In the previous chapter, we talked about some of the key aspects of a futures contract. These included:

-

Underlying instrument

-

Lot size

-

Total contract value, and

-

Margin

Let us continue with that discussion now and talk about other vital aspects of a futures contract. Kindly note that unless otherwise stated, explanations made would be from the point of view of stock/index futures that are traded on the NSE.

Elements of a futures contract

Price Quotation

This refers to the way in which the price of a futures contract is quoted. In case of stock futures and index futures, the price is quoted on a per share basis, similar to the manner in which it is quoted in the cash market. Meanwhile, the price of each futures contract in rounded to two decimal places and moves in multiples of ₹0.05.

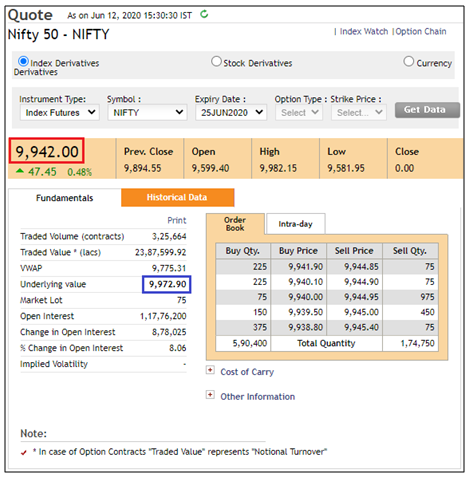

The above screenshot, taken from NSE, displays the various statistics of Nifty futures. Notice the price that is highlighted within the red box. This represents the futures price of Nifty. Meanwhile, also notice the price that is highlighted within the blue box. This represents the underlying value, that is the cash price of Nifty. Note that both the values have two digits after the decimal point, which is the standard way in which futures prices are quoted on the NSE.

Limited life

Unlike cash contracts, futures contracts have a limited life. That is, they remain in existence for a specific period of time only, as specified by the exchange. Once that time elapses, futures contracts cease to exist. On the NSE, index and stock futures each have a life of three months from the date they first commence trading.

Trading Cycle

This refers to the trading cyclesof futures contracts. Stock futures and index futures that are traded on the NSE have a three-month trading cycle. This means that at any point in time, there will be three futures contracts of the underlying instrument available for trading. The front-month contract is called the near month contract, the following or the middle contract is called the next month contract, and the final contract is called the far month contract.

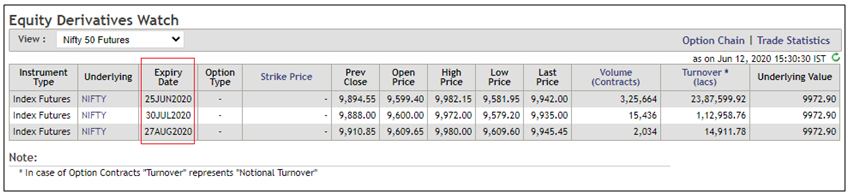

The above is the screenshot taken from the NSE website, displayingall the available monthly contracts of Nifty futures. As can be seen, at any point in time, there will be three contracts that are active. Notice the highlighted red box. Here, the June contract is the near-month contract, the July contract is the next-month contract, and the August contract is the far-month contract. As can be seen, the June contract expires on 25th June. On the day following the June contract expiry, the September contract will commence trading, which will then be the far-month contract, while the July contract will become the near-month contract. This is applicable for stock futures as well.

Settlement type

Settlement type refers to the manner in which the futures contracts settle once they expire. There are two types of settlements:cash and physical. Under cash settlement, for positions that are not closed out or rolled over by expiry, the difference(profits/losses) willbe adjusted by debiting(in case of loss) or crediting (in case of profit) the accounts of traders. For instance, if a buyer has not closed out or rolled over his futures position by expiry and has a profit of ₹20,000 based on the final settlement price of the contract, this amount would be credited to his/her account. Meanwhile, under physical settlement, if a futures contract is not closed out or rolled over by expiry, the seller will have to give delivery of the underlying asset while the buyer will have to take delivery of that underlying asset by making a full payment of the total contract value. Failure to fulfil such obligations by either parties would attract a penalty.

On the NSE, futures on indices are cash settled. That is, there is no exchange of the underlying instrument (index) but just the transfer of funds (final MTM) if the futures position in the index is not closed out or rolled over by expiry. On the other hand, futures on individual stocks are physically settled. That is, there is an exchange of the underlying instrument (stock) if the futures position in the stock is not closed out or rolled over by expiry. For example, if a trader is long 1 lot of Reliance futures and has not closed out his position by expiry, he will have to compulsorily take delivery of 505 shares of Reliance (lot size of Reliance futures = 505) by paying the full contract value(settlement price * lot size * number of lots long) and the applicable taxes.Meanwhile, if a trader is short 1 lot of Reliance futures and has not closed out his position by expiry, he will have to compulsorily give delivery of 505 shares of Reliance. To do so, the seller will need to have the required number of shares of Reliance in his Demat account. If not, it would result in a short deliverynotice (a sort of Default), in which case the seller will be charged a penalty.

Daily Settlement Price vs. Final Settlement Price

There are two types of settlement price: Daily Settlement Price and Final Settlement Price. The Daily Settlement Price is the settlement price of the futures contracts for each trading session, while the Final Settlement Price is the closing price of the underlying on the last trading day of the contract.

On the NSE, the Daily Settlement Price for index futures is calculated as the Volume Weighted Average Price (VWAP) for the last half an hour of the session. Meanwhile, the Daily Settlement Price for stock futures is calculated as the VWAP for the last half an hour of the session across exchanges for the corresponding futures contract.

Meanwhile, the Final Settlement Price for index futures is calculated as the closing price of the underlying index on the last trading session of the futures contract. On the other hand, the Final Settlement Price for stock futures is calculated as the closing price of the underlying stock across exchanges on the last trading session of the futures contract.

Expiry Day

This refers to the day when the futures contract will expire. The expiry day varies depending on the asset class. The monthly stock and index futures contracts that are traded on the NSE expire on the last Thursday of every month. In case the last Thursday of the month happens to be a holiday, the contract will expire on the trading day preceding the day of expiry.

Contract Rollover

We know from the above discussions that futures contracts have a limited life, post which they cease to exist. Leading to the expiration of a contract, the trader has to make a choice in terms of whether to:

-

Close an open futures position

-

Take physical delivery of the underlying (if applicable), or

-

Rollover the contract to the next month

In this section, we will take about rollover. Let us assume that I have a long position in Nifty futures. The expiry is just a few days away and I have to decide whether to exit the long position or rollover the existing position to the next contract (next month). What I choose will depend on a few factors, the key of them being my view on Nifty. As said, I have a long position in Nifty, meaning I am bullish on the index. If I continue to be bullish and expect the index to movehigher in the coming days/weeks, I could very well carry over my position to the next month. To do this, all I have to do is to close my existing long position in the near-month contract and simultaneously create a new long position in the next-month contract. This process is called rollover. However, if I do not have a bullish stance and expect the index to consolidate going into the next month, I could rather exit my long trade on Nifty before expiry.

Next Chapter

Comments & Discussions in

FYERS Community