In this chapter, we will talk about a critical aspect of money management in trading, called Position Sizing.

Position Sizing and Money Management:

So far over the previous four chapters, we have mostly focused on risk management and not really on money management. Now, it is time to turn focus to money management. But before we get there, let us talk about the difference between the two. While the two are very tightly linked to one another and are often used interchangeably, there are subtle differences between the two.

Risk management is mostly concerned with managing the risk side of a trade. This includes deciding on aspects such as the stop loss for each trade as well as the magnitude of each stop loss, in a way that no single trade has a negative impact on your capital that is greater than what you can reasonably tolerate. Meanwhile, money management is mostly concerned with managing your money efficiently and allocating capital across trades. In other words, money management is concerned with position sizing. This includes deciding on aspects such as the quantity (lots in case of derivatives) to be traded per position, how much of the overall capital to be deployed per trade, maximum number of trades that can be kept open at any point in time, etc. Keep in mind that the end objective of both risk and money management is to avoid capital ruin and grow your capital in a disciplined manner. Also keep in mind that even when managing money, you are taking into consideration your risk tolerance level and deploying money management strategies accordingly.

Before developing and implementing a position sizing strategy that suits your style of trading, it is important to focus on the following aspects:

- Capital in your trading account

- Types of securities that you trade

- Your risk tolerance level

The reason why the above factors are important is because one or a combination of the above factors tends to influence the type of position sizing strategies you would deploy. For instance, if you have ₹10 lacs in your trading account and if you trade derivatives, your position sizing strategy is likely to be much different than if you have, say, ₹10 lacs in your account but only trade cash instruments. Similarly, if you have ₹20 lacs in your trading account, you would be more inclined towards taking greater risks than if you have, say, ₹2 lacs in your trading account. The primary objective of position sizing is to inform you the quantity of a security that you should be trading, based on the capital in your account and the risk you are willing to assume.

You may wonder, how important is money management when it comes to trading? Well, the answer is: extremely important. In fact, it is as important as risk management, if not more. Consider this:

- If you have a capital of ₹100 and lose 10% of it, you will need to gain 11.11% to breakeven

- If you have a capital of ₹100 and lose 50% of it, you will need to gain 100% to breakeven

- If you have a capital of ₹100 and lose 90% of it, you will need to gain 900% to breakeven

See the difference? It is not easy to lose capital, but it is difficult to regain the lost capital. Hence, it is extremely important to be prudent when managing money and ensure that an irreparable damage is not caused to the capital. Let us now turn our attention straight to position sizing strategies.

There are many position sizing strategies that traders deploy. The two most popular strategies among them are:

- Fixed rupee (or points) allocation per trade

- Fixed percent allocation per trade

Let us now discuss about each of these strategies in more detail. For our discussion, we will focus primarily on equities. That said, keep in mind that the concepts explained in these strategies are applicable across securities and asset classes that are traded in the financial markets.

Fixed rupee allocation per trade:

Under this method, you allocate a fixed portion of your capital for every trade that you execute. For instance, let us assume that you have ₹1 lac in your trading account. Out of this and based on your risk tolerance, let us say that you have decided to allocate ₹10,000 per trade. So, whenever you take a position, you do so to the tune of ₹10,000 and decide on the quantity to trade based on this amount. As you can see, the quantity that you decide to trade will be a function of the stock price. For instance, if the stock price is ₹1,000, you would be able to trade 10 shares from ₹10,000. On the other hand, if the stock price is ₹25, you would be able to trade 400 shares. Now, what if the stock price is greater than ₹10,000? Well, in that case, you will not be able to trade such stocks. So, before deciding the amount of money to be allocated per trade, you need to take into consideration this factor too.

Once the capital to deploy per trade has been decided (₹10,000 in the above case), the next step is to determine the stop loss. Well, this is a part of risk management, wherein based on your risk profile, you allocate a protective stop loss to each trade. We have already talked about the types of stop losses in the previous chapter. You could use any one of those when trading. Depending on the type of trader you are, the magnitude of the stop loss chosen could vary – smaller stop loss for a day trader and a relatively larger stop loss for a positional trader. That said, it must be ensured that the stop loss chosen falls within your risk tolerance level. Let us now understand this using an example.

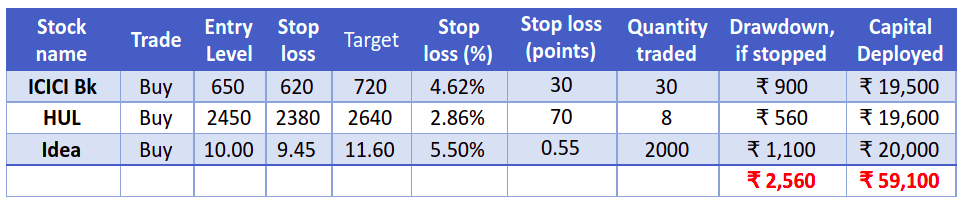

- Total Capital = ₹1 lac

- Capital deployed per trade = ₹20,000

Above, see that out of a total capital of ₹1 lac, the trader has decided to allocate ₹20,000 per trade. Based on the stock price, see how the quantity traded varies. It can be seen that if ₹20,000 is deployed for each trade from a total capital of ₹1 lac, the trader could initiate at most 5 different positions at any given point. That said, it is not necessary for him or her to always have 5 positions open. He or she could have just 1, or 2, or all 5 positions, depending on the prevailing opportunities to trade. Another thing to note is about rounding the quantity to be traded. For instance, at ₹650/share and an allocation of ₹20,000 per trade, the trader can buy 30.77 shares of ICICI bank. However, it is not possible to buy fractional shares. Hence, in case of fractions, you would need to round the number lower. Meanwhile, if all the three positions above were to get stopped out, your loss as a percent of capital deployed would be 4.33%. Your new total capital would now stand at ₹97,440, representing a decline of 2.56%.

The above strategy can be applied to derivatives as well. However, the capital required can vary quite drastically. With ₹1 lac of capital, you may not be able to trade in the equity derivative segment at all as the margins needed to trade derivatives tend to be upwards of ₹1 lac per contract. Hence, when using this position sizing strategy to trade derivatives, you would require much higher capital in your trading account, say at least 5-10 lacs. Before trading derivatives, always keep a track of how much upfront margin is required to trade. You could do so on the FYERS margin calculator, by clicking here. Let us now look at an example of derivatives.

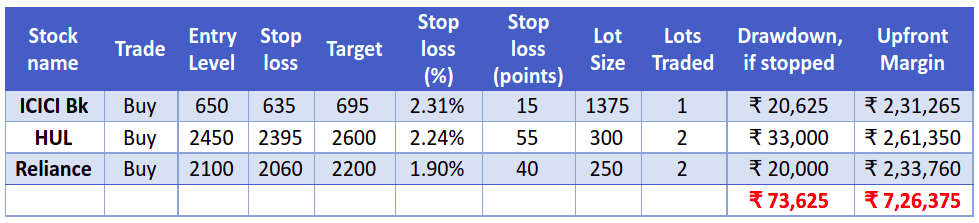

- Total Capital = ₹15 lacs

- Capital deployed per trade = ₹3 lacs

Above, see that out of a total capital of ₹15 lacs, the trader has decided to allocate ₹3 lacs per trade. Depending on the upfront margin requirement, see how the lots traded vary. For instance, in case of ICICI Bank, as the margin needed per lot is around ₹2.31 lacs, the trader would be able to trade only 1 lot. However, in case of Reliance, as the margin needed per lot is around ₹1.17 lacs, the trader would be able to trade 2 lots. Meanwhile, in the previous example (cash stocks), we had included Idea. However, the margin required to trade Idea in the futures segment is around ₹4 lacs. As the capital deployed per trade is ₹3 lacs, the trader won’t be able to take any position in Idea futures. Meanwhile, if all the positions above were to get stopped out, your loss as a percent of capital deployed would be 10.14%. Your new total capital would now stand at ₹14,26,375, representing a decline of 4.91%.

One of the drawbacks of the fixed rupee position sizing strategy is that over time, you could be taking either more risk or less risk than you ideally should. To simplify this, let us consider the cash segment example wherein the total capital was ₹1 lac and the capital deployed per trade was ₹20,000. This means you are deploying 20% of your capital per trade. Over time, let us assume that your capital doubled to ₹2 lacs, but you still continue deploying capital of ₹20,000 per trade. This means you are now deploying only 10% of your overall capital per trade. See that your risk-taking ability has gone down, which would also compromise on your potential returns. Let us now flip the coin. Over time, let us assume that your capital halved to ₹50,000, but you still continue deploying capital of ₹20,000 per trade. This means you are now deploying 40% of your overall capital per trade. See that you are now taking much greater risk than you ideally should. In worst case scenario, this could even cause your account to blow up.

One way to tackle this issue is to, over time, proportionately change the capital allocation per trade depending on whether your total capital is growing or declining. For instance, if your total trading capital has increased by, say, 50%, you could increase your capital allocation per trade by 50%. On the other hand, if your total trading capital has decreased by, say, 25%, you could decrease your capital allocation per trade by 25%. This way, you would ensure that neither are you taking more risk than you initially intended to nor are you taking less risk.

Fixed percent allocation per trade:

In the fixed percent position sizing strategy, the capital allocated per trade is not fixed. Instead, it is variable and is a function of two things:

- Risk per trade (as a percentage of total capital)

- Stop loss in points (difference between the entry price and the stop loss)

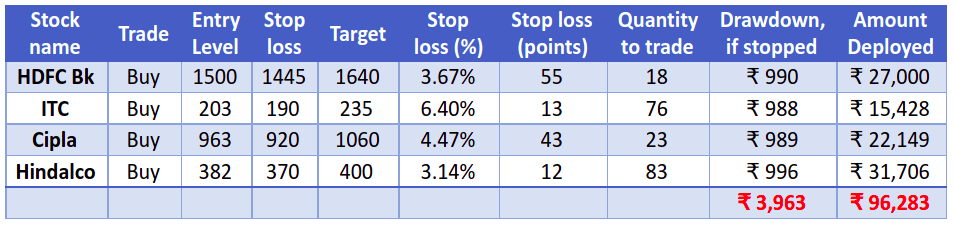

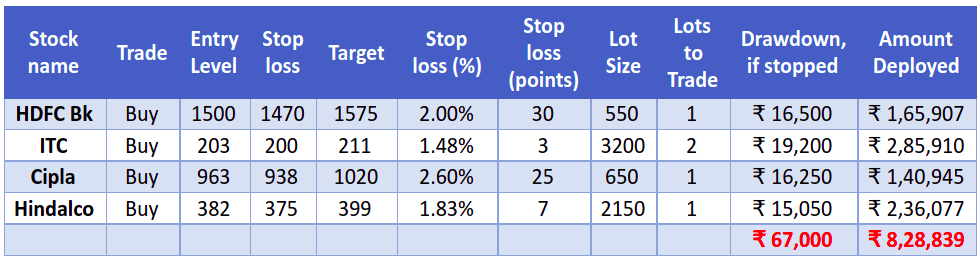

Let us understand this using an example. Let us say that you have a trading capital of ₹1 lac. Let us say that, based on your risk profile and tolerance level, you have decided to risk 1% of your total capital per trade. So, in value terms, the risk per trade is ₹1,000. Now, let us say that you have looked into the chart of HDFC bank. The stock is currently priced at ₹1,500 and you intend to buy at that level. You see support at ₹1,450 and expect the stock to rise 8-10% as long as this support holds. Based on this, you decide to place a stop loss at ₹1,445, which is 55 points away from the entry level. How much quantity of HDFC bank should you buy, such that the loss is capped at ₹1,000 per trade? Well, the answer is 18 shares (1,000 ÷ 55, rounded down to the nearest integer). So, after initiating the long position, if your stop loss were to get hit, you will lose ₹990 (18 shares * loss of ₹55 per share). Let us now derive a formula for the quantity to trade based on the fixed percent position sizing strategy:

- Total Capital = ₹1 lac

- Risk per trade as a percentage of total capital = 1%

- Risk per trade in rupee terms = ₹1,000 (as the capital changes, so does this figure)

In the above example, observe the quantity to trade column to check how the values are calculated. The drawdown for each stock is calculated as the stop loss (in points) times the quantity. See that each of this figure is capped at or below ₹1,000. This is the maximum that you stand to lose per trade. Meanwhile, the amount deployed for each stock is calculated as the entry price times the quantity. In the fixed rupee position sizing method, recollect that the amount deployed per trade was fixed, while the drawdown varied. Meanwhile, in the fixed percent position sizing method, it is the opposite. That is, the drawdown is fixed, while the amount deployed varies, depending on the extent of the stop loss chosen and the percentage risk per trade. Meanwhile, above, if all the four positions were to get stopped out, your loss as a percent of capital deployed would be 4.12%. Your new total capital would then stand at ₹96,037, representing a decline of 3.96%. Going forward, the risk per trade would be 1% of ₹96,037, which is ₹960. See how the risk per trade in rupee terms is a function of the capital.

Depending on factors such as your risk profile, risk tolerance level, capital in hand, and reward expectations, you could alter your risk per trade as a percentage of the total capital. You could define a risk per trade of, say, 0.25%, 0.5%, 1%, 1.5%, 2%, 3% etc. Beware that the larger the risk, the larger would be the capital required to trade and the larger would be the drawdown per trade.

Certain complications of the fixed percent position sizing approach:

Complication 1: A higher risk per trade

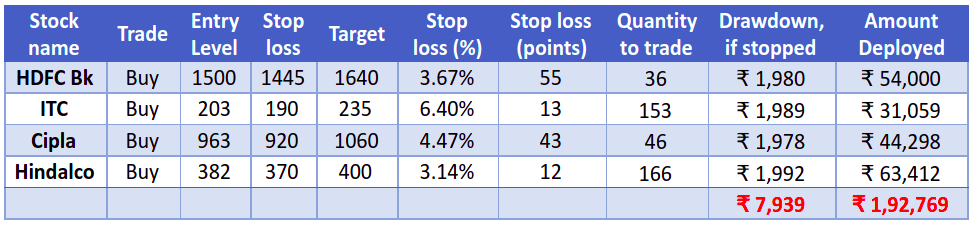

While the fixed percent position sizing approach is a widely followed and an incredibly useful method of determining the ideal position size, there are a few complications that you could face when deploying this method. Let us understand these complications by considering the same example as above, but with a higher risk per trade percentage:

- Total Capital = ₹1 lac

- Risk per trade as a percentage of total capital = 2% (₹2,000)

Did you notice something in the above table? When the risk per trade is 2% of total capital, the capital required to take positions in the above four stocks is ₹1,92,769. As the total capital available is only ₹1 lac, the trader won’t be able to take positions in all the four stocks. Instead, he or she will have to choose a combination of two stocks such that the combined capital deployed in those would be less than ₹1 lac.

Complication 2: A smaller stop loss

In a similar fashion, how far the stop loss is from the entry price also has a bearing on the capital deployed per position. For instance, consider the following table (risk per trade assumed here is 1%):

Above, if the entry is 1500 and stop loss is just 5 points away from the entry, see that the trader can trade 200 shares of HDFC bank, such that the maximum loss he or she suffers is only ₹1,000. However, notice that to buy 1500 shares, the capital required is ₹3 lacs. Because the capital that the trader has is only ₹1 lac, he or she won’t be able to buy 200 shares of HDFC bank.

Let us consider one more example (risk per trade is 1%).

Above, when the stop loss is 20 points away from the entry level, the trader would need to trade 50 shares of HDFC bank, such that the drawdown is ₹1,000, in case the stop loss were to get hit. However, to do so, the capital required would be ₹75,000. The question is, out of a total capital of ₹1 lac, would it be wise to put 75% of that in a single stock? Probably not! Hence, when deploying the fixed percent position sizing strategy, these complications are some important things that you need to keep in mind before deciding to act.

Let us now apply the fixed percent position sizing strategy to derivatives. As you might know from our earlier conversation, you need much more capital to trade in derivatives. Let us assume the following:

- Total Capital = ₹15 lac

- Risk per trade as a percentage of total capital = 1.5% (₹22,500)

Above, the number of lots to trade for each stock is calculated as follows and rounded down to the nearest integer:

Meanwhile, the drawdown per stock is calculated as the product of the stop loss (points), the lot size, and the number of lots traded. Finally, the amount deployed per stock is calculated as the product of the number of lots traded and the initial margin. As said earlier, you can find the initial margin required for each stock futures contract on the FYERS margin calculator web page. Notice the drawdown column. See that the maximum loss for each stock is capped to 1% (₹22,500) of the total capital. The difference is of course because of the effects of rounding down the lot size (as you cannot buy fractional lots). Meanwhile, if all the positions above were to get stopped out, your loss as a percent of capital deployed would be 8.08%. Your new total capital would now stand at ₹14,33,000, representing a decline of 4.47%.

Suggestions on risk and money management:

Let us wind up this chapter by talking about some suggestions and guidelines about risk and money management in trading:

-

Trading is a high risk, high reward activity. Only set aside that amount of capital from your savings that you are willing to risk

-

If you are new to trading, start with cash markets. As you gain experience and your capital grows, you could move into derivatives

-

When trading derivatives, ensure that you have ample capital in you trading account

-

Never trade without a proper risk and money management strategy in place

-

You should always have in place a protective stop loss when entering a position

-

Never revise the stop loss against the direction of your trade. Instead, when necessary, revise the stop loss in the direction of your trade

-

Do not let the emotions of greed, fear, and hope get the better of you

-

You do not have to always trade. Only do so when you spot good trading opportunities

-

Timing a trade is important. Entering at the wrong time could cost you money, even if your view turns out to be eventually correct

-

Never risk more than what you can reasonably afford to lose per trade

-

Never risk your entire capital in one trade. Instead, use proper position sizing strategies to ensure that you are not over committing to a single trade

-

Before entering a trade, ensure that the reward to risk ratio is attractive

-

Leverage is a double-edged sword. Use it wisely when trading and ensure that losses, if any, are well within your tolerance limit

-

Scaling in and out can be a good strategy to deploy as and when needed. But be sure to assess the pros and cons of scaling before implementing it

-

Preferably, risk no more than 2% of your overall capital on a single trade

-

Discipline is the key to success! Do not trade without a having in place a robust trading plan

Next Chapter

Comments & Discussions in

FYERS Community