25 Jul, 2025

25 Jul, 2025

5 mins read

5 mins read

When it comes to low-risk and stable investment options, fixed deposits (FDs) remain a favourite among Indian investors. They offer guaranteed returns, flexible tenures, and a simple investment structure that appeals to both new and seasoned savers. But beyond the basics, what is a fixed deposit, and why does it continue to be such a reliable tool for wealth preservation?

Let’s explore the concept of fixed deposits, how they work, the different types available in India, and the benefits they offer in 2025.

A fixed deposit is a financial instrument provided by banks and non-banking financial companies (NBFCs) where you deposit a lump sum of money for a fixed tenure at a pre-agreed interest rate. At the end of the term, you receive your principal amount along with the earned interest.

Unlike a savings account, a fixed deposit account does not allow regular withdrawals. Instead, the money is locked in until maturity, which helps you earn better returns than traditional savings options.

In simple terms, it’s a safe, time-bound investment that earns predictable interest, making it ideal for conservative investors.

Here’s a quick look at how FDs function:

Deposit Amount: You deposit a specific amount with a bank or NBFC.

Fixed Tenure: Choose a tenure ranging from 7 days to 10 years.

Interest Rate: The institution offers a fixed interest rate for that period.

Interest Payout: You may opt for monthly, quarterly, or cumulative (on maturity) interest.

Maturity: At the end of the term, you receive your original amount plus interest earned.

Some banks allow premature withdrawal, but this may reduce your returns due to penalties or adjusted rates.

When exploring FDs, you’ll come across several variants catering to different financial goals:

The standard FD with fixed tenure and interest rate.

Has a 5-year lock-in period and is eligible for tax deductions under Section 80C of the Income Tax Act.

Offered with higher interest rates for individuals aged 60 and above.

Cumulative: Interest is compounded and paid at maturity.

Non-Cumulative: Interest is paid monthly or quarterly.

Links your FD to your savings account, allowing automatic transfers above a certain limit to be invested as FDs.

Each of these types of fixed deposits offers flexibility based on your liquidity needs, tax planning, and income preferences.

Here’s why FDs continue to be a reliable part of most financial plans:

Your principal is protected, making FDs one of the safest investment instruments.

Unlike market-linked options, FD returns are fixed and not affected by market volatility.

You can choose your tenure and payout frequency, making it suitable for both short-term goals and long-term savings.

Opening an FD is quick and available online and offline through banks, NBFCs, or digital platforms.

You can get a loan of up to 90% of your FD value without breaking the deposit.

Additional interest (0.25% to 0.75%) is offered to seniors, providing better income security.

While FD rates fluctuate, many banks are offering attractive interest rates in 2025 to encourage deposits amidst global uncertainty. Here’s an approximate rate comparison:

| Bank Name | Regular FD Rate (1–3 Years) | Senior Citizen Rate |

|---|---|---|

| SBI | 6.5% – 7.0% | 7.0% – 7.5% |

| HDFC Bank | 7.0% – 7.25% | 7.75% – 8.0% |

| ICICI Bank | 6.9% – 7.2% | 7.4% – 7.75% |

| Axis Bank | 7.0% – 7.1% | 7.5% – 7.6% |

| Bajaj Finance FD | 7.5% – 8.05% | 8.2% – 8.3% |

Note: Rates vary by deposit amount and tenure. Check with your bank or NBFC for exact figures.

Senior citizens enjoy higher FD rates, typically between 0.25% to 0.75% more than the standard rate. This boost in earnings helps retirees secure steady interest income without taking market risks.

Additionally:

Many banks offer special senior citizen schemes with flexible tenures.

Interest earned up to ₹50,000 annually is tax-free under Section 80TTB.

FDs remain one of the most trusted income sources for senior citizens, especially when market-linked investments may feel too risky.

Before starting a fixed deposit, keep these in mind:

Compare interest rates across banks and NBFCs.

Check penalty clauses for premature withdrawal.

Understand the difference between cumulative and non-cumulative options.

Choose tenure wisely to match your financial goals.

Evaluate tax implications, especially if you're in a higher tax bracket.

Also, remember that while FDs are low-risk, their post-tax returns may sometimes lag behind inflation, so diversify accordingly.

To summarise, a fixed deposit is a time-tested, safe, and dependable investment tool that offers steady returns and peace of mind. Whether you're building an emergency fund, planning for retirement, or simply parking excess funds, FDs offer unmatched convenience and stability.

By understanding the types of fixed deposits, their benefits, and the latest bank FD rates, you can make more informed and goal-oriented financial decisions in 2025.

A fixed deposit is a financial product where you invest a lump sum for a fixed period and earn interest at a guaranteed rate.

Yes, but premature withdrawal may result in reduced interest or penalty, depending on your bank’s policy.

Common types include regular FD, tax-saving FD, senior citizen FD, flexi FD, and cumulative/non-cumulative FDs.

In 2025, senior citizens can earn around 7.5% to 8.3%, depending on the institution and deposit tenure.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

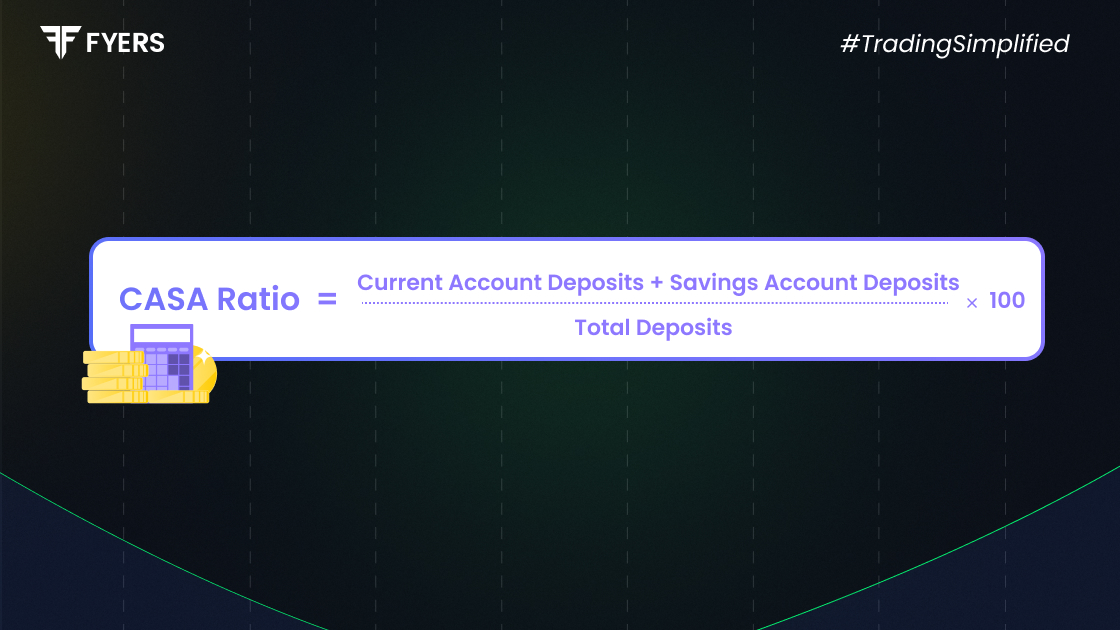

The CASA ratio has long been a key metric for…

23 Jul, 2025

4 mins read

You have successfully submitted your partnership request form. You will be hearing us soon!