Cash Flow Statement as the name suggests, is the statement which provides the flow of cash, in and out of the company. Cash flow statement basically assesses the ability of the company to generate cash & cash equivalents and appropriate usage of that cash.

A cash flow statement, when used in conjunction with the other financial statements, provides information that enables investors to evaluate the changes in net assets of any company, its financial structure and its ability to affect the amounts and timing of cash flows, in order to adapt to changing circumstances and opportunities of the business. The cash that is generated by the company is classified into three segments, namely, Cash flow (a) from operating activities, (b) from investing activities and (c) Cash flow from financing activities.

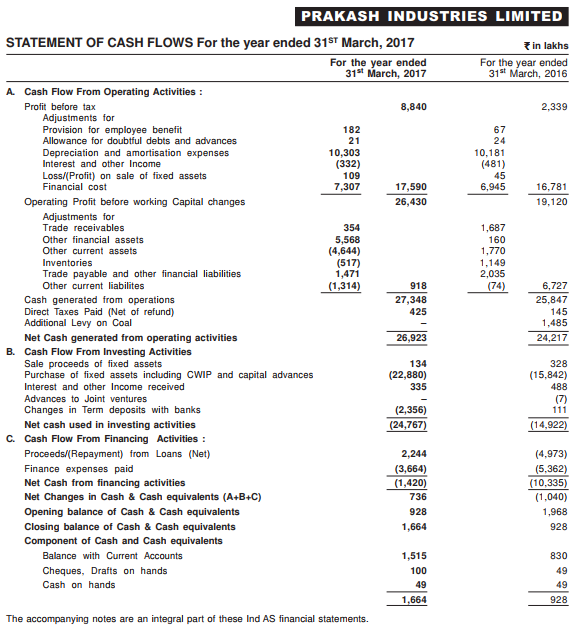

The cash flow statement of Prakash Industries Limited (Source) is provided to understand the various items as described in a typical statement.

Cash Flow from Operating Activities

Cash flows from operating activities are primarily the result of main business operations of the company, with the transactions resulting in net profit or loss. The amount of cash flows arising from operating activities indicates the ability to the company to generate sufficient cash flows to maintain the operating capability of the company, pay dividends, repay loans and make new investments without using any loans.

Cash flows from operating activities can be from various sources, like:

-

Cash receipts from the sale of goods & services, royalties, fees, commissions etc.

-

Cash receipts and cash payments of an insurance company for premiums & claims, annuities and other policy benefits.

-

Cash payments or refunds of income taxes, unless specifically categorized under other cash flow activities.

-

Cash payments to suppliers for goods and services, cash payments for employee benefits.

Generally, changes made in cash, accounts receivable, depreciation, inventory and accounts payable are reflected in cash from operations.

Cash Flow from Financing Activities

Cash flows from financing activities relate to the finances from external sources of the company involving long-term funds or capital, through issue of equity or raising of debt.

Cash flows from financing activities can be from sources like:

-

Cash proceeds from issuing shares (equity and/or preference).

-

Cash proceeds from issuing debentures, loans, bonds and other short/ long-term borrowings.

-

Cash payment of finance expenses and repayments of amounts borrowed.

-

Interest paid on debentures and long-term loans and advances.

-

Dividends paid on equity and preference capital.

Investors have to note that, based on the type of business and transaction, the classification of cash flows changes from company to company. For example, when the installment paid in respect of a fixed asset acquired includes both interest and loan, the interest portion is classified under financing activities and the loan portion is classified under investing activities. Also, same activity may be classified differently for different company. For example, purchase of shares is an operating activity for a share brokerage firm while it is investing activity in case of other companies.

Direct & Indirect Method Cash Flow Statements

When cash flows from operating activities are calculated by an indirect method and depicted in the cash flow statement, the statement itself is termed as ‘Indirect method cash flow statement’. Similarly, if the cash flows from operating activities are worked by direct method while preparing the cash flow statement, it will be termed as ‘Direct method Cash Flow Statement’.

The main difference between the direct method and the indirect method is in the cash flows from operating activities, the first section of the statement of cash flows. (There is no difference in the cash flows reported in the investing and financing activities’ segments.)

Under the direct method, the cash flows from operating activities will include the amounts for items such as, cash from customers and cash paid to suppliers. In contrast, the indirect method will show net income followed by the adjustments needed to convert the total net income to the cash amount from operating activities.

The direct method must also provide a reconciliation of net income to the cash provided by operating activities, while it is done automatically under the indirect method. Unless clearly specified as to which method is to be used, the cash flow statement is mostly prepared by the indirect method, currently done by most companies as a practice.

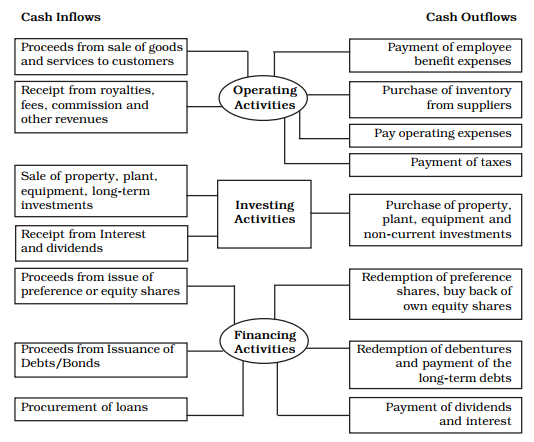

Summary of cash inflows and cash outflows due to various activities of the company (Source).

A cash flow statement’s purpose is to assist the investor in understanding the cash inflows and cash outflows of any particular company, providing a clear picture of the overall cash position of the firm. A projected cash flow statement can be prepared in order to know the future cash position of a company. By this statement, a company can come to discern the quantum of cash generated and cash expensed for various payments, thereby enabling the company to plan and arrange for the future requirements of cash.

Next Chapter

Comments & Discussions in

FYERS Community

Samika commented on April 25th, 2019 at 11:52 AM

The chapter is very well written and has helped me understand the importance of the cash flow statement to a business. I especially like the way you explained how different activities can register under different sections for different firms depending on which side of the transaction you are on.

Tethys commented on August 16th, 2019 at 12:38 PM

Hi Tejas,

I am going through your chapters again and again as it become guide for me for investing and trading. I want to know where can I get reliable figures pertaining to capital expenditure, ROE, ROCE and EPS projections.

Gopal commented on August 16th, 2019 at 12:53 PM

The best source for all financial data is always the respective Company's website, which has quarter as well as annual reports including conference call transcripts and interviews, management commentary etc.

Rest all sources are secondary in nature. Always obtain data from primary source - Company itself.

Ramya Choudhary commented on August 16th, 2019 at 12:40 PM

What is the standalone Cash Flow Statement?

Gopal commented on August 16th, 2019 at 12:57 PM

Companies which have only one entity conducting business report only one type of financial statements called the Standalone Financial Statements. Such Companies don't have income or business in any other entities.

Companies which have diversified businesses involving subsidiaries, associates etc report both - standalone as well as consolidated financials.

Hence, when checking financials of a Company it is imperative to know if the financials are standalone or consolidated.

Maximo Chauvin commented on September 8th, 2019 at 4:04 AM

Good Day, Find out how to get financing on well known products, like Gucci, Prada, and others...For more details, go to: https://youtu.be/lUxPKZtuKVA

Abhishek commented on March 8th, 2020 at 4:04 PM

Under cash flow from financing activities it is mentioned:

when we repay our borrowings for FA, principal portion is categorised under Investing whereas Interest under Financing.

Rather both Interest & Principal reapyment should be categorised under Financing activity, right?

Gopal commented on March 8th, 2020 at 7:39 PM

As mentioned in point 3 of Cash flow from financing activities, interest and loan repayments are categorized under the same.

However, there could be a specific instance when the repayment (which includes interest and principal) could be categorized differently. For eg: When the installment for a fixed asset acquired on a deferred payment basis includes interest and loan, then the interest portion is shown under financing activities while the loan portion is shown under investing activities.

For more information, refer to Ministry of Corporate Affairs website, and check Indian Accounting Standard on Statement of Cash Flows.