17 Sep, 2025

17 Sep, 2025

3 mins read

3 mins read

When it comes to safe and reliable savings options, both fixed deposits (FDs) and term deposits (TDs) are popular among Indian investors. However, many people are often confused about the difference between term deposit and fixed deposit. While both options help in disciplined saving and guaranteed returns, their features and flexibility vary.

This blog explains the concept, benefits, and differences between term deposits and fixed deposits, so you can decide which suits your financial goals better.

A fixed deposit (FD) is a savings instrument offered by banks and financial institutions where you invest a lump sum for a fixed period at a predetermined interest rate.

Tenure: Ranges from a few days to several years.

Interest Rates: Locked at the time of investment and remain unaffected by market changes.

Withdrawal: Premature withdrawal is possible but may attract penalties.

FDs are popular for their safety, assured returns, and flexibility in tenure selection.

A term deposit is a broader category that includes both fixed deposits (FDs) and recurring deposits (RDs). In simple words, every FD is a term deposit, but not every term deposit is a fixed deposit.

Fixed Deposit: Lump sum invested for a fixed term.

Recurring Deposit: Monthly investments over a fixed period.

Tenure: Flexible, ranging from short-term to long-term.

Interest: Locked in for the tenure, just like in FDs.

Thus, term deposit is an umbrella term, while FD is a specific type under it.

|

Aspect |

Fixed Deposit (FD) |

Term Deposit (TD) |

|---|---|---|

|

Definition |

Lump sum deposited for a fixed term |

Broader category including FD and RD |

|

Investment Mode |

One-time lump sum |

Lump sum (FD) or monthly instalments (RD) |

|

Flexibility |

Only lump sum investment |

Choice between FD and RD |

|

Tenure |

Fixed period from days to years |

Depends on type (FD or RD) |

|

Returns |

Guaranteed fixed interest |

Guaranteed fixed interest |

So, while FDs are a type of term deposit, the key difference is that term deposit also includes recurring deposits.

Assured Returns: Guaranteed interest irrespective of market fluctuations.

Capital Safety: One of the safest investment options.

Flexible Tenure: Investors can choose duration as per financial goals.

Loan Against FD: Many banks offer loans against FD, ensuring liquidity.

Variety: Includes both FD and RD, catering to different saving styles.

Flexibility in Investment: You can invest either lump sum or through small monthly contributions.

Guaranteed Earnings: Just like FDs, term deposits assure fixed interest returns.

Discipline in Saving: RDs under term deposits encourage monthly saving habits.

Choosing between term deposit vs fixed deposit depends on your saving style and goals:

If you have a lump sum amount and want to earn guaranteed returns, an FD is the better choice.

If you prefer to save monthly in smaller amounts, a recurring deposit (RD) under term deposits may be more suitable.

Both options offer safety, stability, and fixed returns, making them excellent choices for risk-averse investors.

In summary:

FD = Lump sum term deposit

TD = FD + RD (broader category)

The confusion around term deposit vs fixed deposit often arises because an FD is essentially a type of term deposit. The main difference lies in flexibility—while an FD requires a lump sum investment, a term deposit can also mean recurring contributions.

If you want disciplined monthly savings, go for an RD under term deposits. If you have idle funds that you want to grow securely, choose a fixed deposit. Both options are safe and beneficial depending on your needs.

A fixed deposit is a type of term deposit where you invest a lump sum for a fixed period. Term deposit also includes recurring deposits (RDs).

Both are equally safe since they fall under the same product category offered by banks and NBFCs.

FDs offer fixed tenure, guaranteed returns, flexible investment terms, and the option of loans against deposits.

Yes, term deposits include both FD (lump sum) and RD (monthly deposits), so you can choose either or both.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

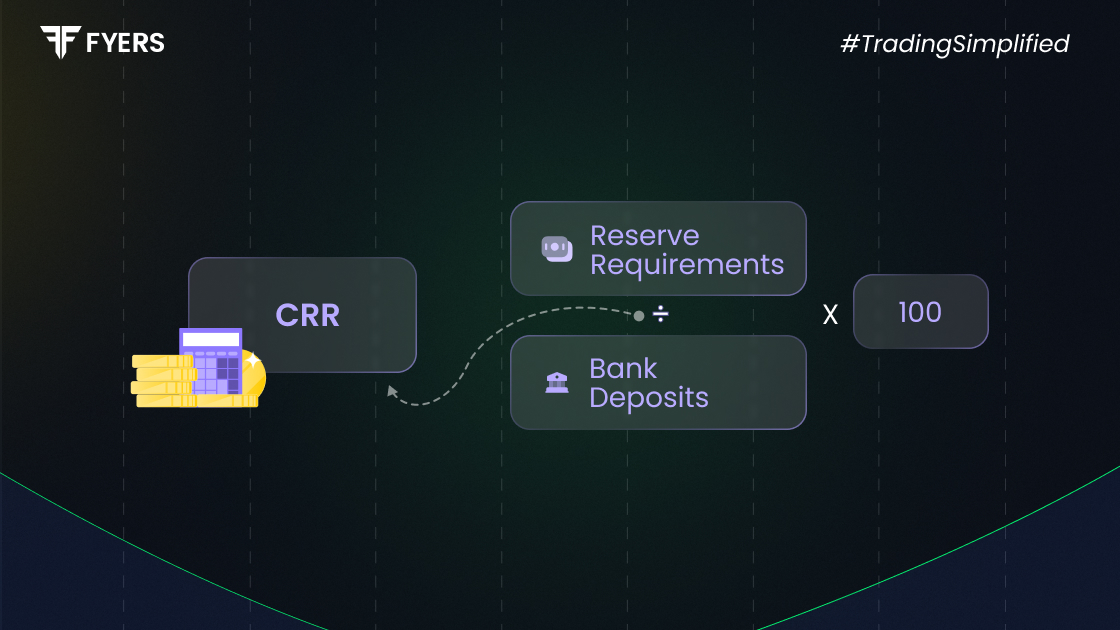

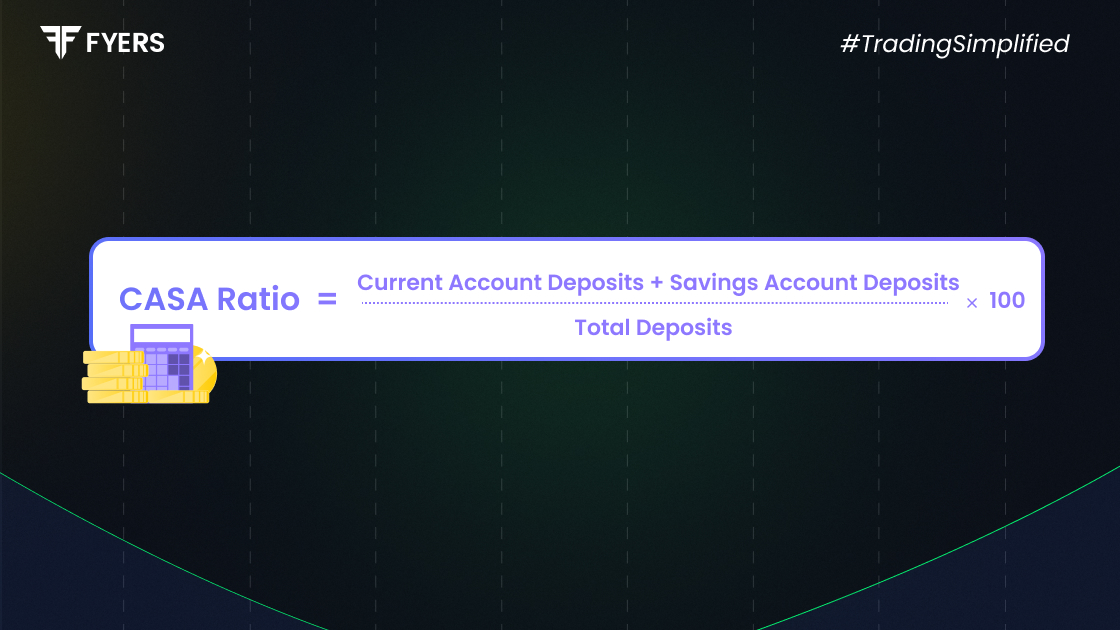

The CASA ratio has long been a key metric for…

23 Jul, 2025

4 mins read

You have successfully submitted your partnership request form. You will be hearing us soon!