29 Sep, 2025

29 Sep, 2025

5 mins read

5 mins read

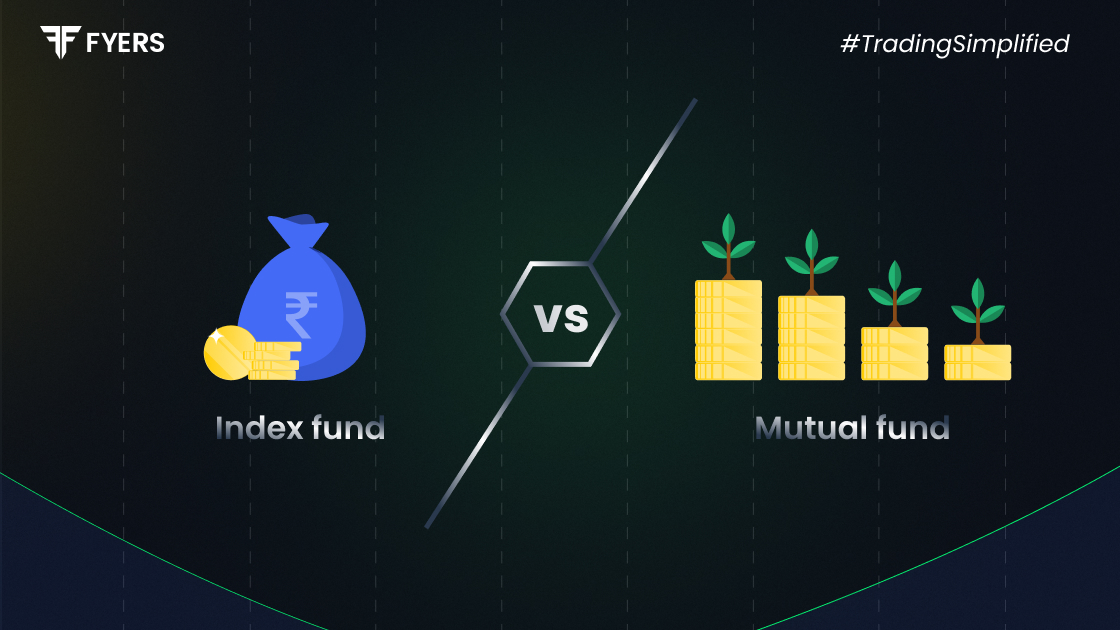

Investors often wonder which path to take when planning their financial journey: index fund vs mutual fund. Both are designed to grow wealth by pooling money from multiple investors, yet the way they operate, charge fees and deliver results differs. Choosing between them is not simply about chasing returns but about aligning with one’s goals, risk appetite, and investment style.

This guide explains how mutual funds and index funds work, where they differ, the updated tax implications under the new rules for FY 2025–26 and when one might be more suitable than the other.

Mutual funds are professionally managed investment schemes that pool money from investors and spread it across different financial instruments, such as shares, bonds, or money market tools. A fund manager actively makes buy and sell decisions with the objective of outperforming the market or achieving a particular goal such as growth, income, or capital preservation.

Common types of mutual funds include:

Equity Mutual Funds: Invest primarily in shares

Debt Mutual Funds: Invest in fixed-income instruments

Hybrid Funds: Mix equity and debt in varying proportions

Thematic or Sectoral Funds: Focus on specific industries or sectors

The performance of an actively managed mutual fund depends heavily on the fund manager’s skill and strategy.

Index funds are a category of mutual funds, but unlike actively managed funds, they follow a passive investment strategy. These funds replicate the performance of a chosen market index such as the Nifty 50 or Sensex.

Key features of index funds:

No active stock selection by fund managers

Lower management fees due to their passive approach

Returns closely track the performance of the chosen index

For instance, if you invest in a Nifty 50 index fund, your returns will reflect the movement of the Nifty 50 itself, minus the fund’s minimal expenses.

Here is a clear comparison:

|

Feature |

Mutual Funds (Active) |

Index Funds (Passive) |

|---|---|---|

|

Investment Style |

Active management |

Passive tracking |

|

Fund Manager Role |

Makes buy/sell decisions |

Minimal intervention |

|

Objective |

Outperform the market |

Match the market |

|

Expense Ratio |

Higher (1% to 2.5% typically) |

Lower (0.1% to 0.5% typically) |

|

Risk Level |

Depends on strategy chosen |

Market-linked, generally stable |

|

Return Potential |

Can outperform index |

Matches index performance |

|

Transparency |

Less frequent disclosures |

Often more transparent |

Mutual funds may offer higher returns but carry higher costs and risks. Index funds, while more predictable, are valued for their simplicity and cost-efficiency.

The Union Budget 2024 introduced significant changes to the taxation of mutual funds, effective in FY 2025–26.

Short-Term Capital Gains (STCG): Taxed at 20% if units are sold within 12 months

Long-Term Capital Gains (LTCG): Taxed at 12.5% on gains above ₹1.25 lakh annually, if held for more than 12 months

(These rates apply to redemptions made on or after 23 July 2024.)

All gains are taxed at the investor’s income slab rate, regardless of holding period

No indexation benefit for debt funds purchased on or after 1 April 2023

Hybrid, Gold, International Funds and Fund-of-Funds:

Treated like debt funds unless they maintain at least 65% in Indian equity

Key implications:

Index funds remain relatively tax-efficient for long-term investors.

Actively managed equity mutual funds face the same taxation as index funds but usually come with higher costs.

Debt funds have lost their former tax advantages, as neither indexation nor long-term capital gains classification applies.

The answer depends on your personal goals, risk tolerance, and time horizon.

Choose Index Funds if:

You want lower costs

You prefer returns that mirror the market

You aim for long-term wealth creation without active monitoring

Choose Mutual Funds if:

You believe in a fund manager’s ability to outperform the market

You are targeting higher-than-average returns

You are comfortable with higher fees and some level of volatility

For beginners and passive investors, index funds are often the most straightforward entry point. Experienced investors seeking potentially higher returns might opt for mutual funds. A combination of both can create balance in a diversified portfolio.

When it comes to index fund vs mutual fund, the decision is less about right or wrong and more about what fits your style of investing. Mutual funds can bring the possibility of beating the market but require trust in the fund manager and acceptance of higher fees. Index funds, on the other hand, quietly and consistently track the market, offering simplicity and cost savings.

Think of it as choosing between a guided tour and a well-marked trail. Both lead you to your destination, but the experience differs.

Index funds are built to replicate the market rather than outperform it. While this means the potential upside is capped, the lower costs and consistency often help them deliver competitive returns over time. In fact, many actively managed funds fail to beat their benchmarks in the long run.

Equity funds, including index funds, are taxed at 20% on short-term gains if sold within 12 months and at 12.5% on long-term gains above ₹1.25 lakh if held for more than 12 months. Debt funds are taxed differently: all gains are added to your income and taxed as per your slab rate, with no indexation or LTCG benefits.

For retirement goals, index funds provide cost efficiency and stable, market-linked returns. Mutual funds can complement them by adding diversification and the chance of higher growth. A balanced mix often works best: actively managed funds during the wealth-building years, and index funds later on to lock in stability.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!