Basis, contango, and backwardation

In the previous chapter, we talked about hedging using futures. In this chapter, we will be covering concepts related to basis, contango, and backwardation. These concepts are especially important in commodities given that commodities are physical assets that have a limited supply and as such are heavily influenced by the demand and supply scenario prevailing across the globe. But what exactly do these terms refer to? We will take about them in more detail over the course of this chapter.

Basis

The term basis refers to the difference between spot price of a commodity and its futures price. Put it in the form of an equation, basis can be defined as:

Basis = spot price of a commodity in the local market – the futures price of that commodity

Basis can be positive or negative. Basis is positive when spot price is above the futures price, and negative when spot price is below futures price. For instance, if the price of spot gold in local market is ₹32,000 and the price of a nearby gold futures contract on the MCX is ₹32,050, there is a negative basis of ₹50. On the other hand, if the price of spot gold in local market is ₹32,000 and the price of a nearby gold futures contract on the MCX is ₹31,950, there is a positive basis of ₹50.

There are several factors that influence basis, such as:

- Local demand and supply conditions

- Quality and other aspects of the commodity

- Storage and insurance costs

- Transportation costs etc.

In an ideal world, as the number of days left to the expiration of a futures contract reduces, the basis should narrowtoo. However, this may not always happen for the reasons mentioned above (factors that influence basis). Over the life of a futures contract, the basis between the spot and the futures might not necessarily narrow but could widenas well. In other words, as the time passes, the basis could change in either direction. Depending on this change, the basis could either be strengthening or weakening. If the spot price of a commodity is outperforming the futures price, the basis is said to be strengthening. Conversely, if the spot price of a commodity is underperforming the futures price, the basis is said to be weakening.Think of this from a number line perspective. If the basis is moving to the right of the number line, it is said to be strengthening. If the basis is moving to the left of the number line, it is said to be weakening.

As the expiration of the futures contract nears, the basis eventually narrows. At the time of expiry, the spot price and the futures price converge, and the basis becomes zero. If the basis has not narrowed closer to expiry, it would give rise to arbitrage opportunities, wherein arbitragers would buy an under-priced instrument and simultaneously sell an over-priced instrument in order to profit from the price imbalance. This would continue as long as the arbitrage opportunity exists, thereby eventually causing the basis to narrow and become zero at the time of expiration of the futures contract.

Strengthening of basis

As already stated, the basis is said to strengthen when the spot price of a commodity is outperforming the futures price. This can occur in any of the following manner:

-

Both the spot price and the futures price are increasing, but the spot price is increasing faster than the futures price

-

Both the spot price and the futures price are decreasing, but the spot price is decreasing slower than the futures price

-

The spot price is unchanged, while the futures price has decreased

-

The spot price has increased, while the futures price has decreased

-

The spot price has increased, while the futures price is unchanged

Anunexpected strengthening of the basis from time benefits the seller of a commodity, such as a commodity producer. This is because the outperformance of the spot price relative to the futures price enables the seller to fetch a higher selling price from the local spot market. For instance, let us assume that a gold producer wants to sell gold three month from today, say on 15th June. As he is exposed to lower price risk over the next three months, let us assume that he is looking to sell July gold futures, which is quoting at ₹32,000 today. Let us also assume that the spot price of gold today is ₹32,050. As we can see, there is a positive basis of ₹50. The producer is essentially seeking to establish a hedge of ₹32,050. If the basis strengthens over the next three months, say from ₹50to ₹75, the effective net selling price would increase to ₹32,075from ₹32,050, thereby benefiting the producer who was able to fetch a higher price for his produce.

An unexpected weakening of the basis, on the other hand, hurts the seller of a commodity. This is because the underperformance of the spot price relative to the futures price causes the seller to realize a lower selling price from the local spot market. For instance, let us consider the same example above with just one change - the basis weakens over the next three months, say from ₹50to ₹25. In this case, the effective net selling price would decrease to ₹32,025from ₹32,050, thereby hurting the producer who realized a lower price for his produce.

Weakening of basis

As already stated, the basis is said to weaken when the spot price of a commodity is underperforming the futures price. This can occur in any of the following manner:

-

Both the spot price and the futures price are increasing, but the futures price is increasing faster than the spot price

-

Both the spot price and the futures price are decreasing, but the futures price is decreasing slower than the spot price

-

The futures price is unchanged, while the spot price has decreased

-

The futures price has increased, while the spot price has decreased

-

The futures price has increased, while the spot price is unchanged

An unexpected weakening of the basis benefits the buyer of a commodity, such as a commodity consumer. This is because the underperformance of the spot price relative to the futures price enables the buyer to buya commodity at alower price from the local spot market. For instance, let us assume that a gold consumer wants to buy gold three month from today, say on 15th June. As he is exposed to higher price risk over the next three months, let us assume that he is looking to buy July gold futures, which is quoting at ₹32,000 today. Let us also assume that the spot price of gold today is ₹32,050. As we can see, there is a positive basis of ₹50. The consumer is essentially seeking to establish a hedge of ₹32,050. If the basis weakens over the next three months, say from ₹50 to ₹25, the effective net purchasing price would decrease to ₹32,025 from ₹32,050, thereby benefiting the consumer who was able to buyat a lower price.

On the other hand, an unexpected strengthening of the basis hurts the buyer of a commodity. This is because the outperformance of the spot price relative to the futures price causes the buyer to buy at a higher price from the local spot market. As an example, let us consider the same example above with just one change - the basis strengthens over the next three months, say from ₹50 to ₹75. In this case, the effective net buying price would increase to ₹32,075 from ₹32,050, thereby hurting the consumer who had to buy gold at a higher price.

Basis risk

In the examples presented above, the producer and the consumer faced uncertainty in terms of what the basis would be in the future. This uncertainty is nothing but the basis risk. The basis risk could either benefit or hurt the hedger, depending on how the basis has changed over time. As already stated above, an unexpected strengthening of the basis benefits the short hedger and hurts the long hedger; whereas an unexpected weakening of the basis benefits the long hedger and hurts the short hedger.

Cost of carry

In commodities parlance, the cost of carry refers to the cost of financing, transporting, storing, and insuring commodities. As the name suggests, cost of carry is the cost of carrying a commodity from the time a position is builttill the maturity of the contract.The cost of carry can be calculated as:

Cost of carry = (forward price/spot price)–1

If the RHS of the above equation is multiplied by 100, we get cost of carry in percentage terms. So, if the 3-month forward price of a commodity is $101 and the spot price is $100, the cost of carry works out to 1%. This means the cost of financing, transporting, storing, and insuring the commodity over a 3-month horizon is 1%.

Futures price is arrived at by adding cost of carry to the spot price of the commodity. This is because there is always a trade-off between selling the commodity today versus storing the commodity today and selling it in future. If the holder of the commodity decides to store the commodity today and sell it in the future, he will have to incur additional costs such as storing costs, insurance costs etc. Also, the holder will have to forego the opportunity cost of selling the commodity today and investing the proceeds from it in interest-bearing assets. As such, all these opportunity costs, which are nothing but the cost of carry, are added to the spot price of the commodity to arrive at the futures price. In other words,

Futures price = spot price + cost of carry

Cost of carry can be positive or negative. If the cost of carry is positive, it gives rise to a situation that is known as contango. If it is negative, it gives rise to a situation that is known as backwardation. It is common to believe that cost of carry would be positive given the opportunity costs that arise when holding a commodity in the future. However, this need not always be the case. On occasions, cost of carry can also be negative. It must be kept in mind that these opportunity costs are just one factor that determine the futures price. The other factor that has a significant bearing on the cost of carry is the prevailing demand and supply situation for a commodity.

A positive cost of carry would occur in case of commodities that experience a period of weak demand or excess supply or a combination of both. Such a situationcauses inventories to pile upand thereby putsmore downward pressure on short-term prices (or spot price) than on long-term prices (or futures price). Also, the piling up of inventories would increase storage and other costs, which would then be passed on to the buyer when the commodity is sold ata future date.

On the other hand, a negative cost of carry would occur in case of commodities that experience (or could experience) a period of strong demand or weak supply or a combination of both. This in turn causes inventories to drain and thereby lifts short-term prices (or spot price) more than long-term prices (or futures price). Also, given a situation of strong demand or weak supply, buyers would prefer buying commodities today rather than at a future date, in turn causing spot or nearby prices to become more expensive than distant prices.

Contango

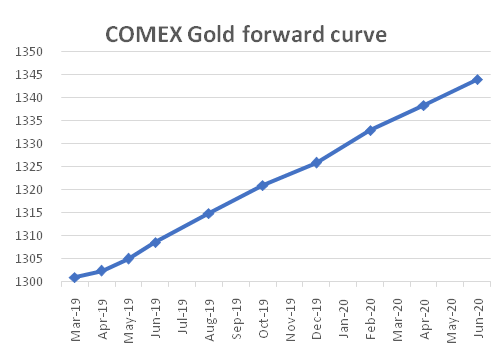

Earlier, we talked about basis and defined it as spot price of a commodity in the local market minus the futures price of that commodity. We saw that this difference could be either positive or negative. If this difference is negative, we have a situation that is known as contango. Contango occurs when the spot price of a commodity is below its futures price. Alternatively, a commodity is also in contango when prices in distant delivery months are higher than those in nearby delivery months. When a commodity is in contango, the shape of the commodity forward curve is normal i.e. upward sloping to the right.

In simplest terms, when a commodity is in contango, it gives clues to market participants about the current demand and supply situation of that commodity. Generally, contango indicates near-term supplies outstrip farther-term supplies, thereby causing nearby prices to trade at a discount to farther prices. Contango could also occur because traders are unwilling to pay a higher price for the commodity today due to an unfavourable cost of carry. When a commodity is in contango, it can benefit a trader who is short the commodity, even without much of a change in the spot price. This is because as each contract is trading at a higher price than its predecessor, a trader who is short the commodity would be able to roll over to the next contract at ahigher price. In other words, he would be able to keep on re-entering the trade by shorting the commodity at higher prices, thus benefiting him. On the other hand, contango would hurt a trader who is long the commodity and intends to roll-over. This is because in order to roll over to the next contract, he will have to enter the trade at a higher price i.e. re-enter the trade by going long the commodity at a higher price.Simply put, contango creates a positive roll yield to a trader who is short the commodity, and a negative roll yield to a trader who is long the commodity.

| Month | Last Price |

| Mar-19 | $1,300.9 |

| Apr-19 | $1,302.3 |

| May-19 | $1,304.9 |

| Jun-19 | $1,308.5 |

| Aug-19 | $1,314.8 |

| Oct-19 | $1,320.9 |

| Dec-19 | $1,325.8 |

| Feb-20 | $1,332.9 |

| Apr-20 | $1,338.3 |

| Jun-20 | $1,344.0 |

Backwardation

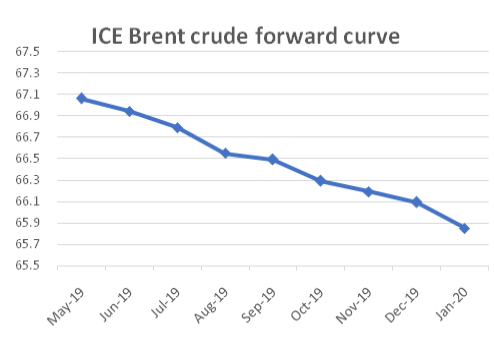

Backwardation is the opposite of contango i.e. it is a condition wherein the basis is positive. Backwardation occurs when the spot price of a commodity is trading at a premium to the futures price. Alternatively, a commodity is also in backwardation when prices in distant delivery months are lower than those in nearby delivery months. When a commodity is in backwardation, the shape of the commodity forward curve is inverted i.e. it is downward sloping to the right.

Backwardation indicates supply tightness, which could be due to factors such as geopolitical events (common in case of crude oil) and weather disruption (common in case of agricultural commodities). When a commodity is in backwardation, it can benefit a trader who is long the commodity, even without much of a change in the spot price. This is because as each contract is trading at a lower price than its predecessor, a trader who is long the commodity would be able to roll over to the next contract at a lower price. In other words, he would be able to re-enter the trade by buying the commodity at a lower price, thus benefiting him. On the other hand, backwardation would hurt a trader who is short the commodity and intends to roll-over. This is because in order to roll over to the next contract, he will have to enter the trade at a lower price i.e. re-enter the trade by going short the commodity at a lower price.Simply put, backwardation creates a positive roll yield to a trader who is long the commodity, and a negative roll yield to a trader who is short the commodity.

| Month | Last Price |

| May-19 | $67.06 |

| Jun-19 | $66.94 |

| Jul-19 | $66.79 |

| Aug-19 | $66.55 |

| Sep-19 | $66.49 |

| Oct-19 | $66.29 |

| Nov-19 | $66.19 |

| Dec-19 | $66.09 |

| Jan-20 | $65.85 |

We can see from the table above that each contract is quoting at a lower price than that of its predecessor, suggesting that the commodity is in backwardation. The graph on the right shows the forward curve for ICE Brent crude oilfutures. Observe how the graph is downward sloping to the right, indicating backwardation.

Summary

-

Basis refers to the difference between spot price of a commodity and its futures price i.e. Basis = spot price of a commodity in the local market – the futures price of that commodity

-

Basis can be positive or negative. Basis is positive when spot price is above the futures price, and negative when spot price is below futures price.

-

Basic is affected by factors such as: Local demand and supply conditions, quality and other aspects of the commodity, storage and insurance costs, and transportation costs etc.

-

Basis is said to strengthen when the spot price of a commodity is outperforming the futures price.

-

An unexpected strengthening of the basis from time benefits the seller of a commodity, such as a commodity producer. This is because the outperformance of the spot price relative to the futures price enables the seller to fetch a higher selling price from the local spot market.

-

Basis is said to weaken when the spot price of a commodity is underperforming the futures price.

-

An unexpected weakening of the basis benefits the buyer of a commodity, such as a commodity consumer. This is because the underperformance of the spot price relative to the futures price enables the buyer to buy a commodity at a lower price from the local spot market.

-

Cost of carry refers to the cost of financing, transporting, storing, and insuring commodities. As the name suggests, cost of carry is the cost of carrying a commodity from the time a position is built till the maturity of the contract.

-

Contango occurs when the spot price of a commodity is below its futures price. Alternatively, a commodity is also in contango when prices in distant delivery months are higher than those in nearby delivery months.

-

When a commodity is in contango, the shape of the commodity forward curve is normal i.e. upward sloping to the right.

-

When a commodity is in contango, it gives clues to market participants about the current demand and supply situation of that commodity. Generally, contango indicates near-term supplies outstrip farther-term supplies, thereby causing nearby prices to trade at a discount to farther prices.

-

Backwardation occurs when the spot price of a commodity is trading at a premium to the futures price. Alternatively, a commodity is also in backwardation when prices in distant delivery months are lower than those in nearby delivery months.

-

When a commodity is in backwardation, the shape of the commodity forward curve is inverted i.e. it is downward sloping to the right.

-

Backwardation indicates supply tightness, which could be due to factors such as geopolitical events (common in case of crude oil) and weather disruption (common in case of agricultural commodities).

Next Chapter

Comments & Discussions in

FYERS Community

vijay commented on May 23rd, 2019 at 12:55 AM

As explained here the spot price commodity is very important in determining the price of commodity. Where we can get the spot price of the commodities like crude oil and zinc..

tejas commented on May 23rd, 2019 at 2:03 PM

Hey Vijay, The exchanges don't provide spot prices of commodities. The best proxy is the near month continuous futures chart which is available by default on Fyers Web on all commodity contracts.

kailash commented on May 30th, 2019 at 6:48 PM

Can you explain briefly if commodity markets are in contango,so will the roll yield on commodity indices be negative or postive?

tejas commented on May 31st, 2019 at 1:23 PM

Kailash, In contango the futures price is higher than the spot price. Hence, if you are long the roll yield will be negative as you have to square off your near-month position at a lower price and re-enter the next month contract at a higher price.

Whereas if you are short, the roll yield will be positive because you get to short at a higher price as the futures price in contango is higher than the spot price and previous month futures price.

Rohit surve commented on July 3rd, 2019 at 11:01 PM

If contango happens can we short the commodities for a period of 3 to 4 days basically, will it affects the commodities trend for a short time.

Jagadish Kumar commented on July 4th, 2019 at 11:00 PM

How the cost of carry can be negative. Because if we are holding the commodity there will be transporting and storing cost.