History of Commodity Derivatives

The history of commodity derivative trading dates to centuries ago, long before the advent of stock and bond trading. At that time, the primary purpose of trading commodities was to hedge the agricultural produce against price uncertainties. In fact, the reason why derivate trading began was to lock the supply and price of commodities and to safeguard farmers against crop failures. Back then, trading was done in Over-the-Counter (OTC) markets – two parties to the trade used to meet at some pre-determined place and decide the terms of the derivate contract. However, as commodity trading grew larger and more sophisticated in terms of size and volume and as credit risk remained a serious problem in OTC markets, the need for a more organized derivative market gained prominence as time progressed.

This eventually led to the formation of one of the first known futures and options exchange in the world. In 1848, the Chicago Board of Trade (CBOT) was formed in Chicago, United States, by a group of prominent grain traders. Back then, only agricultural commodities such as wheat, corn, cattle, and pigs were tradedon the CBOT. However, as the size of commodity markets grew, not only were more agricultural commodities introduced and traded, but several non-agricultural commodities also came into picture, such as metals and energy products.Today, there are several commodity exchanges around the world that attract not only hedgers but also speculators and arbitragers.

The MCX was established in 2003 and has since become India’s largest commodity derivative exchange with an average daily turnover of ₹21,193 crore in FY18 (single side). The MCX has a virtual monopoly in the trading of non-agricultural commodities namely precious metals, energy, and base metals. The NCDEX was established in 2003. As of March 2018, the NCDEX offered trading in 27 commodity contracts, and had an average daily turnover of around ₹2,377 crore in FY18. While NCDEX does offer trading in non-agricultural commodities, it is known for and has a strong monopoly in the trading of agricultural commodities. The ICEX, meanwhile, is a relatively new exchange and is yet to prove its mettle in the commodity derivatives market.

Spot vs. Derivative trading

Commodity trading can be of two types: spot and derivative.

Spot trading, also referred to as physical trading, involves trading of commodities that are available for immediate delivery (usually settlement takes place within two days). The price at which the transaction occurs is referred to as the spot price.

On the other hand, derivate trading of commodities involves trading of commodities whose settlement takes place into future at a pre-determined price. The period of trading ranges from a few days to several months, depending upon the type of commodity traded and other factors. The price at which such a transaction occurs is referred to as the futures price.

Futures price is a derivative of spot price for any commodity. Depending on various factors, futures price can trade below, at, or above the spot price. When futures price is trading above spot price, the situation is known as contango; and when futures price is trading below spot price, the situation is known as backwardation. We will discuss each of these concepts in more details later. Futures price of a commodity can be derived using the following formula:

F = S*e^((R+S-C)*t)

Where,

F = futures price

S = spot price

E = 2.71828

R = risk-free rate of return (%)

S = storage cost (%)

C = convenience yield (%)

T = time to expiration (in years)

Generally, commodity derivatives that are traded on exchanges around the world are usually of two types: futures and options.

A commodity futures contract is a contract between two parties to buy or sell a commodity at a specific time in the future for a specific price. It is similar to a forward contract but with a few key differences, which are shown in the table below:

|

Futures |

Forwards |

|

Exchange traded contracts |

Private contracts between two parties |

|

Standardized contracts |

Customized contracts |

|

No element of counterparty risk |

Element of counterparty risk |

|

Settled every day (mark-to-market) |

Settled at the end of the contract |

|

Highly regulated instruments |

Less regulated instruments |

The biggest advantage of futures contract is that as these are traded on an exchange, there is no element of counterparty (credit) risk. Below image shows a sample highlight of a few commodity futures contracts that are traded on the MCX (source: ).

A commodity options contract is a contract that gives the buyer (the holder of the option) the right, but not an obligation, to buy or sell a commodity at a specific time in the future for a specific price, called the strike price or the exercise price. An options contract is of two types: call options contract and put options contract. A call optionscontract gives the buyer the right to buy a commodity in the future for a specific strike price, while a put option gives the buyer the right to sell a commodity in the future for a specific strike price. Below image shows a sample highlight of a few commodity options contracts that are traded on the MCX (source: www.mcxindia.com).

Below mentioned are some basic option terminologies to remember:

-

Call option: Gives the buyer the right to buy a commodity in the future for a specific strike price.

-

Put option: Gives the buyer the right to sell a commodity in the future for a specific strike price.

-

Long position: Implies taking a buy position in options – either buying a call option or a put option.

-

Short position: Implies taking a sell position in options – either selling a call option or a put option.

-

Strike price: Also known as the exercise price, it refers to a pre-agreed price at which a commodity will be bought (in case of call option) or sold (in case of put option) on expiration day.

-

Option price: Also known as option premium, this is the price that an option buyer must pay to an option seller for acquiring the right to the contract. It comprises of two components – time value and intrinsic value.

-

In-the-money (ITM): A call option is said to be ITM if the current price of the commodity is above the strike price, while a put option is said to be ITM is the current price of the commodity is below the strike price.

-

At-the-money (ATM): A call/put option is said to be ATM if the current price of the commodity is equal to the strike price.

-

Out-the-money (OTM): A call option is said to be OTM if the current price of the commodity is below the strike price, while a put option is said to be OTM is the current price of the commodity is above the strike price.

-

Intrinsic value: This refers to the amount an option contract is ITM. If the option is OTM, intrinsic value is zero. For a call/put option that is ITM, intrinsic value is calculated asthe positive difference between current price of the commodity and the strike price.

-

Time value: This is the difference between the option price and the intrinsic value. If an option is OTM, option price is equal to time value (as intrinsic value is zero). The greater the time to expiration, the higher will be the time value, and vice versa.

-

Breakeven price: This is the price at which the buyer of an option will be at breakeven, i.e. neither making a profit nor a loss. For a call option, the breakeven price is equal to strike price plus the premium paid by the buyer; while for a put option, the breakeven price is equal to strike price minus the premium paid by the buyer.

Let’s now simplify all this with the help of a couple of examples.

Example 1 (put option):

p style="text-align: justify;">At the time of writing, a put option on MCX gold having a strike price of ₹33000, underlying value of ₹33390, and an expiry of 27-March-19 is trading at ₹191.

As this option is OTM (remember: a put option is OTM if underlying price is above the strike price), it has only time value and no intrinsic value. As such, the entire premium of ₹191 is the time value component.

If a person buys 1 lot of this contract, his breakeven point would be ₹32809 (strike price of ₹33000 – premium of ₹191). He would profit only if the underlying price drops below ₹32809 by the time of expiration.

If the price closes at, say, ₹33500 on expiration, the buyer would let the option expire worthless, in which case his loss would be to the tune of the premium paid i.e. ₹191. As the lot size of gold on the MCX is 100, this would mean a loss of ₹19100 per lot. The seller would get to keep the premium and therefore profit ₹19100 per lot.

On the other hand, if the price closes at, say, ₹32500 on expiration, the buyer would exercise the right to sell gold at the strike price i.e. ₹33000. As he is selling at a price above the prevailing underlying price, he would make a profit to the tune of ₹309 (strike price of ₹33000 – underlying price of ₹32500 – premium of ₹191). His profit per lot would be ₹30900, which would also be the seller’s loss per lot.

Example 2 (call option):

At the time of writing, a call option on MCX gold having a strike price of ₹33000, underlying value of ₹33390, and an expiry of 27-March-19 is trading at ₹530.

As this option is ITM (remember: a call option is ITM if underlying price is above the strike price), it has an intrinsic value of ₹390 (underlying price of ₹33390 – strike price of ₹33000). As the option price is ₹530, the remaining portion i.e. ₹140 is the time value component.

If a person buys 1 lot of this contract, his breakeven point would be ₹33530 (strike price of ₹33000 + premium of ₹530). He would profit only if the underlying price rises above ₹33530 by the time of expiration.

If the price closes at, say, ₹32800 on expiration, the buyer would let the option expire worthless, in which case his loss would be to the tune of the premium paid i.e. ₹530. This would mean a loss of ₹53000 per lot. The seller would get to keep the premium and therefore profit ₹53000 per lot.

On the other hand, if the price closes at, say, ₹33800 on expiration, the buyer would exercise the right to buy gold at the strike price i.e. ₹33000. As he is buying at a price below the prevailing underlying price, he would make a profit to the tune of ₹270 (underlying price of ₹33800 – strike price of ₹33000 – premium of ₹530). His profit per lot would be ₹27000, which would also be the seller’s loss per lot.

Things to note from the above two examples:

-

A buyer of call option would profit only if underlying price rises above the breakeven point, while a buyer of put option would profit only if underlying price drops below the breakeven point.

-

A buyer of a call option has a bullish view on the underlying, while the seller of a call option has a bearish view.

-

A buyer of a put option has a bearish view on the underlying, while the seller of a put option has a bullish view.

-

Maximum profit for an option buyer is potentially unlimited, while maximum loss is limited to the extent of premium paid.

-

Maximum profit for an option seller (also known as option writer) is limited to the extent of premium received, while maximum loss is potentially unlimited.

-

As the number of days to expiration reduce, the time value drops and eventually approaches to zero on expiration.

Types of commodities that are traded

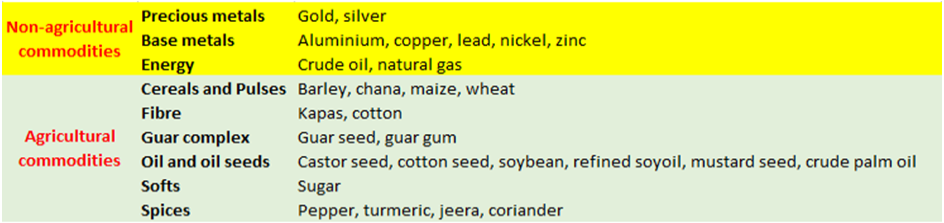

Broadly speaking, commodities can be divided into two groups: agricultural commodities and non-agricultural commodities.

Agricultural commodities include commodities that are grown or cultivated. Examples include soybean, wheat, cotton, corn, barley, coriander, turmeric etc. Agricultural commodities could also include commodities that are derived from animals such as pork, milk, hogs etc. Given their perishable nature, these commodities usually have a relatively short-shelf life and as such have shorter maturity periods.One of the major factors that determine the price of agricultural commodities isweather. Given that weather conditions follow specific patterns in different regions around the world, these commodities tend to be highly seasonal. Any unexpected change in weather forecast can have a significant impact on the supply of these commodities, and subsequently on their prices. On a macro-economic front, agricultural prices are closely monitored and scrutinized by governments and central banks of all countries, given that they have a direct influence on food prices and inflation.In India however, not all agricultural commodities are traded on the derivatives exchange given the political sensitivity of these commodities due to their impact on food prices and inflation.

Non-agricultural commodities include commodities that are not cultivated bur rather mined. These can broadly be divided into two groups: metals and energy. Metals can again be divided into two groups namely precious metals and base (industrial) metals. Precious metals are metals that are considered quite valuable due to their scarcity. The most commonly traded precious metals are gold and silver followed by platinum and palladium. The latter two also have industrial uses especially in the auto-catalyst segment. Base metals are those metals that are abundantly available around the planet and those that are heavily used for industrial and consumption purposes. The most commonly traded are copper, aluminium, zinc, nickel, lead, and steel. The other type of non-agricultural commodities are energy products. These include crude oil, natural gas, and electricity. Unlike agricultural commodities, non-agricultural commodities are non-perishable and hence can be stored for as long as warranted. Also, these commodities are not as widely impacted by weather conditions. Instead, geopolitical developments, macroeconomic factors, and mining and supply-side forces tend to have a larger impact on the prices of non-agricultural commodities.

In India, both agricultural and non-agricultural commodities are traded on the exchanges. The MCX is more renowned for the trading of non-agricultural commodities in terms of volume and market share, while the NCDEX is more renowned for the trading of agricultural commodities. The most commonly traded commodities on the Indian bourses are mentioned below:

Participants in the commodity derivatives

Broadly speaking, there are three types of participants in commodity derivatives – hedgers, speculators, and arbitrageurs. Each participant has a differing set of objectives and risk appetite. While some are in the markets only to safeguard their risk, others trade with the intention of earning profits. The entities that participate in commodity markets include individuals, corporates, governments, funds etc. Each of these three types of participants are discussed below.

Hedgers

Hedgers participate in the commodity market with the intention of reducing their underlying risk in the spot market. These participants are usually producers and consumers of commodities and are in the business of hedging not to make money but to safeguard their risk. They could include individuals such as farmers or institutions such as metal or crude oil producing companies.

The simplest example is the case of a farmer, say wheat farmer. For him, the risk is of wheat price falling from the time the sowing begins till the time of harvesting. In such a scenario, the farmer will be forced to sell at a lower price, and thereby suffer losses on the crop. In order to safeguard his position in the spot market, this farmer can hedge his exposure by initiating a short position on wheat in the derivatives market (futures or options, or a combination of both). By hedging his exposure in the derivatives market, he would lock in a price and thereby hedge his risk to a significant extent.

Another example would be the case of a company that makes biscuits, for instance Britannia. Such companies need wheat as an ingredient to make biscuits. For them, the risk is of wheat price rising as this would increase their cost of production and thereby squeeze profit margins. Given the volatile nature of commodity prices, this company can hedge its exposure by initiating a long position on wheat in the derivatives market.

Speculators

While hedgers participate in the commodity market to hedge their risk exposure, speculators are in the business with the primary objective of making a profit. By assuming the risk of market price fluctuation, speculators provide liquidity to the markets. Unlike a hedger who has an underlying exposure in the spot market, a speculator does not have exposure in the spot market. A speculator just has a view on the underlying commodity and trades according to that view to make money.

For instance, if a speculator is bullish in gold, he will initiate a long position in gold futures (or options) with the objective of riding the up move in gold prices. Generally, speculators do not take delivery of the commodity. They either close out their positions before expiry of the derivatives contract or roll it over to the next contract. The magnitude of the trade depends upon the objective and risk profile of speculators. While some enter and exit their positions in minutes, others may hold on to their positions for weeks or months.

Arbitrageurs

Another type of participants in the commodity markets are arbitrageurs. The objective of an arbitrageur is to earn risk-free profits from price inefficiencies that exist between a commodity in two different markets. To do so, an arbitrageur simultaneously enters a position in one market and an opposite position on the same commodity in another market with the intention of capturing the price differential between the two when the price converge.

For instance, if an arbitrageur sees that the price of gold futures on MCX is ₹30000 and that on NCDEX is ₹30025, he may simultaneously buy a contract on the MCX, where the price of gold is undervalued, and sell a contract on the NCDEX, where the price of gold is overvalued. If things remain constant until the time he cuts both the positions, he would capture a ₹25 profit, minus other transactional costs. Arbitrage can be done between spot and futures markets too.

That said, with the advancement in technology, the arbitrage opportunities that are available today are extremely limited in numbers. Any price discrepancy that occurs between identical assets/markets are eliminated within seconds by computer-driven algorithms that are pre-programmed by large institutions and professionals. As such, they are quickly eliminated by systems before they come to the notice of retail and individual traders.

Stocks vs. Commodities

There are a few important differences between commodities and stocks. Some of these are mentioned below:

Paper assets vs hard assets

One of the most notable difference between commodities and stocks is the tangibility aspect. Stocks are financial, paper assets; while commodities are hard, physical assets. Stocks do not have a physical presence. Instead, they exist only on paper, which represents an ownership in the company. Stocks do not have a fixed life and they exist as long as the company exists. On the other hand, commodities are real assets, some of which have a finite life, such as agricultural commodities. Because of their tangible nature and usefulness, they are limited in supply and as such, can never become useless or available free of cost.

Given that stocks are paper assets, when a person or an entity buys stock of a company in the cash segment, he can hold it for as long as he wants to or until the time the company is in existence. However, trading in the cash (spot) segment of commodity market is quite different than trading in stocks given that commodities are physical assets. Buying in the cash segment means taking delivery of a commodity, which is not feasible for all as it requires considerable storage space and other costs.As such, trading in the commodity spot market is usually restricted to institutions that have an underlying exposure to the commodity.

Instead, most of the trading in commodities takes place in the derivatives market, as there is no compulsion to take delivery of commodities. As stated earlier, participants in the derivatives market include those who have an underlying exposure to the commodity (hedgers), those who do not have any exposure to the commodity but are there just to earn a profit (speculators), and those who try to earn a risk-free profit by taking advantage of price discrepancy (arbitrageurs).

Some commodities on the MCX are cash settled i.e. on expiration, the difference is adjusted and settled in cash. Crude oil and natural gas are two such commodities where settlement is done by cash. Other commodities on the MCX are physically settled, i.e. if the contract is not settled before expiry, the seller must give delivery of the commodity to the buyer once the full contract amount has been paid by the buyer. Examples include precious metals and base metals. Of the commodities where physical settlement takes place, most of the trading is done in the futures platform rather than options platform, as the latter are still not liquid instruments in India and were only recently introduced by the MCX in select commodities.

The time element

As already stated in the previous section, another difference between stocks and commodities is the time element. Stocks that are traded in the cash segment can be held on by investors to infinity as they do not have a fixed life and exist as long as the company they represent exists. However, trading of commodities in the cash segment is done for the eventual purpose of consumption. For instance, trading of agricultural commodities is done for the purpose of feeding the world’s population, trading of industrial metals is done for the purpose of construction and economic development, trading of crude oil is done for the purpose of fuelling and others, etc. An exception here could be precious metals. For instance, while a small portion of gold is consumed for industrial purposes, a significant portion of the metal’s demand is for jewellery and investment purpose rather than consumption purpose.

Type of settlement

Financial derivatives are instruments that exist just on paper. On expiration, they are mostly settled in cash, or in some cases, by delivery of the underlying financial instrument. As such, there are no complex elements involved in financial derivative contracts such as physical settlement, need for warehousing, storage costs etc.However, settlement of commodity derivatives is quite different and more complex than that of financial derivatives. In the case of commodity derivatives, the seller who intends to give delivery of the commodity must deposit that commodity at the exchange designated warehouses. Similarly, the buyer who intends to take delivery of the commodity must go to the warehouse to take delivery of the commodity. The commodity being deposited at the warehouse must meet the exchange requirements in terms of quality and quantity.

As can be seen, as commodity derivatives are instruments that can be settled physically, they are subject to elements such as warehousing and quality of the underlying commodity, elements that do not exist in financial derivatives. As financial derivatives exist on paper only, they do not require any warehouse for storage, and do not have the quality factor unlike commodities.

Summary

-

In India, the three major exchanges that offer commodity derivative trading are Multi-Commodity Exchange of India Ltd (MCX), National Commodity and Derivative Exchange Ltd (NCDEX), and Indian Commodity Exchange Ltd (ICEX).

-

Spot trading, also referred to as physical trading, involves trading of commodities that are available for immediate delivery (usually settlement takes place within two days). The price at which the transaction occurs is referred to as the spot price.

-

Derivate trading of commodities involves trading of commodities whose settlement takes place into future at a pre-determined price.

-

A commodity futures contract is a contract between two parties to buy or sell a commodity at a specific time in the future for a specific price.

-

A commodity options contract is a contract that gives the buyer (the holder of the option) the right, but not an obligation, to buy or sell a commodity at a specific time in the future for a specific price, called the strike price or the exercise price.

-

Some important terminologies pertaining to options include call option, put option, long position, short position, strike price, option price, in-the-money option, at-the-money option, out-the-money option, intrinsic value, time value, and breakeven price.

-

A buyer of a call option has a bullish view on the underlying, while the seller of a call option has a bearish view; a buyer of a put option has a bearish view on the underlying, while the seller of a put option has a bullish view.

-

Maximum profit for an option buyer is potentially unlimited, while maximum loss is limited to the extent of premium paid; maximum profit for an option seller (also known as option writer) is limited to the extent of premium received, while maximum loss is potentially unlimited.

-

A buyer of call option would profit only if underlying price rises above the breakeven point, while a buyer of put option would profit only if underlying price drops below the breakeven point.

-

Agricultural commodities include commodities that are grown or cultivated. Examples include soybean, wheat, cotton, corn, barley, coriander, turmeric etc. Agricultural commodities could also include commodities that are derived from animals such as pork, milk, hogs etc.

-

Non-agricultural commodities include commodities that are not cultivated bur rather mined. These can broadly be divided into two groups: metals and energy.

-

In India, both agricultural and non-agricultural commodities are traded on the exchanges. The MCX is more renowned for the trading of non-agricultural commodities, while the NCDEX is more renowned for the trading of agricultural commodities.

-

Hedgers participate in the commodity market with the intention of reducing their underlying risk in the spot market. These participants are usually producers and consumers of commodities and are in the business of hedging not to make money but to safeguard their risk.

-

While hedgers participate in the commodity market to hedge their risk exposure, speculators are in the business with the primary objective of making a profit.

-

Another type of participants in the commodity markets are arbitrageurs. The objective of an arbitrageur is to earn risk-free profits from price inefficiencies that exist between a commodity in two different markets.

-

One of the most notable difference between commodities and stocks is the tangibility aspect. Stocks are financial, paper assets; while commodities are hard, physical assets.

-

Stocks that are traded in the cash segment can be held on by investors to infinity as they do not have a fixed life and exist as long as the company they represent exists. However, trading of commodities in the cash segment is done for the eventual purpose of consumption.

-

On expiration, financial derivatives are mostly settled in cash, or in some cases, by delivery of the underlying financial instrument. As such, there are no complex elements involved in financial derivative contracts such as physical settlement, need for warehousing, storage costs etc.

-

Settlement of commodity derivatives is quite different and more complex than that of financial derivatives. In the case of commodity derivatives, the seller who intends to give delivery of the commodity must deposit the commodity at exchange designated warehouses.

Next Chapter

Comments & Discussions in

FYERS Community

soorya commented on May 9th, 2019 at 7:37 PM

This is what really traders community required , really a great platform built by fyers , fyers is getting many step ahead in broking industry by understanding the needs and requirements of traders and investors

tejas commented on May 9th, 2019 at 10:30 PM

Glad you find it useful Soorya. Well, just working on things which we think are important. Thanks for your patience so far and stay tuned. There's more coming!

Pritham Erukala commented on May 10th, 2019 at 8:53 PM

Hey Tejas, do you have plans on explaining these concepts through videos?

tejas commented on June 14th, 2019 at 1:09 AM

Hi Pritham, Not as yet. We're going to write about a lot of things. Creating videos is not on the cards yet.

Neha commented on May 13th, 2019 at 2:38 PM

Absolutely brilliant efforts are taken here. The modules offers so much knowledge on Commodity Trading. Loved it. Thank you !..

tejas commented on June 14th, 2019 at 1:10 AM

Thanks, Neha! Yes, it's quite some effort writing in detail. Glad you like it.

Ramya commented on May 13th, 2019 at 2:42 PM

Fyers doing great Job. You guys are educating the novice without them having to attend the seminars. Kudos to the team, keep up the awesome work and hope to see more topics soon :)

tejas commented on June 14th, 2019 at 1:11 AM

Hey, I just saw your message. Yes, we have added many chapters since your last comment. Do check them out.

Tara commented on May 13th, 2019 at 2:50 PM

Big Thumbs Up!.. Very useful source for the beginners in Indian Trading Market.

tejas commented on June 14th, 2019 at 1:11 AM

Do spread the word.

vijay commented on May 22nd, 2019 at 2:30 AM

Thanks for the detailed explanation. Now i come to know about commodity markets and the difference between commodity markets and capital market.

tejas commented on June 14th, 2019 at 1:12 AM

Vijay, looks like you are a beginner. I strongly recommend you spend a lot of time reading the basic concepts. If you need knowledge on fundamentals, make sure to read Gopal Kavalireddi's content on the introduction to capital markets and fundamental analysis.

Mahesh commented on May 22nd, 2019 at 3:02 PM

Thank you Fyers, I was trading in equity from last 3-4 years. With your support, I have started trading in commodities.

tejas commented on June 14th, 2019 at 1:15 AM

Hi Mahesh, Since you are just starting out in commodities, make sure to trade in the smaller lots using the mini contracts. That way, you won't freak out with large MTM fluctuations.

Rajesh commented on July 15th, 2019 at 11:16 PM

Does fyers allow the clients to take Commodity for delivery?

tejas commented on August 14th, 2019 at 4:53 PM

As per our risk management policies, we square-off positions to avoid unintended deliveries. This is because most traders want to avoid deliveries and the complex tedious tasks that come along with it apart from the margin requirements.

tejas commented on August 14th, 2019 at 8:40 PM

Hi Rajesh, no we don't. In fact, our clients stay away from deliveries.

Gopal commented on July 15th, 2019 at 11:19 PM

Why there is no information about ComRIS?

tejas commented on December 30th, 2019 at 9:00 PM

This chapter is more about basic concepts.

nishikant kumar commented on December 24th, 2019 at 8:20 PM

commodity ar currecy ke liye kitna money fund honi chahiye,trade ke liye how i learn

tejas commented on December 30th, 2019 at 9:01 PM

Hey Nishikant, For more information about funds required to trade, check out our Margin calculators. If you are going to use Bracket Orders or Cover Orders, the margin requirement is really less.

Sumit commented on January 9th, 2020 at 2:09 AM

Which commodities are cash settled ?

Shriram commented on January 23rd, 2020 at 10:12 PM

Among the non-agro commodities, Crude oil and Natural gas are cash settled