Introduction

So far, we have talked about commodities from a derivative perspective by covering instruments such as commodity spot, forwards, futures, and options. We have also spoken about types of participants in the commodities market, types of commodities, Indian commodity exchanges, contract specifications of commodities on Indian exchanges, commodity basis etc.

In this chapter, we shall now be focusing on the fundamentals of commodities. We will talk about the key factors that drive the commodities on the demand and supply side. We will also be discussing about some of the key macro-economic events that have a bearing on commodity prices. The commodities that we would be focusing on are precious metals (gold and silver), energy complex (crude oil and natural gas), and base metals (copper, aluminium, zinc, lead, and nickel).

Precious metals

Precious metals have been given their name because of the rarity of these metals on our planet and because of the high price that they fetch. These metals have been with us dating back to thousands of years and have been considered sacred and highly valuable ever since they were first discovered by mankind. Not only do these metals have industrial uses, but they are also heavily used as investment vehicles. In some countries, such as India and China, these metals have gained even more prominence among people and are considered as an excellent store of value.

In India, the two precious metals that are widely traded are gold and silver. We shall now focus on each of them in more detail.

Gold

Gold is the most widely traded precious metal around the world. History suggests that gold was first smelted sometime around 3600 B.C. by the Egyptians. Since then, the role of the metal has evolved into various forms. That said, despite the passing of several centuries, one factor that has remained constant is that gold has retained its tag as a store of value. The metal is not just a commodity, but also a currency. In fact, before the advent of paper currency, gold was a primary currency in several countries. Today, gold is used not only as a jewellery, but also in industries and as an investment vehicle. Gold is also the only commodity that central banks buy and store in the form of official reserves, given the limited availability of the metal, its role as a store of value, its hedge against tail risks, and its use as a valuable collateral. Gold is a highly liquid commodity as it is widely traded across the world in several commodity exchanges. In India, the exchange that dominates volumes for gold derivatives is MCX.

Gold demand

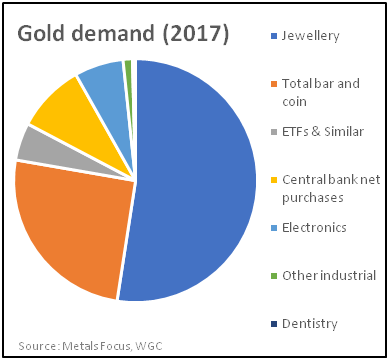

Demand for gold comes from various sectors. The chart shows global demand for gold in the year 2017.

As can be seen, the largest share on the demand side comes from the jewellery sector – just over a half of gold’s overall demand. Given the cultural affinity for gold, a significant portion of the metal’s jewellery demand comes from Asia, primarily from China and India, who combined account for almost three-fifths of the global jewellery demand. The jewellery demand is more sensitive to the price of gold. It tends to increase during times when gold prices are falling and decrease during times when gold prices are rising.

As can be seen, the largest share on the demand side comes from the jewellery sector – just over a half of gold’s overall demand. Given the cultural affinity for gold, a significant portion of the metal’s jewellery demand comes from Asia, primarily from China and India, who combined account for almost three-fifths of the global jewellery demand. The jewellery demand is more sensitive to the price of gold. It tends to increase during times when gold prices are falling and decrease during times when gold prices are rising.

The second major category of gold demand is investment demand for the metal, which includes bars & coins and ETFs & similar products. Combined, theyaccount for three-tenths of gold’s overall demand. Unlike jewellery demand which is price sensitive, investment demand is not as price sensitive, especially in the western countries. Instead, investment demand is largely driven by macro-economic factors around the globe. Investment demand tends to increase during times of uncertainties & economic hardship and decrease during times of economic strength & an appetite for riskier assets.

The third major source of gold demand is central bank buying, contributing to just around a tenth of gold’s demand. This side of gold’s demand has been gaining a lot of prominence since the last two decades. The 2008 global financial crisis lead to a devaluation of several currencies around the world, in turn causing central banks to increase their purchases of gold. Their buying of gold during difficult financial times has further highlighted the importance of gold as a hedge against currency devaluation and global macro-economic risks.

The final source of gold demand comes from the industrial side. This includes demand from the electronics sector, dentistry sector, and other industrial sectors. Combined, they account for less than 10% of gold’s demand.

Gold supply

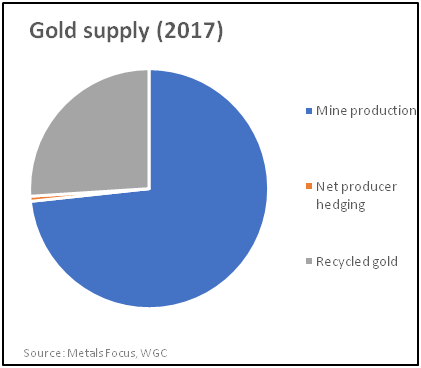

There are three major sources of gold supply: mine production, recycled gold, and producer hedging/de-hedging.

Mine production, which is also known as primary supply, accounts for nearly three-fourth of gold’s overall supply. Mine production is less sensitive to gold price fluctuations. This is because it takes a significant amount of time, possibly even decades, to discover a mine and then bring that mine into operation. As such, the reaction to gold price changes is only gradual i.e. it could take a few years of sustained movement in the price of gold for it to have an impact on mine output. China is the largest gold producing nation in the world, contributing to around 13% of global output, followed by Australia and Russia, who account for around 9% of world production.

Recycled gold, which is also known as secondary or scrap supply, is the recycling of gold that has already been mined previously and is now above the earth’s surface. Over 90% of recycled gold comes from jewellery while the rest comes from industrial and other sources. Recycled gold accounts for around a fourth of gold’s supply. Unlike mine production which is less sensitive to gold price fluctuations, recycled gold responds quickly to changes in the price of the yellow metal. Recycling tends to rise during times of high gold price and tends to fall during times of low gold price.

Net producer hedging, which refers to selling future gold output using derivative instruments to lock in a price today, is the third component of gold supply. This component can be either positive or negative. A positive figure indicates gold producers are hedging their future production, primarily to safeguard against declining gold prices. A negative figure suggests that gold producers are unwinding their forward sales, mostly in reaction to rising gold prices. In 2017 net producer hedging occupied a negative share in overall gold supply, as miners unwound their hedges in reaction to rising gold prices. As can be seen, this component of gold supply is sensitive to changes in gold price. Hedging from miners tends to increase during periods of sustained price decline and decrease during periods of sustained price rally. As already seen in an earlier chapter, hedging has both benefits and drawbacks. The benefit is that it prevents miners from incurring losses in case of price decline. The drawback is that this benefit comes at a cost, which is that hedging prevents miners from gaining in case of price rally.

Factors that influence gold price

Gold is a unique asset in that it is partly a commodity and partly a currency. While gold is not an official means of payment, it nonetheless has retained its role as a store of value. Gold has a history of gaining in value during times of economic crisis or when people lose their faith in paper currencies. Even during the most recent financial turmoil, the 2008 subprime crisis, gold price initially declined along with other assets, but then nearly tripled in value over the next few years as central banks around the world embarked on a path of ultra-low interest rates in order to stimulate their economies. The devaluation in currencies during this period and uncertainties about the health of the global economy triggered massive inflows into gold.Unlike most commodities that are heavily influenced by the traditional demand-supply factors, gold price is also impacted by factors beyond these. For instance, gold price is heavily influenced by market sentiment and risk flows prevailing across the globe, currency movement, inflation expectation, central bank policy actions etc. We shall now talk about the key factors that impact the price of gold.

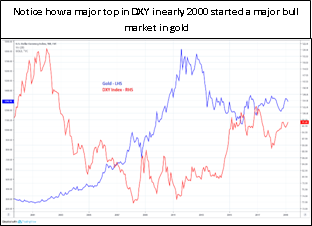

The US dollar

One of the major factors that determine the direction of gold is the US dollar. While short-term correlations may sometimes fluctuate from time to time, the long-term relation between the two has remained remarkably stable. The two share a strong negative correlation between them. A rally in the dollar causes gold price to head south, while a decline in the dollar causes gold price to head north. One of the reasons why this happens is because gold is priced in US dollar terms. A strengthening of the US dollarviz a viz other currencies makes it more expensive to buy gold to holders of other currencies, thereby reducing demand for the metal. Similarly, a weakening US dollar makes it attractive for holders of other currencies to buy gold, thereby stimulatingdemand for it.

Monetary policy

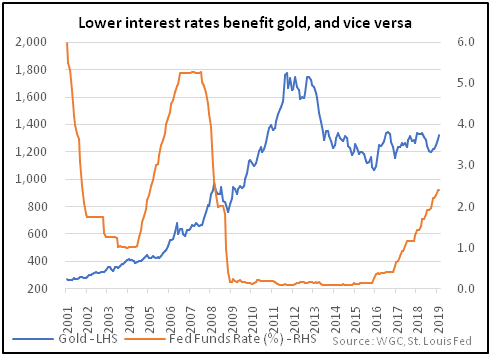

Gold is impacted by the actions of central banks around the world. One of the objectives of a central bank is to control inflationary pressuresin an economy. To achieve this objective, central banks use monetary policy, which is the primary tool at their disposal to influence money supply in an economy and ensure price stability.

At times when inflationary pressures are mounting and start doing more harm to the economy than good, central banks adopt a tight monetary policy, wherein they reduce money supply by raising short-term interest rates. Unlike equities and bonds, gold is a non-yielding asset as it does not yield a periodic cash flow. As such, rising interest rates increase the allure for other competing assets such as bonds. Also, as interest rates go up, so does the value of the local currency. So, any rate increases in the US tends to lift the US dollar as well. And as we know by now, rising dollar is negative for gold prices. As a result of all these, a tightening monetary policy tends to reduce the appetite for buying gold and thereby puts downward pressure on gold prices.

The opposite is also true in case of an accommodative monetary policy, wherein central banks increase money supply by lowering short-term interest rates in order to revive economic conditions. Such an environment underpins gold price.

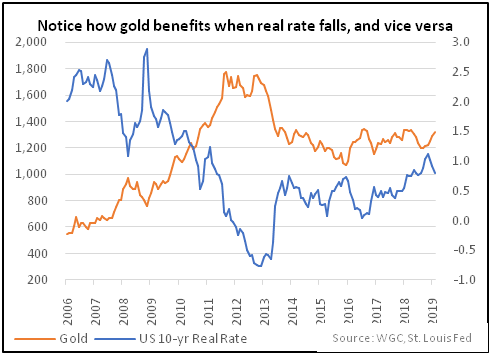

Real rate of return

Historically, gold has been used by investors as a hedge against inflation, gaining in value during periods of a sustained build-up in price pressures, and vice versa. This is more so the case when inflation reaches a point wherein it makes the real rate of return (which is nominal rate of return minus the expected inflation) negative.

Let’s talk about this in a little more detail with a simple example.

Nominal rate of returnis the stated rate, i.e. it is the rate stated in financial instruments such as bank loans, fixed deposits, provident fund etc. It does not include the element of inflation in it. If the nominal rate of return is 7% and inflation is 5%, the real return is 2%. This means after taking inflation into consideration, the investor would earn a 2% return. However, if nominal rate of return stays constant at 7% and if inflation rises to, say, 8%, the real rate of return is now -1%. This means after considering inflation, the investor would end up losing 1%.

As already stated, one of the reasons why gold tends to underperform during periods of rising interest rates is because the opportunity cost of holding the metal goes up. After taking inflation into account, if the real rate is positive and heading higher, investors prefer investing in interest-bearing assets that yield periodic cash flows. However, if the real rate is negative and falling, investors would end up losing money after taking into consideration the effects of inflation. Unlike paper assets, gold is a physical asset that is extremely scarce in supply. Hence, demand for the metal shoots up when real rates become negative and starts to fade when real rates become positive.

As such, it’s worth keeping an eye on the direction in which real rates are headed rather than focusing on just the nominal rates or inflation. One way to track the real rate is to monitor the difference between 10-year US treasury yield and 10-year US breakeven inflation rate (data for both isavailable on the Federal Reserve’s website) and then look at the direction in which this spread is heading.

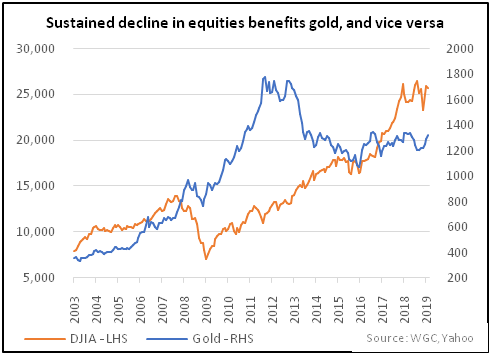

Risk appetite

As we already know by now, gold is often considered a hedge against tail risks. The yellow metal tends to gain in value when macro-economic conditions are deteriorating. This is because during times of financial and economic stress as well as during times of geopolitical tensions, investors tend to dump riskier assets, such as equities, in favour of safer ones. As gold is not a paper asset but rather a head asset that is scarce in supply, there is little to no risk of it becoming worthless. As such, demand for the metal shoots up during times of rising tail risks, macro-economic headwinds, and geopolitical uncertainties. On the other hand, when economic conditions are strengthening and tail risks are receding, the opportunity cost of holding gold increases, thereby lowering demand for it as investors shift from safe havens to riskier assets in search of higher yield.

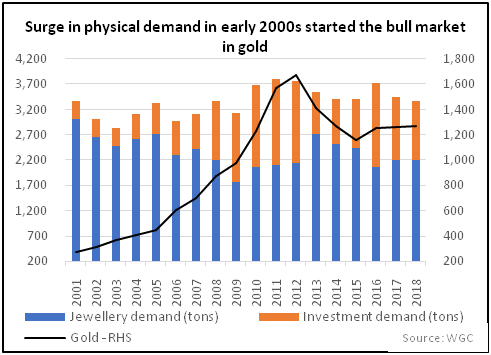

Physical demand

As we saw earlier, over half of gold’s demand comes from jewellery, within which a bulk of the global share is occupied by China and India. Unlike the western countries where investors mostly perceive gold as a portfolio diversifier & a hedge against macro risks, consumers in the eastern countries have a greater sentimental and cultural attraction towards gold. As such, in the east, demand for gold also tends to pick up during prosperous times when household incomes are rising. It’s not surprising that the gold bull market which lasted from 2000 to 2011 came on the back of not only a strong investment demand from the west but also a robust physical demand from the east. While short and medium-term prices tend to be influenced by investment flows, longer-term prices tend to be impacted by how strong physical demand for gold is.

How to trade gold

As we know by now, gold price tends to be impacted by a lot of factors other than the traditional demand-supply factors that impact prices of other commodities in general. In order to trade gold:

-

One must closely watch how the real rates and the US dollar are moving.

-

One must watch the risk appetite prevailing in the markets, by keeping an eye on global indices such as the S&P 500 and CBOE volatility index.

-

Also, as gold is priced in US dollars, understanding the health of the US economy is of utmost importance, given the impact it has on the US monetary policy and subsequently on other asset classes.

-

Some of the key US economic reports that must be focused on are the nonfarm payrolls and unemployment rate, GDP, consumer and producer inflation, manufacturing and non-manufacturing PMI, trade balance, retail sales, and consumer confidence.

-

Once in a quarter when the World Gold Council (WGC) releases its demand-supply update, one must also monitor the jewellery demand for gold, especially in the east.

Next Chapter

Comments & Discussions in

FYERS Community

saloni commented on June 4th, 2019 at 6:56 PM

Which is the best way to trade in gold, direct ownership, gold mutual funds or gold option and futures?

tejas commented on June 5th, 2019 at 11:19 PM

Trading in physical bullion is expensive and inefficient. Gold MFs/ETFs are alright for the long term and options are kinda illiquid at the moment. the best way is to trade in gold futures. There are various contract sizes which can suit you needs. If your capital size is small, consider trading in Gold Mini.

All the best.

Manish commented on June 24th, 2019 at 11:15 PM

How the dollar affects the Gold, Because US is not the major Producer of the gold nor the US is a major importer of the gold.

tejas commented on July 1st, 2019 at 7:43 PM

US Dollar affects all those commodities which are priced in US dollars mostly because it is the world's most widely used and powerful currency.

Mayank K S commented on June 24th, 2019 at 11:31 PM

In MCX Gold majorly trades happens from the hedgers or speculators.

tejas commented on July 1st, 2019 at 7:44 PM

Speculators! Hedgers don't transact very often.

Vinayak Joshi commented on July 15th, 2019 at 11:08 PM

Can we take short position in Gold Mini and close it before 1st of expiry, as same as NIFTY or there any difference in MCX.

tejas commented on August 14th, 2019 at 5:08 PM

Hi Vinayak, You can do that. Just make sure to keep track of expiry dates. You don't want that to interfere with your trade. If either contract is expiring earlier, you can rollover to the next contract.