29 Sep, 2025

29 Sep, 2025

5 mins read

5 mins read

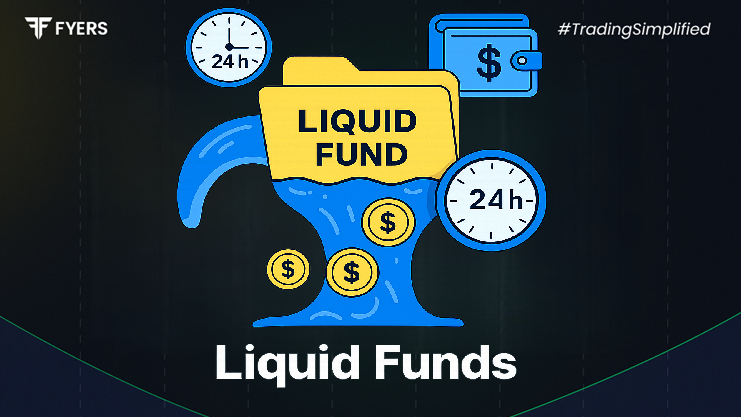

Investors seeking safe, short-term investment options often explore liquidity funds, also referred to as short-term debt funds or money market mutual funds. These funds provide high liquidity, low risk, and relatively stable returns, making them a popular alternative to traditional bank deposits.

Liquid funds are a type of debt mutual fund that invests primarily in highly liquid money market instruments. These include treasury bills, commercial papers, and certificates of deposit, typically with a maturity of up to 91 days. Unlike equity funds, these funds are not exposed to stock market volatility, making them ideal for parking surplus cash for short durations.

In essence, cash management mutual funds aim to provide investors with both safety of principal and easy access to funds, often within a day or two.

High Liquidity: The most prominent feature of high-liquidity mutual funds is the ability to redeem investments quickly, usually within 24 hours. This makes them suitable for emergency funds or short-term cash needs.

Short-Term Investment Horizon: These funds are designed for investors looking to invest from a few days to a few months. They are not intended for long-term wealth creation.

Low Risk Profile: Since liquid funds invest in instruments with short maturities and high credit quality, they carry minimal credit and interest rate risk compared to longer-term debt funds.

Stable Returns: While returns are modest compared to equity funds, they are generally more predictable, making them an attractive choice for risk-averse investors.

Professional Management: Like other mutual funds, liquid mutual funds are managed by professional fund managers who monitor market conditions to optimize returns while maintaining liquidity.

Better than Savings Accounts: Historically, liquidity funds provide returns slightly higher than traditional savings accounts, while still maintaining capital safety.

Ease of Access: Investors can redeem money at any time without penalties, making short-term debt funds a convenient parking option.

Low Minimum Investment: Many liquidity funds allow investors to start with relatively small amounts, often as low as ₹500, making them accessible to retail investors.

Diversification of Cash Holdings: Instead of keeping surplus cash idle in a savings account, investors can earn incremental returns by allocating funds to cash management mutual funds.

Flexibility for Corporates and Individuals: Both corporate treasuries and individual investors can benefit from the short-term nature of these funds to manage liquidity efficiently.

Returns from liquidity funds are influenced by prevailing interest rates in the money market. Typically, these funds generate annualized returns in the range of 3–6%, depending on market conditions and fund performance. Unlike fixed deposits, returns fluctuate slightly based on changes in short-term interest rates, providing a more market-linked yield.

Investors should note that while returns are modest, the primary goal of money market mutual funds is to preserve capital while offering liquidity, rather than generating high gains.

Interest rates on underlying instruments, such as commercial papers and treasury bills, directly affect the yield of high-liquidity mutual funds. When the Reserve Bank of India (RBI) raises policy rates, short-term instruments tend to offer higher returns, which reflects in the fund’s performance. Conversely, declining rates may reduce yield but generally do not impact the principal invested.

Short-term debt funds, including liquidity funds, are taxed differently depending on the holding period:

Less than 36 months: Gains are treated as short-term capital gains and taxed according to the investor’s income tax slab.

More than 36 months: Gains qualify as long-term capital gains and are taxed at 20% with indexation benefits.

Interest income from these funds is distributed in the form of dividends if opted, which may be subject to dividend distribution tax.

Investors should consult tax professionals to understand the implications based on individual financial situations.

Retail Investors: Individuals seeking a safe parking option for short-term goals, emergency funds, or idle cash can benefit from liquidity funds.

Corporate Treasuries: Companies often use cash management mutual funds to optimise surplus cash while ensuring liquidity for operational needs.

Risk-Averse Investors: Those hesitant to expose capital to market volatility can rely on these funds for stable returns.

Savers Looking for Flexibility: Investors who require access to funds without locking them into fixed deposits can take advantage of the quick redemption feature.

Despite being low-risk, short-term debt funds are not entirely risk-free. Key limitations include:

Credit Risk: Although rare, if a fund invests in lower-rated commercial papers, there’s a small chance of default.

Interest Rate Fluctuations: Changes in short-term interest rates may slightly affect the returns, even though principal remains largely safe.

Not Ideal for Long-Term Wealth Creation: Investors seeking high capital appreciation over long periods should explore equity funds instead of high-liquidity mutual funds.

Returns May Be Lower Than Bank FDs in Some Cases: While generally competitive, liquid fund yields can be lower than fixed deposits during periods of high interest rates.

Liquid funds, also referred to as short-term debt funds or cash management mutual funds, provide an ideal blend of liquidity, safety, and modest returns. They serve as an effective alternative to idle cash in savings accounts and offer professional management of surplus funds.

While not a vehicle for long-term wealth creation, these funds are highly useful for risk-averse investors, corporates, and individuals looking for accessible, low-risk investment options. By understanding features, benefits, and taxation, investors can effectively integrate money market mutual funds into their short-term financial planning.

While extremely rare, slight negative returns can occur during market disruptions, especially if short-term interest rates fall sharply.

They often offer higher liquidity and marginally better returns, though fixed deposits provide guaranteed interest.

Most funds allow starting investments as low as ₹500.

Yes, their high liquidity makes them an ideal choice for parking emergency funds.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

In the world of mutual funds, debt schemes often attract…

29 Sep, 2025

4 mins read

You have successfully submitted your partnership request form. You will be hearing us soon!