The objective of this chapter is to talk about the two types of exchange rate systems that are prevalent today - the fixed exchange rate system and the floating exchange rate system. So, let us get started.

Fixed exchange rate system

Fixed exchange rate system is a system in which the central bank of a nation has a strong sayindeciding the trajectory of its currency. It is a system in which the currency of a nation doesn’t fluctuate much, because the monetary authorities keep the value of the currency fixed against other currencies, most notably against those of their key trading counterparts. The objective of keeping the value of the currency fixed is generally two-folds. One is to reduce volatility in currency movements that could otherwise harm the imports or exports of that nation. The importers and exporters of a country that is under a fixed exchange rate regime would have more clarity on the currency and need not worry much about the same than if the country were under a floating exchange rate regime. The other objective is to keep inflationary pressures in check, by periodically adjusting the value of its domestic currency. In order to keep the value of its currency fixed, the central bank will have to transact (buy or sell) huge quantity of its currency with the foreign currency against which it is fixed. To do so, the central bank must have strong foreign exchange reserves.

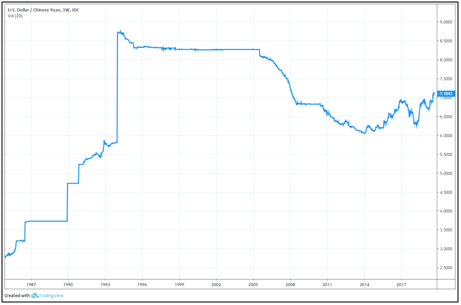

One of the most renowned countries to use the fixed-exchange rate system post the end of the Bretton Woods agreement was China. China is a global giant that has over the years emerged as the second largest economy in the world. It is known for its mammoth size of exports and for the consumption of several key commodities that it uses not only to produce the goods and products but also to meet the infrastructural needs of the nation. In order to protect its export-sector, the People’s Bank of China(PBoC) has closely managed the Yuan over the past few decades. Since 1994, the currency has been pegged to the US dollar at an exchange rate of 8.28. As can be seen from the USD/CNY chart above, this peg was in place for more than a decade. By keeping the exchange rate fixed at low, the Chinese exports became extremely competitive in the international markets and had a strong impact on significantly improving the economic prospects of the nation. Since 1994, China’s economy has expanded from $0.6 trillion to $13.6 trillion in 2018, while the GDP per capita has shot up from $1,116 to $7,754 in 2018 (Source: St. Louis Federal Reserve Bank).

Since 2005, facing heavy international pressures (especially from the US), China switched its exchange rate system from fixed to managed float, wherein it gradually permitted its currency to strengthen against the dollar for almost a decade. In 2014, the appreciation of the Yuan came to an end and since then, the currency has gradually depreciated against the dollar. Recently, the PBoC, for the first time in over a decade, permitted the Yuan to weaken beyond 7 per dollar. Over the years, China has successfully managed to keep its currency quite stable against the dollar, despite the significant dollar strength seen among other emerging market currencies. Chinahas been able to do so by limiting the Yuan’s movement within a band of 2% to the daily Yuan reference rate set each day by the PBoC.Besides China, there are other countries in the world that follow a fixed exchange rate system. To name a few - Hong Kong, Qatar, Saudi Arabia, Bahrain, and UAE follow a fixed exchange rate system.

As already stated, central banks must have enough foreign exchange reserves to effectively manage the fixed exchange rate system. If the central bank runs out of reserves, it could give rise to an economic crisis, like the one that happened during the Asian and the Russian currency crisis in 1997 and 1998, respectively.

Floating exchange rate system

The other type of exchange rate system is the floating exchange rate system. Under this system, currencies are permitted to float freely in the forex market depending upon the prevailing demand and supply conditions. Most of the developed countries in the world today use the floating exchange rate system, wherein market forces rather than the government determine the value of the currency. Having said that, even under the floating exchange rate system, the government can and do occasionally intervene in the Forex market, if needed. Switzerland is one such example wherein the country intervened despite being under the floating rate regime. Back in 2011, for almost four years, the Swiss Franc was witnessing a wave of inflows against the Euro, because of the global financial and the euro zone crisis. In order to prevent this from damaging the Swiss economy, which is heavily reliant on exports and hence suffers when the Franc strengthens, the Swiss National bank (SNB) intervened in the Forex market by establishing a floor for the EUR/CHF currency pair, causing the Franc to depreciate sharply against the Euro in the following days. Eventually however, this peg was removed in 2015.

.png)

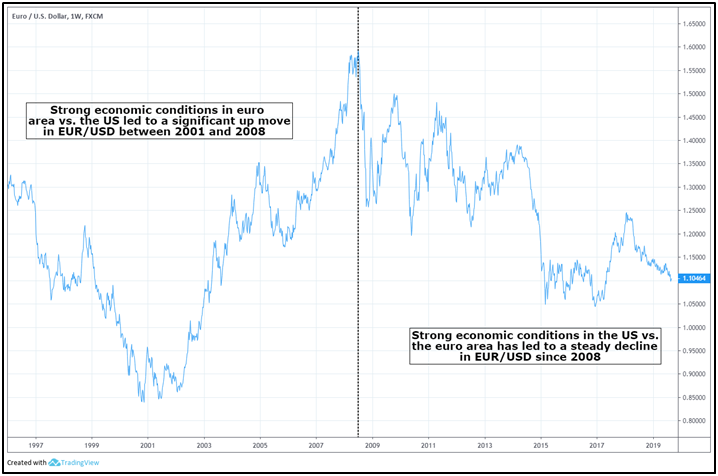

In a floating exchange rate system, currency movements are determined by prevailing demand and supply, which in turn is determined by economic conditions prevalent between two nations. For instance, the movement in the currency pair EUR/USD would be determined by the economic health of the euro area and the US. If economic conditions in the euro area are better than those in the US, the euro will likely appreciate against the dollar, and vice versa. Currencies that are under the floating exchange rate system will also be quite sensitive to very short-term developments that take place during the day, such as when some news or economic data come in.

The above chart shows the movements of EUR/USD, a currency pair wherein both the currencies are under the floating exchange regime. Contrast this chart with that of USD/CNY shown earlier. Notice that a pair that is under the floating system is more sensitive and reflects the prevailing demand-supply situation much better than the one that is under a fixed system.

The Indian Rupee: A managed float currency

The Indian Rupee is a managed float currency, wherein movements in the currency are determined by the prevailing market forces of demand and supply. The RBI closely monitors the Rupee and intervenes in the Forex market only when needed, such as at times when volatility is too high or when the Rupee’s movement has become too one-sided in a short span of time. On most other occasions, the rupee movement is determined by the market, as can be seen from the chart below.

Capital and Current account convertibility

In the context of currencies, the term convertibility refers to the ease with which one currency could be exchanged for another for any purpose. If a currency is fully convertible, it could be exchanged freely (i.e. without any restrictions) at the prevailing market price, irrespective of the purpose (assuming the purpose is legal) and the amount. On the other hand, if a currency is not fully convertible, there are certain restrictions towards its conversion with other currencies.

There are two types of convertibility: current account convertibility and capital account convertibility. Both these convertibility refer to the ease with which a local currency could be exchanged for a foreign currency, and vice versa, when doing international transactions. However, they differ in terms of the purpose for which the international transactions are done. In case of current account convertibility, these international transactions are done for purposes such as foreign trade and invisibles (such as services, interest on loan, interest on other investments, remittances towards meeting family expenses, etc). Meanwhile, in case of capital account convertibility, these international transactions are carried on for purposes such as making investments (purchase and sale) in financial assets (shares, bonds, property etc.), converting proceeds from dividend and interest payments, directly investing in companies and businesses of other countries etc.

There are advantages and disadvantages of currency convertibility. The advantage is that convertibility facilitates easy movement of goods between borders as well as gives a nation increased access to foreign capital. The increase in trade and investment flows would boost economic growth and generate employment opportunities in the country. The drawback is that in case the convertibility is poorly implemented or if the nation is not equipped to efficiently handle a fully convertible currency, it could lead to major macro-economic problems such as increased volatility in the domestic financial markets, surge incapital flows into and out of a nation, sharpswings in the value of the domestic currency, high inflation etc.

The chart below shows movement in the Thailand Baht (which was a pegged and a fully convertible currency back then) against the Dollar during the time of the Asian financial crisis in 1997. Observe how the Thai currency plunged more than 50% against its US counterpart in a quick span of time. The plunge came amidsta wave of speculative attack on the nation’s assets because of deteriorating economic conditions in the nation and as the government lacked enough foreign exchange reserves to maintain the Baht’s peg against the dollar. As the Baht was fully convertible back then, foreigners were able to exit the nation in record numbers without much restrictions, causing the currency to plummet and forcing the government to remove the peg and change to a floating regime. The problems that originated in Thailand eventually spread to other east Asian countries as well, significantly impacting the currencies of those Asian countries that were fully convertible. One important lesson to learn from the Asian currency crisis was that if a nation is not fully equipped to handle currency convertibility, it could give rise to significant economic crises in future.

So, summing up in simple terms, current account convertibility refers to currency conversion for purposes related to trade flows, while capital account convertibility refers to currency conversion for purposes related to investment flows.

The Indian Rupee: A partially convertible currency

The Indian Rupee is a partially convertible currency. This is because it is fully current account convertible, but only partially capital account convertible. Because the Rupee is fully current account convertible, there are no restrictions for international transactions thatpertain to trade (imports/exports) and invisibles. In other words, payments and receipts relating to current account can be converted from foreign to domestic currency, and vice versa,at the prevailing market exchange rate that is quoted by authorized dealers, such as banks. Meanwhile, even in case of capital account transactions, there are little regulations for capital flows into and outside of India up to a certain limit. However, regulatory approval by the RBI is needed in case of large capital transactions that exceed the limits prescribed by the government. These restrictions apply to both Indians who want to make financial investments abroad as well as to foreigners who want to make financial investments in India.

Next Chapter

Comments & Discussions in

FYERS Community

Ashwin commented on September 18th, 2019 at 9:55 PM

How does Exchange rate respond to the Monetary policy Contraction if price is totally flexible?

tejas commented on September 20th, 2019 at 5:15 PM

Ashwin, Contractionary monetary policy is exercised to deal with high inflation. When the central bank increases the interest rates, it reduces the supply of money in the economy. In theory, with a reduced money supply, the value of the currency should go up. Also, raising rates will increase govt. bond rates and make investing attractive from foreign investors thereby further increasing the domestic currency strength.

akshay commented on September 18th, 2019 at 9:57 PM

What method can one use to predict currency exchange rate?

tejas commented on September 20th, 2019 at 5:19 PM

You'll have to read the following chapters in detail to get a better grip on that:

- Chapter 3 - Factors that drive the forex market

- Chapter 4 - Analysing Economic Data

Harsha Vardhan commented on September 19th, 2019 at 10:31 AM

Very useful information for the beginner like me. Thanks for writing this sir. You are educating youngster like us and creating lot of interest in the stock market. Looking forward for more informative article like this.

tejas commented on September 20th, 2019 at 5:22 PM

Hi Harsha Vardhan,

Thanks for appreciating our efforts. WIll write more in the near future! Stay tuned and do share it with your friends, colleagues or teachers if you think they would find it useful too.

Dr.Tushara Rao commented on September 19th, 2019 at 10:34 AM

I am always busy seeing patients and reading medical books. This is so refreshing to learn new things about the stock market. Sir, what I like about your writing is that you make it so simple. This really helps for a beginner like me. Thanks for educating us. Look forward to read more.

tejas commented on September 20th, 2019 at 5:23 PM

You're welcome Dr. :)

Sudhakar commented on September 19th, 2019 at 10:38 AM

I am in prawn culture and exports. This is very useful for me. Thanks for making me to understand and thanks a lot for sharing.

Ramya Choudhary commented on September 19th, 2019 at 7:00 PM

Which currency system do you think is more advantageous for depreciating the currency?

tejas commented on September 20th, 2019 at 5:26 PM

1. For a country which is in the doldrums, fixed exchange rate works best as they can peg the value of their currency to a more stable currency.

2. For a country that has built sufficient foreign reserves, stable GDP growth, partial convertibility on the current account, a floating rate is more suitable.

3. For a developed country which has a lot going for it, obviously a fully convertible floating rate is most suitable.

Milind commented on September 19th, 2019 at 7:07 PM

Please explain about creating a calendar spread with USDINR and How to calculate annual volatility in USDINR?

Thanks in Advance.

Shriram commented on January 28th, 2020 at 10:15 PM

For understanding how to calculate annual volatility, you can refer to the chapter on Volatility in the Options module.

As far as calendar spread is concerned, you can create a calendar spread in USDINR futures by buying a USDINR futures contract having one expiry and simultaneously selling a USDINR futures contract having a different expiry. For example, buying USDINR January futures and simultaneously selling USDINR February futures is an example of calendar spread.

Spread between two futures contract with differing maturities can be calculated as: farther-term futures contract minus near-term futures contract. For instance, if USDINR Jan fut is currently trading at 70.0000, while Feb fut is currently trading at 70.5000, the spread between the two is 70.5000-70.0000 = 0.5000

If you expect the spread to narrow down, you can buy the near-term contract and simultaneously sell the farther-term contract. This strategy is also known as Bull futures spread.

Alternatively, if you expect the spread to widen, you can sell the near-term contract and simultaneously buy the farther-term contract. This strategy is known as Bear futures spread.

Vivek commented on September 30th, 2019 at 10:51 PM

One of best information which I was looking in the other website, I found here all realative information about currency market and it's fictionallty. Thank you for the post.

Shriram commented on January 28th, 2020 at 10:16 PM

Hi Vivek, thank you for the feedback!

Julius commented on August 28th, 2020 at 11:28 AM

How does exchange rates affect policy decisions?

Abhishek Chinchalkar commented on August 31st, 2020 at 8:19 AM

Hi Julius, exchange rate can have an impact on inflation. For instance, if the Rupee depreciates against the dollar, it makes imports of goods and services more expensive. This in turn can directly as well as indirectly increase the level of inflation within the economy If this rise in inflation moves beyond the comfort zone of the central bank, it tends to put upward pressure on interest rates. The opposite is also true when the Rupee appreciates against the dollar.