By now, we have studied various aspects of Options, starting right from the basics before proceeding to more complex areas. Now, in this chapter, we will talk about some of the other important aspects of Options that we have not yet discussed but are worth knowing. So, let us get started.

Put Call Ratio (PCR)

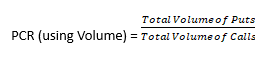

As the name suggests, Put Call ratio is a ratio showing the open interest of Put options relative to the open interest of Call options. Occasionally, volume is also used in place of open interest. Put Call ratio, which is commonly abbreviated as PCR, is usually calculated on a daily basis. It helps one to see the build-up of overall Open Interest or Volume for a particular option structure. Recollect that in the previous chapter, we had talked about Option Chain, wherein one could see the Option structure of a particular underlying instrument for a particular expiration at various strike prices. In the NSE Option Chain, if you had noticed, the Open Interest of all Call options for a particular series are totalled, and so are the Open Interest of all Put options. The aggregate figures that are thus arrived at can then be used to calculate the PCR. Below, the PCR is expressed in equation form:

From the above formula, we can see that the PCR could be either less than 1 or more than 1. When the open interest of Puts is less than the open interest of Calls, PCR is less than 1. On the other hand, when the open interest of Puts is greater than the open interest of Calls, PCR is more than 1. If you recollect, Put options are bearish, because they gain in value when the price of the underlying instrument falls, and vice versa. Similarly, Call options are bullish, because they gain in value when the price of the underlying instrument rises, and vice versa. So, more Put OI than Call OI (PCR of more than 1) for a particular series indicates that buyers, in general, are bearish on the underlying instrument as they are buying more Put options than Call options. Conversely, more Call OI than Put OI (PCR of less than 1) for a particular series indicates that buyers, in general, are bullish on the underlying instrument as they are buying more Call options than Put options.

However, there is an alternate way of looking at this. Remember, in the previous chapter, we said that option buyers are usually retail participants while option sellers are professional traders. As we know, professional traders are usually more informed about the markets than are retail traders. So, if you think from a seller’s perspective, more Put OI than Call OI for a particular series meansPut writers are more aggressive than Call writers, which suggests that supports could hold (due to greater Put writing) and price of the underlying could move higher. Alternatively, more Call OI than Put OI for a particular series means Call writers are more aggressive than Put writers, which suggests that resistances could hold (due to greater Call writing) and price of the underlying could move lower.

PCR is widely used as a contrarian indicator to identify the sentiment of option traders. This is especially true when the ratio is at an extreme reading. A very high ratio, for instance, indicates that option buyers are excessively bearish on the underlying. This can provide warning that the market might be oversold and could reverse its trend from down to up. Alternatively, a very low ratio indicates that option buyers are excessively bullish on the underlying. This can provide warning that the market might be overbought and could reverse its trend from up to down. Having said that, an extreme reading in PCR must not be immediately used to initiate a counter position. Instead, one must look at other indicators also to confirm this extreme reading in PCR and must act only when there is some sort of reversal signalled in the price itself. Again, one could think from an option writer’s perspective.For instance, an extremely high PCR reading meansa greater number of supports at lower levels. If these supports hold, one can consider initiating a counter trade (i.e. go long).Similarly, an extremely low PCR reading means a greater number of resistances at higher levels. If these resistances hold, one can consider initiating a counter trade (i.e. go short).

Talking about my experience, whenever I see an extreme reading in PCR, I usually combine it with Technical Analysis to decide when to enter a counter trade.For instance, if I see that Nifty is trading at 12000 and that the PCR is very high compared to the historical average, I will keep a close watch on a nearby resistance level where a significant number of Call options have been written. If this resistance level is breached with volumes and if it is also confirmed by my Technical signals, I would consider initiating a longposition on the underlying by placing a stop loss either below a nearby support where there is a lot of Put writing or below a key technical level. Similarly, if Nifty is trading at 12000 and the PCR is very low compared to the historical average, I will keep a close watch on a nearby support level where a significant number of Put options have been written. If this support level is breached with volumes and if it is also confirmed by my Technical signals, I would consider initiating a short position on the underlying by placing a stop loss either above a nearby resistance where there is a lot of Call writing or above a key technical level.

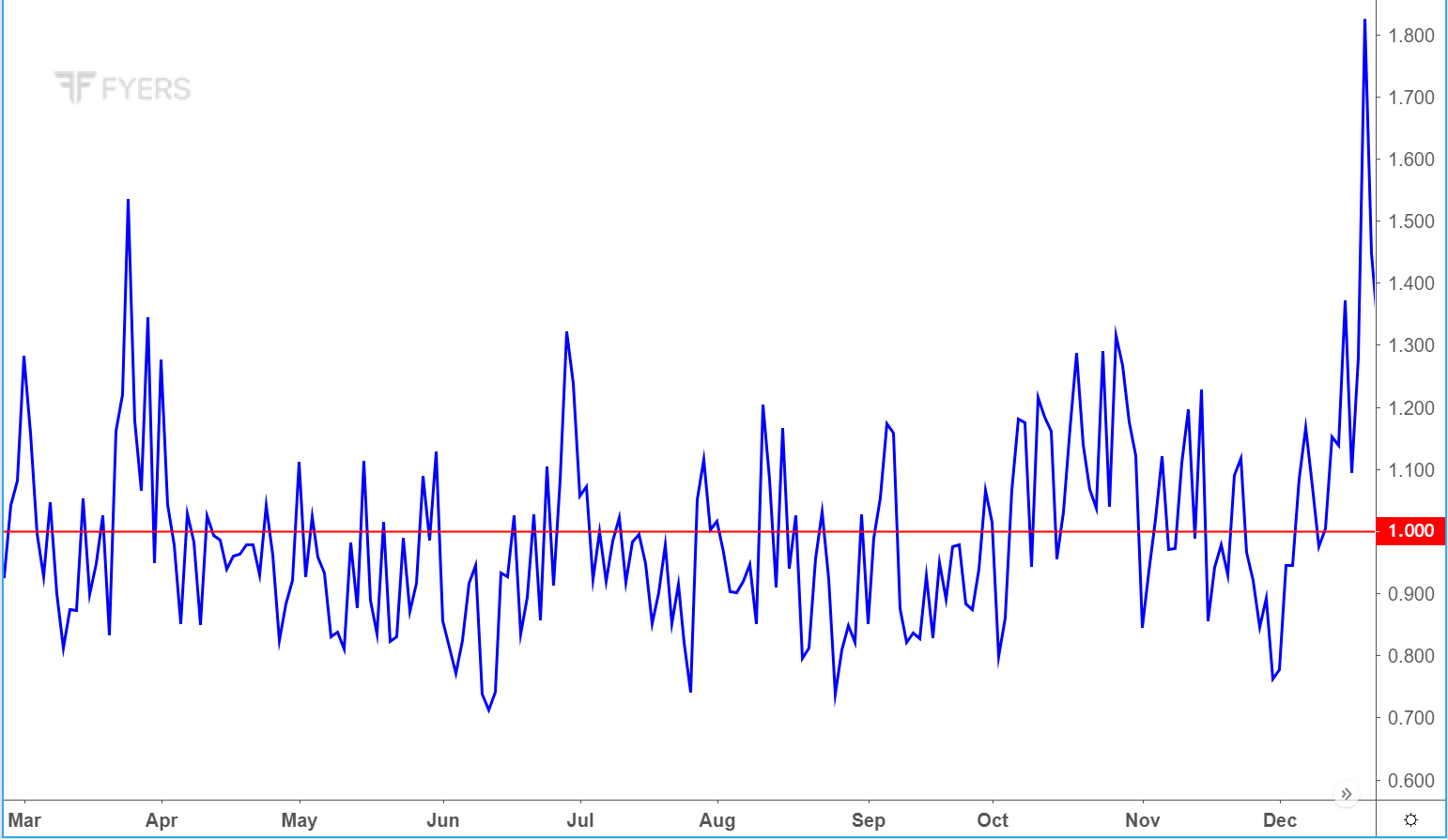

What level of PCR is considered high and what is considered low? Well, this varies from securities to securities and from time to time. One must look at the historical movements in the PCR of a particular underlying instrument to determine the historical extremes in the ratio. Usually, but not always, a PCR of 1.5 and above is considered very high and indicates that the market could be oversold. On the other hand, a PCR of 0.6 and below is considered very low and indicates that the market could be overbought. Again, keep in mind that these levels may vary from securities to securities and from time to time. Hence, what is a high PCR reading and what is a low PCR reading can only be determined by looking at historical PCR data.

PCR can also be calculated for an individual Call Option and the corresponding Put Option having the same underlying instrument, strike price, and expiry. However, one must not rely much on this statistic because it could yield inaccurate results, given that there are many strike prices at which options are written within a particular Option Chain, which could yield contrasting PCR.Instead, the best way to use PCR is to use it holistically, i.e. total the OI or volume of all Call options and Put options within an Option Chain, and then calculate the ratio.Alternatively, one could also total the OI or volume of all Call options as well as all Put options across various maturities for a particular underlying instrument, and then calculate the PCR in order to understand the market-wide positioning for a particular underlying asset. For instance, to calculate the PCR for Nifty options expiring in February, one could total Call OI and Put OI, and then calculate the PCR for the February series. On the other hand, to calculate the PCR of market-wide positions for Nifty monthly options, one could total Call OI and Put OI across maturities (such as Nifty monthly options expiring in February, March, April etc.), and then calculate the PCR to find out the market-wide positioning.

The table below shows the implications of changes in the PCR. Keep in mind that the numerator consists of Puts and the denominator consists of Calls:

| PCR is… | What does this mean? |

| Rising | # of Puts is increasing, or # of Calls is decreasing, or both |

| Falling | # of Calls is increasing, or # of Puts is decreasing, or both |

Finally, the table below summarizes the things we have learned so far about the PCR and how to interpret the PCR:

| PCR is… | Implication | Remarks |

|

Rising and above 1 |

Bearish, down trend likely to continue |

Indicates more Puts are being bought than Calls. If the prevailing trend is down, it is likely to continue as and whenkey option supports, where a lot of Puts have been written, is convincingly broken. |

|

Rising and above 1.5 |

Cautiously bearish, but look for signs of reversal |

Indicates that excessively greater number of Puts have been bought than Calls. It indicates that the market is oversold. Break above a key option resistance, where a lot of Calls have been written, could indicate a reversal in trend from down to up. |

|

Falling and below 1 |

Bullish, uptrend likely to continue |

Indicates more Calls are being bought than Puts. If the prevailing trend is up, it is likely to continue as and when key option resistances, where a lot of Calls have been written, is convincingly broken. |

|

Falling and below 0.5 |

Cautiously bullish, but look for signs of reversal |

Indicates that excessively greater number of Calls have been bought than Puts. It indicates that the market is overbought. Break below a key option support, where a lot of Puts have been written, could indicate a reversal in trend from up to down. |

Keep in mind that the above are just guidelines and not hard and fast rules. When applying PCR in the real world, one has to be very flexible in his/her approach and take decisions logically, based on prevailing market conditions.

Below mentioned are some of the key points to remember about PCR:

-

PCR above 1 means more Puts are being bought than Calls, which indicates at bearishness.

-

PCR below 1 means more Calls are being bought than Puts, which indicates at bullishness.

-

When PCR reading is extremely high, it indicates that the market could be oversold as significantly more Puts have been bought relative to Calls.

-

When PCR reading is extremely low, it indicates that the market could be overbought as significantly more Calls have been bought relative to Puts.

-

When looking at the extreme PCR readings however, one has to be very cautious and must also think from an option writer’s perspective.

-

An extremely high PCR reading also indicates that Put writers are more aggressive than Call writers, which suggests that supports, where a lot of Puts have been written, could hold.

-

An extremely low PCR reading also indicates that Call writers are more aggressive than Put writers, which suggests that resistances, where a lot of Calls have been written, could hold.

-

Hence, when PCR reading is extremely high, one must wait for markets to show signs of upside reversal before acting. One way to act is to wait for the immediate resistance, where a lot of Calls have been written, to break. This is because break above such resistances could cause unwinding of short Call positions, which in turn could be the first trigger that would cause the underlying to start heading higher

-

Similarly, when PCR reading is extremely low, one must wait for markets to show signs of downside reversal before acting. One way to act is to wait for the immediate support, where a lot of Puts have been written, to break. This is because break below such supports could cause unwinding of short Put positions, which in turn could be the first trigger that would cause the underlying to start heading lower.

Volatility Index (VIX)

In an earlier chapter (On Vega), we had talked about a concept called Implied Volatility. Just to recap, Implied volatility (or IV) is used to measure future volatility. It is based on what market participants imply the volatility of the underlying instrument to be over the remaining life of an option contract. Because IV is forward looking rather than backward looking, it is heavily used in the pricing of option contracts. Implied volatility is expressed as a percentage on an annualized basis. To understand more about it, we suggest you go through Chapter 7 on Option Vega.

In this section, we shall talk about Volatility index, which is commonly abbreviated as VIX. VIX is usually expressed as the 30-day implied volatility of index options that are traded on an exchange. It is a very commonly used measure of risk and tells a lot about the prevailing risk sentiment in the market. VIX and the underlying instrument tend to move in the opposite direction. In other words, a rise in the price of the underlying is accompanied by VIX heading lower, while a fall in the price of the underlying is accompanied by VIX heading higher. VIX tends to rise sharply during times of severe market stress. Broadly speaking, the prevailing value of VIX can be interpreted as the likely percent change in the price of the underlying over the next 30 days. For instance, let us say that the current VIX reading is 18%. As VIX is expressed in annualized terms, a reading of 18% means that the underlying is likely to move approximately 1.5% over the next 30 days. So, as we can see, the higher the VIX, the higher is the market’s expectationabout the future price movement of the underlying, and vice versa.

VIX can be measured for various financial instruments. One of the most commonly referred to VIX index in the world is the CBOE Volatility Index. It measures the 30-day implied volatility of the S&P 500 index options and is based on the midpoint of the Bid and Ask quotes of near-term ATM and OTM options. It is very closely tracked by all major market participants around the world. In fact, the CBOE VIX is also heavily traded in the US, both in the form of futures contracts and options contracts. In India, VIX measures the 30-day implied volatility of the Nifty index options and is based on the best Bid and Ask quotes of the near-month and mid-month Nifty OTM options.

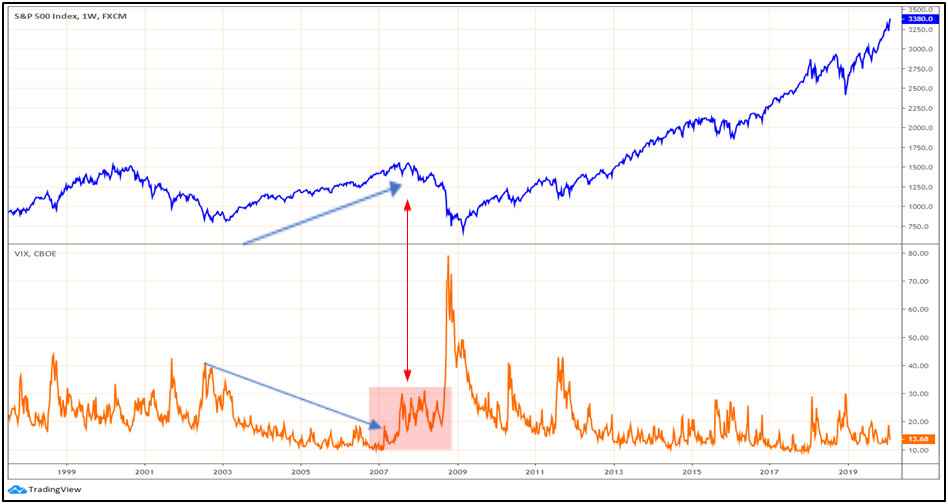

The above chart is the daily chart of the S&P 500 index and the CBOE VIXfor the past three years. Compare the regions that are marked using the blue arrows. It can be seen that during periods when the S&P 500 is trending higher, it has usually coincided with VIX trending lower and within a range of 10 and 20. Now observe the regions that are marked using the red arrow. It can be seen that during times of market stress, there is a tendency for VIX to rise sharply and move upwards of 30-35 levels. So, as we can see, VIX shares an inverse correlation with the S&P 500 index (or for that matter any equity index around the world). A rising and a high VIX reading indicates at market stress and as such, is negative for risk assets (equities, industrial metals and crude oil, high-yielding currencies etc.) and positive for safe havens (treasuries, gold, low-yielding currencies etc.). On the other hand, a falling and low VIX reading indicates at optimistic market conditions and as such, is positive for risk assets and negative for safe havens.

The above chart is the weekly chart of the S&P 500 index and the CBOE VIX for the past two decades. Notice that VIX frequently moved towards 40 and struggled to sustain below 20 during the 2-year bear market in the S&P 500 index between 2000 and 2002. Now contrast this to movements in VIX post 2011 till date. We can see that VIX frequently moved towards 10 and barely moved beyond 30 during this decade-long bull market in equities. An important concept can be gleaned from this. There is a tendency for VIX to move in ranges during bull and bear market. For instance, notice that during bull markets, VIX tends to move between 10 and 30; while during bear markets, there is a tendency for VIX to move between 20 and 40. If the range of VIX is shifting higher from, say, 10 and 30 to, say, something like 15 and 35, it is a sign that the uptrend in the underlying is weakening and that the market could start its correction lower. On the other hand, if the range of VIX is shifting lower, it is a sign that the downtrend in the underlying is weakening and that the market could start moving higher. Using this concept, notice how the VIX moved during the period marked using red arrows. Observe that just prior to the onset of the 2008 Global Financial Crisis, the range of VIX shifted higher from 10 and 20 to 20 and 30. This shift in the range of VIX was then accompanied by a very steep decline in the S&P 500 index that took the VIX to an abnormally high reading of 80.

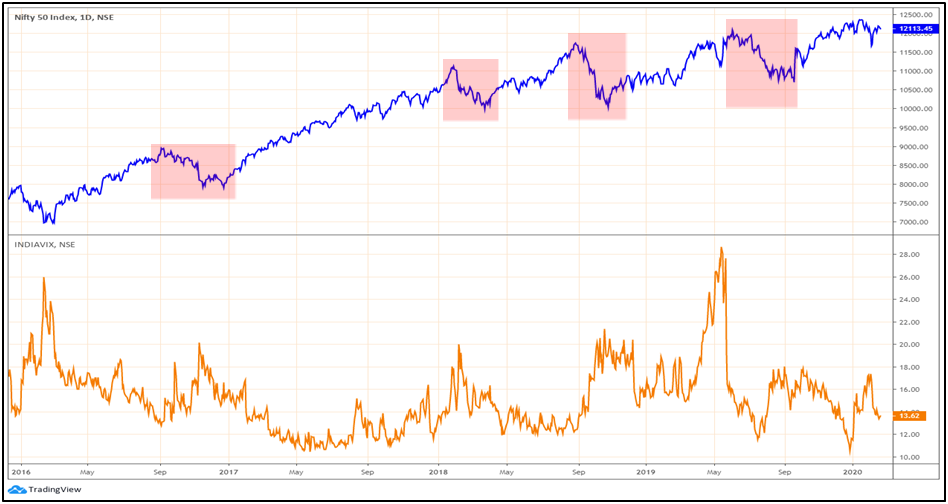

The above chart is the daily chart of the Nifty index and the India VIX for the past four years. Notice that during this four year bull market, periods of price correction in Nifty (regions in red boxes) were accompanied by the VIX moving higher. An interesting thing to observe in this chart is the behaviour of price and VIX during May 2019. During this period, notice that despite the rally in Nifty, there was a sharp jump in VIX during this period. Later, the subsequent decline in Nifty over the next one quarter was accompanied by VIX moving lower. This brief breakdown in correlation between Nifty and VIX was due to the 2019 General Elections results that were scheduled to be announced in late-May. There is a tendency for volatility to rise ahead of major events, making Option premiums more expensive. However, once the event is over, volatility tends to return to normal levels. One needs to be aware of this when trading.

Below mentioned are some of the key points to remember about VIX:

-

VIX is commonly referred to as Fear index, because it tells a lot about the prevailing market sentiment.

-

During times of panic and market stress, VIX tends to rise; and during times of market calm and confidence, VIX tends to fall.

-

During an uptrend, it is common for VIX to fall towards 12-10 levels. During a downtrend, VIX often tends to rise above 30-35 levels.

-

There is a tendency for VIX to rise ahead of major events, before returning to normal levels once the events are behind.

-

Shifts in the traditional range of VIX can often provide clues that the trend of the underlying instrument could be about to change.

Combining PCR and VIX

Now that we have talked about PCR and VIX in detail, it is time to discuss about how the two can be combined to get an even stronger understanding of the prevailing market sentiment.Just remember two things. One is that a rising VIX means market participants are getting more anxious and that fear is starting to increase in the marketplace, whereas a falling VIX means market participants are getting optimistic and that fear is receding in the marketplace. The second is that a rising PCR means either the Put activity is increasing or the Call activity is decreasing or a combination of both, whereas a failing PCR means either the Put activity is decreasing or the Call activity is increasing or a combination of both.

-

If the rise in VIX is accompanied by an increase in PCR, it indicates that Put buyers (who have a bearish stance on the underlying) are becoming more aggressive and that the demand for Puts could be outpacing the supply for them. Additionally, it could also mean Call holders (who have a bullish stance on the underlying) are exiting their positions. Either ways, this is a bearish signal.

-

If the fall in VIX is accompanied by an increase in PCR, it indicates that Put writers (who have a bullish stance on the underlying) are becoming more aggressive and that the supply for Puts could be outpacing the demand for them. Additionally, it could also mean Call writers (who have a bearish stance on the underlying) are exiting their positions. Either ways, this is a bullish signal.

-

If the rise in VIX is accompanied by a decrease in PCR, it indicates that Call writers (who have a bearish stance on the underlying) are becoming more aggressive and that the supply for Calls could be outpacing the demand for them. Additionally, it could also mean Put writers (who have a bullish stance on the underlying) are exiting their positions. Either ways, this is a bearish signal.

-

If the fall in VIX is accompanied by a decrease in PCR, it indicates that Call buyers (who have a bullish stance on the underlying) are becoming more aggressive and that the demand for Calls could be outpacing the supply for them. Additionally, it could also mean Put holders (who have a bearish stance on the underlying) are exiting their positions. Either ways, this is a bullish signal.

Maximum Pain Theory

Now, it is time to focus on a concept that is widely spoken about, at least during the last few days of an Options contract. This concept, or rather should I say theory, is popularly known as the Maximum Pain theory. This theory refers to a particular point (strike price) in the Option Chain that would cause the maximum pain or maximum loss to option holders. Why option holders and not option writers? Well, remember what we said earlier. Option buying is usually done by retail market participants, whereas Option writing is usually done by professional traders. As professional traders are usually better informed than retail traders, they tend to write options at such strikes which they believe would expire worthless and thereby help them in retaining the premium that they have received upfront from option buyers. Also, remember the concept of time value. Because this component of option price keeps eroding with each passing day, the odds are stacked against the buyer earning a profit. Recollect from our discussion in earlier chapters that for buyers to make money, the underlying price has to trend in the buyer’s direction (up in case of long call and down in case of long put). However, option writers can make money even if the underlying price remains sideways. Because of all these factors, option buyers usually end up losing the premium that they have paid upfront, whereas option sellers usually get to keep the premiums.

Now coming back to our main topic of discussion, the Maximum Pain theory states that as the expiration approaches, there is a tendency for the price of the underlying asset to gravitate towards the strike price where the largest number of option contracts will expire worthless. In other words, Maximum Pain is that point (strike price) on the Option Chain that would cause the least amount of loss to option writers and the maximum loss tooption buyers. Usually, this happens to be the strike price wherethe combined open interest of Calls and Puts is the highest. Let us now look at how the Maximum Pain level is calculated. Keep in mind that this is the level where option seller would suffer the least and option buyer would suffer the most.

| Call OI | Strike Price | Put OI |

| 800 | 11800 | 1300 |

| 1200 | 11900 | 1500 |

| 1500 | 12000 | 1400 |

| 1600 | 12100 | 1100 |

| 1400 | 12200 | 700 |

For simplicity’s sake, let us assume that there are only 5 strikes available on Nifty at a particular point in time. In order to calculate the Maximum Pain level, one will have to assume that Nifty closes at each of these strikes at expiration and then calculate where the Maximum Pain point lies. So, let us get started.

Nifty expires at 11800

Let us start with the 11800 strike first. If Nifty expires at this level, none of the Call options would be exercised as none of them are ITM. As a result, the option sellers will get to keep the entire premium and as such, will incur no losses. Now moving to the Put side, those who had written 11800 options will not lose any amount because the option is expiring ATM. However, for each of the other Put options,writers would end up losing money as each of these options are ITM. As the 11900 strike has expired 100 points ITM, the Put writers’ loss at this strike would amount to ₹1,12,50,000 (₹100 loss * 1500 Put OI * 75 lot size). Similarly, for each of the 12000,12100, and 12200 strikes, the Put writers’ loss would amount to ₹2,10,00,000,₹2,47,50,000, and ₹2,10,00,000, respectively. So, if Nifty closes at 11800, Call writer’s loss across all the strikes would be 0, while Put writer’s loss across all the strikes would be ₹7,80,00,000. Combined, the loss of both the writers,if Nifty closes at 11800, would amount to ₹7,80,00,000.

| Strike | 11800 | 11900 | 12000 | 12100 | 12200 | Total |

| Calls | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 |

| Puts | ₹ 0 | ₹ 1,12,50,000 | ₹ 2,10,00,000 | ₹ 2,47,50,000 | ₹ 2,10,00,000 | ₹ 7,80,00,000 |

Nifty expires at 11900

If Nifty expires at 11900, those who had written the 11800 Call will be on the losing side. The loss suffered by them would amount to ₹60,00,000 (₹100 loss * 800 Call OI * 75 lot size). Meanwhile, each of the other Call writers would not suffer any loss as none of these options are expiring ITM. Now moving to the Put side, those who had written options at strikes 11800 and 11900 will not suffer any loss as none of these are expiring ITM. However, for each of the other Put options, writers would end up losing money as each of these options are ITM. For the 12000, 12100, and 12200 strikes, the Put writers’ loss would amount to ₹1,05,00,000, ₹1,65,00,000, and ₹1,57,50,000, respectively. So, if Nifty closes at 11900, Call writer’s loss across all the strikes would be ₹60,00,000, while Put writer’s loss across all the strikes would be ₹4,27,50,000. Combined, the loss of both the writers would amount to ₹4,87,50,000.

| Strike | 11800 | 11900 | 12000 | 12100 | 12200 | Total |

| Calls | ₹ 60,00,000 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 60,00,000 |

| Puts | ₹ 0 | ₹ 0 | ₹ 1,05,00,000 | ₹ 1,65,00,000 | ₹ 1,57,50,000 | ₹ 4,27,50,000 |

Nifty expires at 12000

In a similar way, let us now perform the rest of the calculations.

| Strike | 11800 | 11900 | 12000 | 12100 | 12200 | Total |

| Calls | ₹1,20,00,000 | ₹ 90,00,000 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 2,10,00,000 |

| Puts | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 82,50,000 | ₹ 1,05,00,000 | ₹ 1,87,50,000 |

Nifty expires at 12100

| Strike | 11800 | 11900 | 12000 | 12100 | 12200 | Total |

| Calls | ₹ 1,80,00,000 | ₹ 1,80,00,000 | ₹ 1,12,50,000 | ₹ 0 | ₹ 0 | ₹ 4,72,50,000 |

| Puts | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 52,50,000 | ₹ 52,50,000 |

Nifty expires at 12200

| Strike | 11800 | 11900 | 12000 | 12100 | 12200 | Total |

| Calls | ₹ 2,40,00,000 | ₹ 2,70,00,000 | ₹ 2,25,00,000 | ₹ 1,20,00,000 | ₹ 0 | ₹ 8,55,00,000 |

| Puts | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 | ₹ 0 |

The table below shows the losses suffered by Call writers at each assumedexpiration levels, the losses suffered by Put writers at each assumed expiration levels, as well as the total losses suffered at each assumed expiration levels.

| Expiry at | Loss to Call Writers at various Strikes | Loss to Put Writers at various Strikes | Total Loss |

| 11800 | ₹ 0 | ₹ 7,80,00,000 | ₹ 7,80,00,000 |

| 11900 | ₹ 60,00,000 | ₹ 4,27,50,000 | ₹ 4,87,50,000 |

| 12000 | ₹ 2,10,00,000 | ₹ 1,87,50,000 | ₹ 3,97,50,000 |

| 12100 | ₹ 4,72,50,000 | ₹ 52,50,000 | ₹ 5,25,00,000 |

| 12200 | ₹ 8,55,00,000 | ₹ 0 | ₹ 8,55,00,000 |

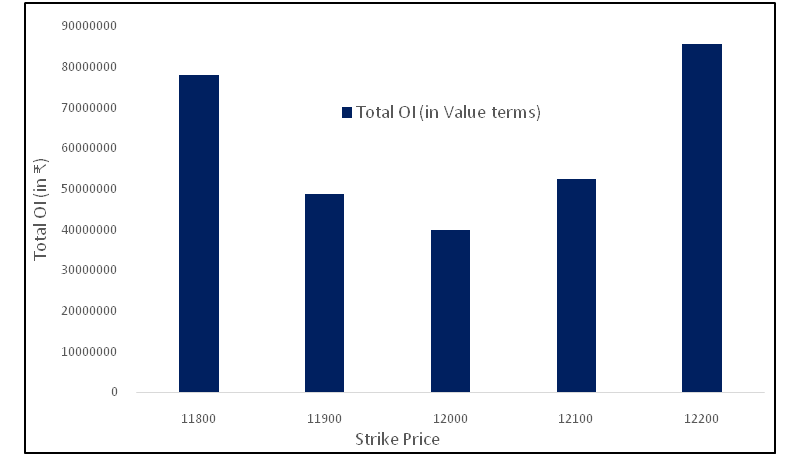

As stated earlier in the chapter, Maximum Pain is that point (strike price) on the Option Chain that would cause the least amount of loss to option writers and the maximum loss to option buyers. In the table above, that level happens to be 12000, where option writers suffer the lowest loss (₹ 3,97,50,000). This is the level of Maximum Pain, because it is at this level that option buyers suffer the most. As the expiration approaches, there is a tendency for the underlying asset price to gravitate towards the level of Maximum Pain. So, in the case of the above example, as per the Maximum Pain theory, Nifty is likely to expire around 12000.

The chart above shows the total outstanding open interest (in value terms) assuming expiry at each strike price, as was considered in the example above.

How to apply the concept of Maximum Pain?

Calculating the Maximum Pain as option contracts near expiration can help one in identifying where the price of the underlying asset could be at expiration. But how exactly does one benefit by knowing where the expiration could be? Well, by knowing the Maximum Pain point, one could deploy strategies to profit from such setups. For instance, given that Maximum Pain is the strike price at which the highest number of option contracts expire worthless, a Call writer can write a Call option whose strike price is above the Maximum Pain level; while a Put writer can write a Put option whose strike price is below the Maximum Pain level. Similarly, a Call buyer can buy a Call option whose strike price is below the Maximum Pain level; while a Put buyer could buy a Put option whose strike price is above the Maximum Pain level.

Also, once the Maximum Pain level has been identified, one can compare it with the underlying price to identify the potential trend of the underlying until option expiration. This can then be used to either build new positions or to close out existing positions. For instance, if the underlying price at present is above the Maximum Pain level, given that there is a tendency for the underlying price to gravitate towards the level of Maximum Pain, one can expect a down move in the price of the underlying until expiration and thereby deploy bearish derivative strategies (or close out existing bullish positions that are nearing expiration); whereas if the underlying price at present is below the Maximum Pain level, one can expect an up move in the price of the underlying until expirationand thereby deploy bullish derivative strategies (or close out existing bearish positions that are nearing expiration).

That said, keep in mind that Maximum Pain strategy should be used only in case of liquid options. Also, one must constantly monitor the Option Chain on a real time basis, because the data keeps changing every moment until expiration. Hence, there is a need to keep a track of the Maximum Pain point on a real time basis and make changes as and when needed, rather than calculating it as a onetime basis.

Keep in mind that the example we presented above had very few strikes (5 to be precise). In the real word, there are various strikes at which options are traded. Take the case of Nifty Option Chain below:

| Call OI | Strike Price | Put OI | Total OI |

| 0 | 10150 | 221 | 221 |

| 4 | 10200 | 20 | 24 |

| 1 | 10250 | 27 | 28 |

| 37 | 10300 | 57 | 94 |

| 452 | 10350 | 220 | 672 |

| 2261 | 10400 | 879 | 3140 |

| 0 | 10450 | 0 | 0 |

| 6901 | 10500 | 5409 | 12310 |

| 0 | 10550 | 9 | 9 |

| 84 | 10600 | 270 | 354 |

| 0 | 10650 | 45 | 45 |

| 188 | 10700 | 519 | 707 |

| 0 | 10750 | 0 | 0 |

| 159 | 10800 | 1928 | 2087 |

| 0 | 10850 | 0 | 0 |

| 73 | 10900 | 2254 | 2327 |

| 0 | 10950 | 13 | 13 |

| 5074 | 11000 | 15348 | 20422 |

| 1 | 11050 | 11 | 12 |

| 346 | 11100 | 4487 | 4833 |

| 2 | 11150 | 50 | 52 |

| 740 | 11200 | 6892 | 7632 |

| 0 | 11250 | 97 | 97 |

| 667 | 11300 | 14995 | 15662 |

| 2 | 11350 | 252 | 254 |

| 467 | 11400 | 15713 | 16180 |

| 13 | 11450 | 106 | 119 |

| 3716 | 11500 | 26747 | 30463 |

| 149 | 11550 | 1004 | 1153 |

| 3292 | 11600 | 19776 | 23068 |

| 155 | 11650 | 3532 | 3687 |

| 7038 | 11700 | 26367 | 33405 |

| 224 | 11750 | 2897 | 3121 |

| 6769 | 11800 | 33014 | 39783 |

| 358 | 11850 | 5811 | 6169 |

| 8434 | 11900 | 28022 | 36456 |

| 808 | 11950 | 6389 | 7197 |

| 18728 | 12000 | 53307 | 72035 |

| 3018 | 12050 | 6483 | 9501 |

| 34729 | 12100 | 25446 | 60175 |

| 15844 | 12150 | 4216 | 20060 |

| 45950 | 12200 | 15932 | 61882 |

| 8782 | 12250 | 1038 | 9820 |

| 36174 | 12300 | 7923 | 44097 |

| 9495 | 12350 | 337 | 9832 |

| 29768 | 12400 | 870 | 30638 |

| 4842 | 12450 | 11 | 4853 |

| 34403 | 12500 | 4384 | 38787 |

| 2548 | 12550 | 100 | 2648 |

| 12715 | 12600 | 443 | 13158 |

| 486 | 12650 | 1 | 487 |

| 12717 | 12700 | 260 | 12977 |

| 335 | 12750 | 3 | 338 |

| 6791 | 12800 | 89 | 6880 |

| 64 | 12850 | 2 | 66 |

| 2609 | 12900 | 287 | 2896 |

| 34 | 12950 | 0 | 34 |

| 15622 | 13000 | 6371 | 21993 |

| 27 | 13050 | 1 | 28 |

| 818 | 13100 | 18 | 836 |

| 0 | 13150 | 0 | 0 |

| 1148 | 13200 | 34 | 1182 |

| 1 | 13250 | 0 | 1 |

| 395 | 13300 | 88 | 483 |

| 0 | 13350 | 0 | 0 |

| 96 | 13400 | 2 | 98 |

| 0 | 13450 | 0 | 0 |

| 2835 | 13500 | 5189 | 8024 |

| 0 | 13550 | 0 | 0 |

| 173 | 13600 | 25 | 198 |

| 0 | 13650 | 0 | 0 |

| 157 | 13700 | 62 | 219 |

| 4 | 13750 | 0 | 4 |

| 679 | 13800 | 548 | 1227 |

| 51 | 13850 | 1 | 52 |

As we can see, there are multiple strikes at which Nifty Options are traded (75 to be precise). Assuming an expiry at each strike price and then calculating the Maximum Pain can be too tedious and time consumingin the real world. The best way is to develop an Excel sheet that would do all the labour-intensive work for you. Alternatively, one could also roughly estimate the Maximum Pain level. To do this, calculate the aggregate Open Interest for each strike price, by taking the sum of Call OI and Put OI. Then find out which strike price has the highest aggregate OI. The one that has the highest aggregate OI is the point of Max Pain. In the above table, the strike price that has the highest aggregate OI is 12000 (72035 contracts). Hence, this is the Maximum Pain level of Nifty at the time of writing (for the February series).

Below mentioned are some of the key points to remember about Maximum Pain:

-

The Maximum Pain theory states that as the expiration approaches, there is a tendency for the price of the underlying asset to gravitate towards the strike price where the largest number of option contracts will expire worthless.

-

In other words, Maximum Pain is that point (strike price) on the Option Chain that would cause the least amount of loss to option writers and the maximum loss to option buyers.

-

Usually, this happens to be the strike price where the combined open interest of Calls and Puts is the highest.

-

In order to calculate the Maximum Pain level, one will first have to visit the Option Chain monitor of the underlying. Then, one will have to assume that the underlying closes at each of the available strikes at expiration. Then, at various strikes, one will have to calculate how much money Call and Put writers are losing at each expiration level (using OI statistics) and take the aggregate of such losses for Calls as well as for Puts at each expiration level. The strike that has the lowest total loss is the point of Maximum Pain.

-

Alternatively,one could also roughly estimate the Maximum Pain level. To do this, calculate the aggregate Open Interest for each strike price, by taking the sum of Call OI and Put OI. Then find out which strike price has the highest aggregate OI. The one that has the highest aggregate OI is the point of Max Pain.

Next Chapter

Comments & Discussions in

FYERS Community

Prasad commented on March 2nd, 2020 at 9:38 PM

Very nicely explained and thanks a lot for this chapter.

Shriram commented on March 5th, 2020 at 8:51 PM

Hi Prasad, thank you!

Vijay commented on March 3rd, 2020 at 5:40 PM

I thank u for this information. It s very wonderful information. How can i get intraday strategy from this.

Shriram commented on March 5th, 2020 at 8:59 PM

Hi VIjay, thank you! You can apply each of these concepts for intraday trading as well, though you will need to monitor them closely. The concepts mentioned above are applicable for intraday and positional time frames. Indicators such as PCR and VIX can not only be used to confirm the prevailing trend but also to identify market extremes.