures contract is physically deliverable). If the trader does not intend to take delivery, then he/she must either close out the existing long position before expiration of the futures contract or roll it over to the next contract (A rollover of long position is a scenario wherein the trader would close all existing long position(s) in the futures contract that is approaching expiration and simultaneously create new long position(s) in the next futures contract). Whether or not the trader rolls over the long position(s)to the next contract depends on a few factors, one of them being his/her view on the underlying. If the trader continues expecting the underlying to rise, he/she may opt to rollover the contract to the next one. On the other hand, if the trader does not expect the underlying to rally, he/she may choose to close out the long position altogether prior to expiration.

As we have seen above as well as in previous chapters, a major advantage of a futures contract is that it can be exited anytime post the entry. There is no obligation, whatsoever, for the trader to carry his/her position till the expiration of the futures contract. In fact, the trader can exit the position even a few seconds after entering into the contract.

Short Futures

Above, we saw that when a trader has a bullish view on the underlying, he/she can buy the futures contract on that underlying and sell it (exit) later in case his/her view turns out to be right (or wrong!). But what if a trader has a bearish view on the underlying? Can a trader short the futures on that underlying and buy it back (exit) later? The good news is that the trader can short in futures, just as easily as he or she can long in futures. Unlike in the cash segment where short selling is permitted only for intraday (sell and back buy later but on the same day), there are no restrictions in shorting futures and carrying the position forward until expiry.

Along with long futures, short futures is a very popular strategy. A short futures is a trading strategy wherein the trader would initiate a short (sell) position in futures with the objective of profiting from a potential decline in the price of the instrument that underlies that futures contract. A trader establishing a short position in futures would have a bearish outlook on the instrument that underlies that futures contract. For instance, if I am short Nifty futures, I have a bearish view on the Nifty 50 index; if I am short ICICI Bank futures, it means I have a bearish view on ICICI Bank, and so on.

Let us take an example now. Let us assume that ICICI Bank futures is currently trading at 350 and the trader expects the stock to fall in the coming days. Because of his bearish stance on the underlying, he decides to initiate a short position in ICICI current month futures at the prevailing price of 350. Going forward, if the futures pricefallsbelow 350, the trader would benefit; while if the futures price rises above 350, the trader would suffer. Let us analyse both these situations as below:

Contract: ICICI Bank July futures – current month expiry

Lot size: 1375

Number of Lots: 5

Futures CMP: 350

Position: Short at CMP

Scenario 1: After 8 days

ICICI Bank futures CMP: 305

As expected, the stock has declined from the time the short position was established. The trader now sees that the stock is approaching a key support level, which he feels could hold in the short-term. Based on this, he has decided to close out his short position and book profits. Remember, closing out a short position means buying the same instrument in the same quantity and for the same expiry. So, in this case, the trader would buy (i.e. exit) 5 lots ICICI Bank July futures at 305. His profitability on the trade would be calculated as follows:

Profit = (Entry Price – Exit price) * lot size * number of lots = (350 – 305) * 1375 * 5 = ₹3,09,375

Scenario 2: After 3 days

ICICI Bank futures CMP: 375

Post initiation, ICICI Bank started inching higher. The stock has broken a key resistance level of 375. Based on this, the trader has decided to cut short his losses and exit the short position. His loss on the trade would be calculated as follows:

Loss = (Entry Price – Exit price) * lot size * number of lots = (350 – 375) * 1375 * 5 = ₹171,875

If a trader holds on to the short position, as the expiration of the futures contract draws nearer, he/she must make a choice of whether to give delivery of the underlying (assuming the futures contract is physically deliverable). If the trader does not intend to give delivery, then he/she must either close out the existing short position before expiration of the futures contract or roll it over to the next contract (A rollover of short position is a scenario wherein the trader would close all existing short position(s) in the futures contract that is approaching expiration and simultaneously create new short position(s) in the next futures contract). Whether or not the trader rolls over the short position(s) to the next contract depends on a few factors, one of them being his/her view on the underlying. If the trader continues expecting the underlying to decline, he/she may opt to rollover the contract to the next one. On the other hand, if the trader does not expect the underlying to decline, he/she may choose to close out the short position altogether prior to expiration.

Just like in case of a long futures position, a short futures position would also be subject to Initial Margin and MTM Margin requirements. Because the trader is short the futures, keep in mind that the payoff will be opposite as compared to a long futures position. That is, the trader’s account would be credited in case the settlement price for one session is below the settlement price of the previous session (if the position is carried overnight) or below the short entry level (for intraday positions or on the first day of shorting the futures contract), and vice versa.

Things to remember when going long or short in futures

-

A trader who is long futures has a bullish view on the underlying of the futures contract

-

A trader who is short futures has a bearish view on the underlying of the futures contract

-

At the time of opening a long or short position in futures, the trader will need to have sufficient funds in his/her account to meet the initial margin requirements

-

Even after creating a position, a trader would need sufficient funds in his/her account to meet the requirements of daily margining, if he/she intends to carry the position overnight

-

If a futures contract is physically deliverable and if a trader has an open long or short futures position for which he/she does not intend to take or give delivery, the trader must either close the position before expiry or roll it over to the next contract

-

Because futures are highly leveraged instruments, risk management is of utmost importance when creating long or short futures position

-

Before entering a position in futures, it is important to have a stop loss in place and adhere to that stop loss in case the view goes wrong

-

One could use either fundamental or technical analysis, or a combination of both, to create long or short position(s) in futures

Calendar Spread (aka Intra market Spread)

Now that we understand the two plain vanilla futures strategies i.e. long futures and short futures, it is time to dwell a little deeper. In this section, we will talk about Calendar spread, which is a popular spread strategy implemented by traders in the futures segment. But what exactly is a calendar spread?

Also known as Intramarket Spread, a Calendar Spread is a strategy in which a trader establishes a long futures position in one contract and simultaneously establishes a short futures position having the same underlying instrument but different expiration. An example includes buying Nifty futures near month contract and simultaneously selling Nifty futures next month contract, or vice versa.

A Calendar Spread is implemented by a trader when he/she is of the opinion that the price spread between two futures contracts having the same underlying but differing maturities has gotten out of sync. That is, either the spread is narrower than usual or wider than usual. This strategy can also be implemented if a trader has a view on the spread and expects it to widen or narrow over time. One of the biggest advantage of a Calendar Spread is that it eliminates price risk. In other words, by establishing a Calendar Spread, a trader becomes neutral on the direction of the underlying price. He/she wouldn’t care whether the price of the asset that underlies the two futures contracts goes up or down. If it goes up, then loss incurred in one of the two positions would be more or less offset by profits made in the other position, and vice versa. Instead, what would matter most to a trader when establishinga Calendar Spread strategy is the direction of the spread in terms of whether it would widen going forward or narrow. Another major advantage of establishing a Calendar Spread strategy is the cost of implementing this strategy. Compared to a naked Long Futures or Short Futures strategy, Calendar Spread is much less risky. For instance, let us take an example using the following statistics.

-

Nifty spot CMP: 10233

-

Nifty July futures CMP: 10169

-

Nifty August futures CMP: 10170

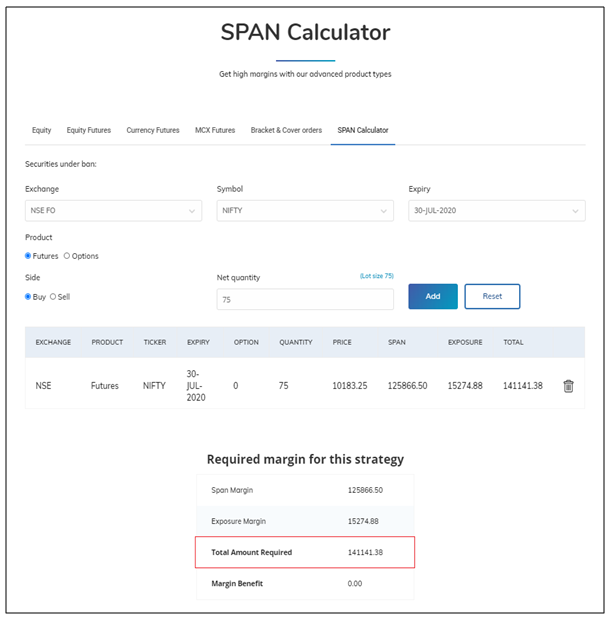

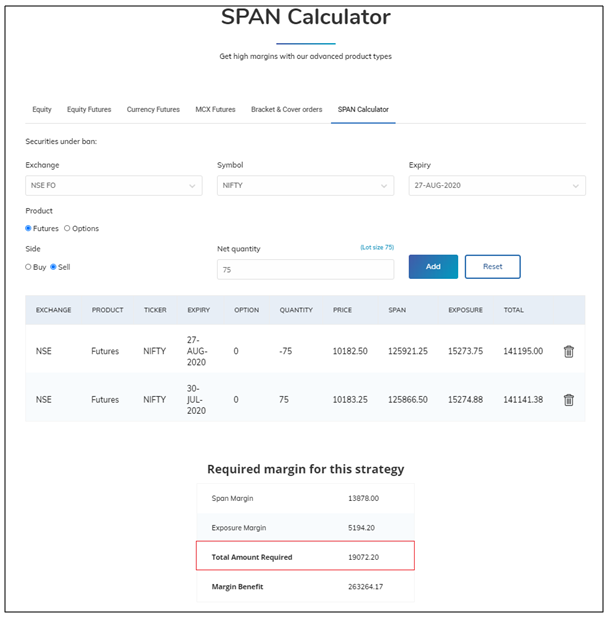

In a couple of days, let us assume that Nifty spot falls to 10000, which implies a fall of 233 points (10233-10000). Because the underlying price has declined by 233 points, the two futures contracts would also fall by more or less a similar margin. Let us say that Nifty July futures drops to 9935, while Nifty August futures drops to 9937. Now, if the trader had established a naked Long futures position, he/she would have suffered a loss of 233 points, which translates to a loss of ₹17,475 per lot (233 * 75). However, what if the trader had instead established a spread strategy wherein, he/she had simultaneously gone long July futures and short August futures? In this case, the trader would have suffered a loss of 234 points in the July position (10169-9935) and realized a gain of 233 points in the August position (10170-9937), for a net loss of just 1 point, which translates to a loss of just ₹75 per lot. Notice the difference? Because a spread involves creating two opposite positions (long and short) rather than just a naked position (long only or short only), they tend to be much safer and less volatile. As a result, the margin requirement in a Calendar Spread strategy also tends to be drastically smaller. Let us explore this now using our FYERS SPAN calculator.

Notice in the image above that the initial margin needed to buy 1 lot of Nifty July futures is ₹1,41,141. However, compare this to the image below, which shows the margin needed to trade a Calendar Spread. As the trader is buying 1 Nifty July futures and simultaneously selling 1 Nifty August futures, the total margin needed to execute this strategy is just ₹19,072!

Because Calendar Spreads require significantly less margin and because they are much less risky than a naked long or short futures position, it goes without saying that the absolute return on Calendar Spreads also tends to be quite small. Furthermore, while Calendar Spreads are much less risky, it must be kept in mind that they are completely without risks. For instance, if a trader establishes a Calendar Spread on the back of expectations that the spread between the two contracts will narrow and if it instead ends up widening, then the trader could suffer a loss.

Types of Calendar Spread

There are two types of Calendar Spreads, Long Calendar Spread (aka Bull Calendar Spread) and Short Calendar Spread (aka Bear Calendar Spread). A Long Calendar Spread is a strategy in which the trader would buy a near-month futures contract (near dated) and sell the next-month futures contract (farther dated). This strategy is initiated when a trader expects the near-month futures contract to outperform the next-month futures contract. Meanwhile, a Short Calendar Spread is a strategy in which the trader would sell a near-month futures contract and buy the next-month futures contract. This strategy is initiated when a trader expects the near-month futures contract to underperform the next-month futures contract.

While the price of the two futures contracts (near-month and next-month) belonging to the same underlying tends to move in the same direction most of the time, the speed at which the price moves is not the same. This in turn, occasionally, gives traders the opportunity to set up Calendar Spread strategies.

A Long Calendar Spread strategy can benefit from any one of the following scenarios:

-

The near-month futures contract rises, while the next-month futures contract remains unchanged

-

The near-month futures contract rises, while the next-month futures contract falls

-

The near-month futures contract rises, while the next-month futures contract also rises but at a slower rate

-

The near-month futures contract remains unchanged, while the next-month futures contract falls

-

The near-month futures contract falls, while the next-month futures contract also falls but at a faster rate

Similarly, a Short Calendar Spread strategy can benefit from any one of the following scenarios:

-

The near-month futures contract remains unchanged, while the next-month futures contract rises

-

The near-month futures contract falls, while the next-month futures contract rises

-

The near-month futures contract rises,whilethe next-month futures contract also rises but at a faster rate

-

The near-month futures contract falls, while the next-month futures contract remains unchanged

-

The near-month futures contract falls,while the next-month futures contract also falls but at a slower rate

Let us look at an example now. Let us assume the following things:

-

Nifty July futures CMP: 10237

-

Nifty August futures CMP: 10233

-

Nifty Spread CMP: -4 (10233-10237)

Let us say that the trader is of the opinion that this discount in spreadwill widen in the next few days. Based on this, he decides to initiate a long Calendar Spread wherein he will buy 1 Nifty July futures at 10237 and simultaneously sell 1 Nifty August futures at 10233. The Initial Margin needed for this strategy is ₹19,102.

Scenario 1: After 5 days

-

Nifty July futures CMP: 10530

-

Nifty August futures CMP: 10503

-

Nifty Spread: -27 (10503 - 10530)

As the trader is long in July futures, he would realize a profit of 293 points (10530 - 10237) on the long position. On the other hand, as the trader is short in August futures, he would suffer a loss of 270 points (10233 - 10503) on the short position. Net-net, the trader has realized a gain of 23 points (profit of 293 points –loss of 270 points) on the trade, which translates to a gain of ₹1,725 per lot (23 * 75). In this case, the return on the trade would be +9.03% (1725 / 19102 * 100).

Scenario 2: After 5 days

-

Nifty July futures CMP: 10000

-

Nifty August futures CMP: 9953

-

Nifty Spread: -47 (9953 - 10000)

As the trader is long in July futures, he would suffer a loss of 237 points (10000 - 10237) on the long position. On the other hand, as the trader is short in August futures, he would realize a gain of 280 points (10233 - 9953) on the short position. Net-net, the trader has realized a gain of 43 points (profit of 280points –loss of 237 points) on the trade, which translates to a gain of ₹3,225 per lot (43 * 75). In this case, the return on the trade would be +16.88% (3225 / 19102 * 100).

Scenario 3: After 5 days

-

Nifty July futures CMP: 10500

-

Nifty August futures CMP: 10523

-

Nifty Spread: 23 (10523 - 10500)

As the trader is long in July futures, he would realize a profit of 263 points (10500 - 10237) on the long position. On the other hand, as the trader is short in August futures, he would suffer a loss of 290 points (10233 - 10523) on the short position. Net-net, the trader has suffered a loss of 27 points (profit of 263 points –loss of 290 points) on the trade, which translates to a loss of ₹2,025 per lot (27 * 75). In this case, the return on the trade would be -10.60% (2025 / 19102 * 100).

Scenario 4: After 5 days

-

Nifty July futures CMP: 9950

-

Nifty August futures CMP: 9983

-

Nifty Spread: 33 (9983 - 9950)

As the trader is long in July futures, he would suffer a loss of 287 points (9950 - 10237) on the long position. On the other hand, as the trader is short in August futures, he would realize a gain of 250 points (10233 - 9983) on the short position. Net-net, the trader has suffered a loss of 37 points (profit of 250points –loss of 287 points) on the trade, which translates to a loss of ₹2,775 per lot (37 * 75). In this case, the return on the trade would be -14.53% (2775 / 19102 * 100).

As we can see from the above example of long Calendar Spread, the trader would profit if the near-month futures contract outperforms the next-month futures contract. If the opposite happens, that is if the near-month futures contract underperforms the next-month futures contract, the trader would suffer a loss. This situation would be reversed for a short Calendar Spread strategy. Under this strategy, the trader would profit if the near-month futures contract underperforms the next-month futures contract. If the opposite happens, that is if the near-month futures contract outperforms the next-month futures contract, the trader would suffer a loss.

Things to remember when initiating a Calendar Spread in futures

-

A Calendar spread involves buying near-month futures and simultaneously selling next-month futures, or vice versa

-

Both the futures positions must belong to the same underlying instrument

-

A Calendar Spread requires significantly less margin than does a naked long only or short only futures position, because it is much safer and less volatile than the latter

-

A Calendar Spread is initiated when the trader foresees the spread between two futures contracts either narrowing or widening

-

There are two types of Calendar Spread – Long Calendar Spread and Short Calendar Spread

-

A Long Calendar Spread is initiated when a trader expects the near-month contract to outperform the next-month contract

-

A Short Calendar Spread is initiated when a trader expects the near-month contract to underperform the next-month contract

-

Unlike a long futures which only benefits if underlying price rises or a short futures which only benefits if underlying price falls, a Calendar spread strategy can benefit in cases where underlying price rises as well as in cases where underlying price falls

-

When trading a Calendar Spread, a trader would realize a profit in one leg and a loss on the other

-

Net profit would be realized if gain in one leg is larger in magnitude than loss in the other leg, and vice versa

-

To exit from the spread, you would do the reverse – sell the leg in which you have established long position and buy the leg in which you have established short position

-

Because Calendar Spreads are much less risky and because they require much less margin, the potential reward under this strategy also tends to be small.

-

One could use technical charts or other parameters to trade Calendar Spreads

Next Chapter

Comments & Discussions in

FYERS Community

Sandeep Ullal commented on July 27th, 2020 at 8:12 PM

waiting for the advance lesson on iron condor adjustments.