Continuing from the previous chapter, let us now talk about the practical application of the Top Down approach on Indian markets/sectors and stocks. For our illustration, let us take the price action in 2020 and see what we can decipher from the charts.

Stage 1: Analyzing Trends in Global Markets

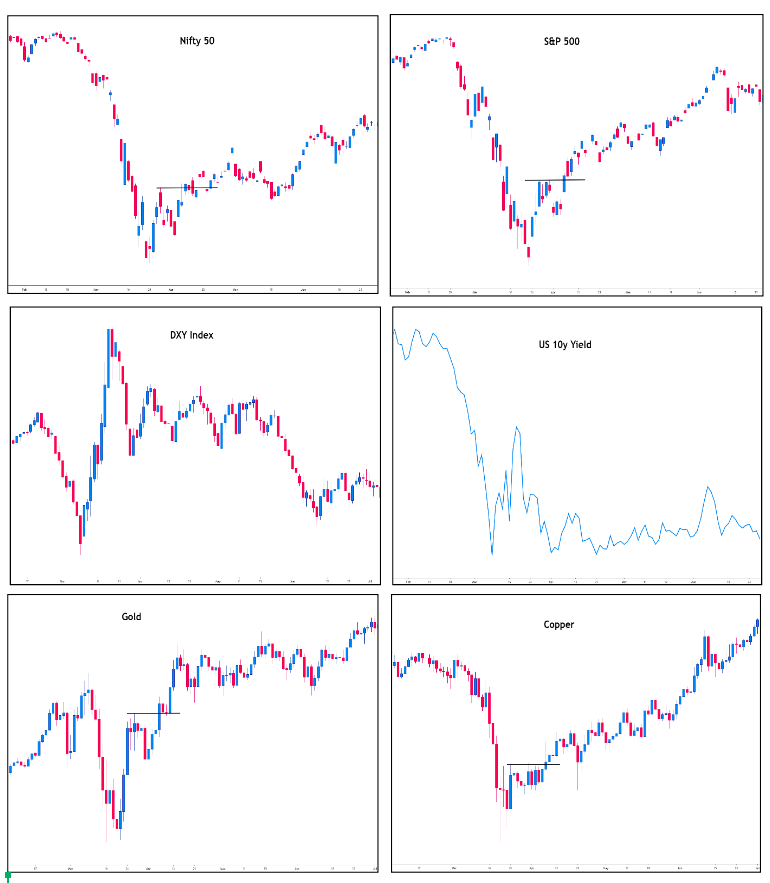

As stated previously, the first stage involves looking at the absolute as well as relative charts of major global asset classes. Let us do so now. The assets that we will consider for our illustration are the Nifty 50 index, S&P 500 index, DXY index, US 10-year Treasury yield, Gold, Copper, Crude oil, and CBOE VIX. So, let us go ahead and look at the individual charts first.

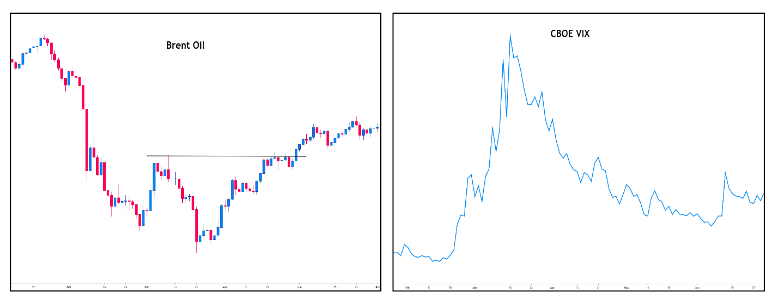

Notice the above charts. This depicts the price action during the first half of 2020. It can be seen that each of S&P 500, Nifty 50, Gold, and Copper formed a higher low – higher high sequence in early April, following a precipitous fall over the past few weeks. Crude oil prices also bottomed, albeit with an element of time lag. Meanwhile, the DXY and VIX peaked out towards the end of March, following a near vertical rise; while the US 10-year yield bottomed out in the early parts of April, following a plunge to record lows. All these intermarket and Technical factors occurring within a time span of a few days suggested that financial stresses are receding and that a recovery could get underway. Let us now look at a couple of macro ratio charts to see what they were suggesting during this period.

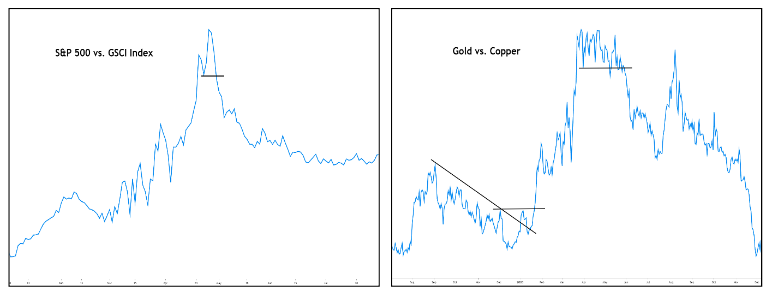

Notice above that the equity outperformance relative to commodities peaked out towards the end of April, following which commodities started outperforming. As Emerging Markets are major consumers of commodities, the reversal in this ratio can be construed as an early sign that economic conditions in EMs are reviving and that the business cycle could be turning up. This bodes well for riskier assets. Meanwhile, the breakdown in the Gold/Copper ratio in May suggested that an industrial commodity is starting to outperform a safe haven. This is again a signal of improving risk appetite. In a nutshell, the unfolding developments during April and May 2020 could be construed as a signal that riskier assets are returning in favour. Now that we have a broad overview of global markets and risk appetite, let us look at how one could have capitalised the trends that unfolded between April and May 2020.

Stage 2: Drilling down to Indian markets and Sectors

As said in the previous chapter, there are two ways of doing this. The first is the market approach and the second is the sectoral approach. You could choose any one or even both of the approaches.

Market Approach:

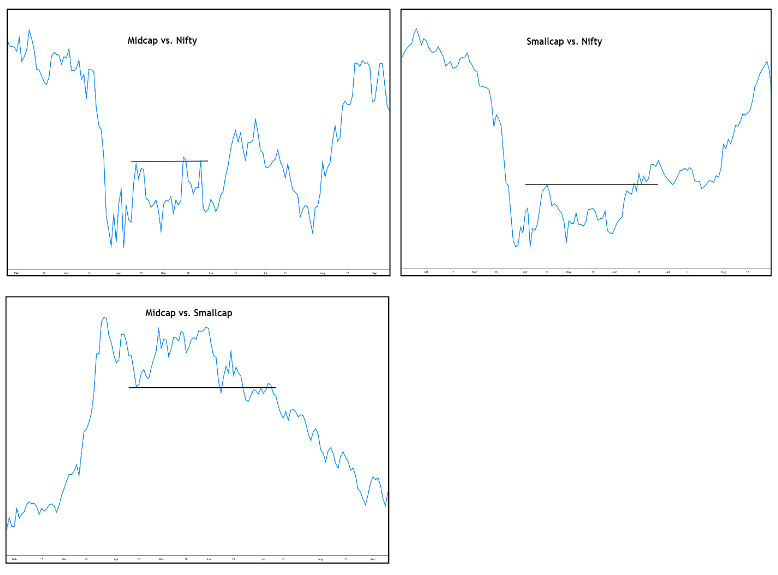

Let us look at the absolute and relative charts of Nifty Midcap 100 and Smallcap 100 index.

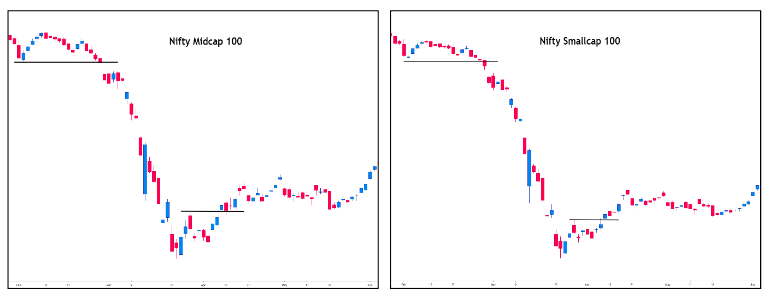

The above is the absolute price chart of the Nifty Midcap 100 index and the Nifty Smallcap 100 index. It can be seen that both the indices, following a precipitous fall, bottomed out in March and made a higher low – higher high sequence in April. This sequence essentially coincided with a similar sequence that was made by Nifty, as was saw earlier. Just by looking at the absolute chart, we can see that the swings and the trajectory of Nifty 50, Midcap 100, and Smallcap 100 are quite similar to each other. Hence, it is difficult to conclude at hindsight whether Midcaps and Smallcaps are outperforming Nifty or is it the other way around. It is for this reason that one needs to look at ratio charts as well, to understand whether one instrument is underperforming or outperforming the other and the degree of this outperformance/underperformance. Let us now look at the ratio charts.

Notice from the above charts that each of Midcap 100 and Smallcap 100 index started outperforming Nifty once the markets bottomed. Meanwhile, between Midcap 100 and Smallcap 100, see that Smallcaps started outperforming Midcaps. What do these ratio charts tell us? They tell us that Smallcaps are outperforming Midcaps, which in turn are outperforming the Largecaps. This in turn suggests that a trader should deploy a greater percent of his/her capital into Smallcaps, then into Midcaps, and finally the rest into Largecaps.

Sectoral Approach:

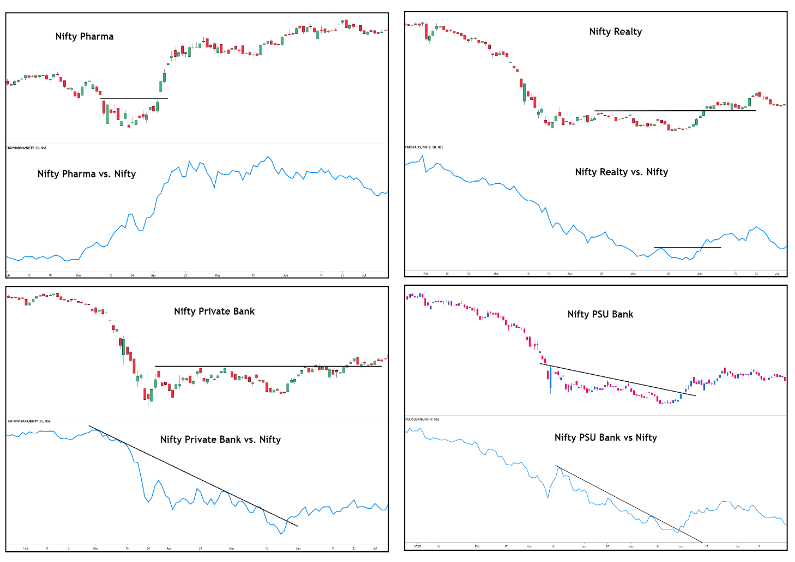

Let us look at the ratio and absolute charts of sectoral indices.

Keep in mind that Indian markets bottomed out towards the end of March 2020 and henceforth started recovering. From the above individual and ratio charts, see that Auto and Metal were the first sectors that started outperforming Nifty from early May; while IT and Pharma were already outperforming Nifty, even during the market downtrend. Meanwhile, each of Financial Services, Realty, Private Bank, and PSU Bank were laggards and started outperforming Nifty much later. On the other hand, the FMCG sector started underperforming Nifty just as other sectors were starting to outperform. What do all these charts tell us? They tell us that once the market bottomed and started recovering from April 2020, the sectors that led the market recovery were IT, Pharma, Auto, and Metal. Hence, these are the sectors that could be considered for deploying capital during the early stages of market recovery.

Stage 3: Stock selection from outperforming Markets or Sectors

Now that we are aware of the trends that were unfolding across the global markets as well as across the Indian markets and sectors between April and May 2020, the next stage is to start screening stocks, depending on the approach chosen - market or sectoral. But before proceeding towards discussing each of these, let us first talk about an important concept called Position Sizing.

Position Sizing:

As the name suggests, Position Sizing refers to deciding the size of each position within a portfolio of securities. Some of the key objectives of Position Sizing are:

- To determine the number of stocks to buy

- To manage portfolio risks efficiently and effectively

There are several ways in which a trader can choose Position Sizing depending upon the capital deployed and the portfolio risks that the trader is willing to take. In here, we will discuss two widely used methods of Position Sizing.

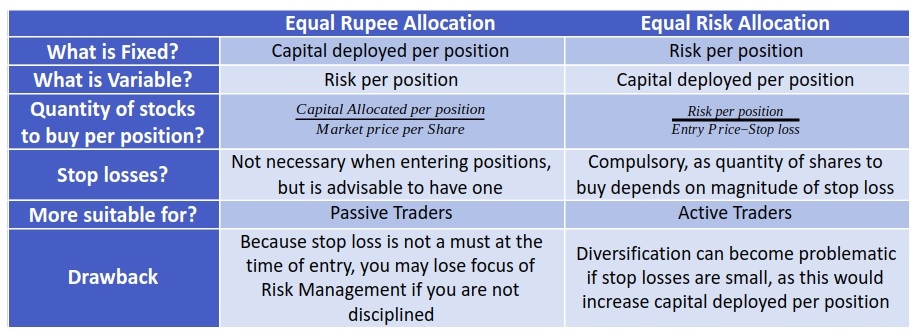

Method 1: Equal Rupee allocation

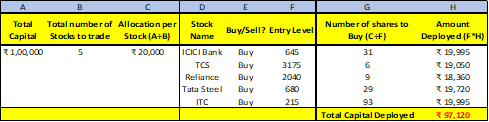

Under this method, equal money is allocated to each position within a portfolio. How much money is allocated for a position depends on several factors, such as a trader’s objective, capital size, extent of diversification to be achieved etc. Let us take a simple example. Let us assume that a trader has a capital of ₹1 lac and has decided to deploy ₹20,000 per stock. Based on this, a trader would be deploying his capital in 5 different stocks (₹1,00,000/₹20,000). As it may not always be possible to deploy exactly ₹20,000 in each stock (because the market price per share may not be exactly divisible by ₹20,000), small differences are acceptable. Also, in this case, see that a trader will not be able to buy a stock that is currently selling for more than ₹20,000 per share (such as MRF and Page Industries). If a trader intends to achieve greater diversification, he must deploy lesser capital per position, such as ₹10,000 instead of ₹20,000, and vice versa.

Let us take a simple example now. Let us assume that we have looked into the chart of ICICI Bank and expect it to rise going forward. At the prevailing price of ₹645 per share and an allocation of ₹20,000 per position, a trader would be able to buy 31 shares of ICICI (₹20,000/₹645, rounded down to the nearest integer). So, the total capital invested in this position is ₹19,995 (₹645 * 31). Coming to the risk management part, the trader must now decide the stop loss for the trade. Keep in mind that the stop losses chosen must not be random but rather logical and based on the past price action. Let us assume that the trader sees an important support converging near ₹597 and likewise decides to place a stop loss at ₹595. In case the stock moves contrary to expectations and hits ₹595, the position would be exited, and the trader would suffer a loss amounting to ₹1,550 ((₹595 - ₹645) * 31). In a similar way, the trader would deploy ₹20,000 in each of the other 4 stocks.

Below is a sample illustration of Portfolio sizing done using Equal Rupee approach. Total capital deployed is ₹1 lac, which is then evenly distributed across 5 different stocks (₹20,000 per position). Notice how the capital deployed per stock is nearly identical.

Method 2: Equal Risk allocation

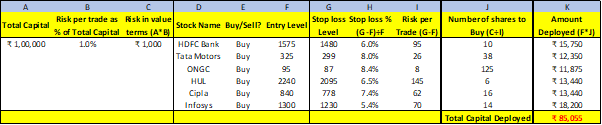

Under this method, equal risk is allocated to each position in the portfolio, while the amount of capital deployed in any one position varies depending upon the stop loss chosen for each stock in the portfolio. Now contrast this method to the previous, in which equal capital was allocated to each position. In this method, the risk per position as a percent of the total capital deployed is fixed. Ideally, this risk should not exceed 2% of the total capital, as doing so would significantly increase portfolio risks in case of adverse market movements. Instead, the risk should ideally be capped at 0.5% or 1% of the total capital. For our illustration, let us assume that the total capital to be deployed is ₹1 lac and that the risk the trader is willing to take per position is 1% of the total capital. This turns out to be ₹1,000 per position (1% of ₹1,00,000).

Let us take the example of ONGC. After reviewing the chart, let us assume that the trader expects the stock to rise going forward. Let us assume that he/she wants to buy at the prevailing price of ₹95 per share. From the chart observation, the trader is of the opinion that his/her bullish view would stand negated in case the price drops to ₹87.50. Hence, he/she is willing to place a stop loss at ₹87. So, the risk per share is ₹8 (₹87 - ₹95). Given that the trader has decided to cap his/her losses to ₹1,000 per position, the number of shares of ONGC that he/she can buy, such that the loss amounts to exactly ₹1,000, is 125 (₹1,000 ÷ 8). See that in case the stop loss is hit, the trader would exit the position at ₹87 and suffer a loss of ₹1,000 ((₹87 - ₹95) * 125). In a similar way, you would cap your risk to ₹1,000 per position for each of the other stocks that you have bought. Remember, the total capital deployed at any point would be ₹1 lac or less.

Below is a sample illustration of Portfolio sizing using Equal Risk approach. Total capital deployed is ₹1 lac and risk per trade is 1% of the total capital.

Before jumping back to the Top Down approach, let us summarize the key differences between the two Position Sizing methods discussed above:

Now that we understand the basics of Position Sizing, let us come back to our topic of discussion, stage 3 of the Top Down approach.

Market Approach:

If market approach is chosen, the trader must decide on the allocation that would go into smallcaps, midcaps, and largecaps. For our example, based on our interpretation from Stage 1 and 2, let us select a 40%, 35%, and 25% allocation to smallcaps, midcaps, and largecaps, respectively. Let us also assume the total deployable capital is ₹4 lacs. Out of this, ₹1,60,000 would go into Smallcaps, ₹1,40,000 into Midcaps, and ₹1,00,000 into largecaps. To decide on position sizing within each of Smallcaps, Midcaps, and Largecaps, a trader could resort to one of the two methods discussed above or implement his/her own position sizing strategy. For our case, let us assume that the trader has decided to deploy ₹20,000 per position in each of the three markets. That means the trader would be buying 8 smallcap stocks, 7 midcap stocks, and 5 largecap stocks, for a total of 20 stocks. Now that the allocation has been decided, the trader must scan all the stocks (250 in total) from each of the three indices, with the objective of selecting 8 smallcap, 7 midcap, and 5 largecap stocks that he/she believes would perform the best going forward.

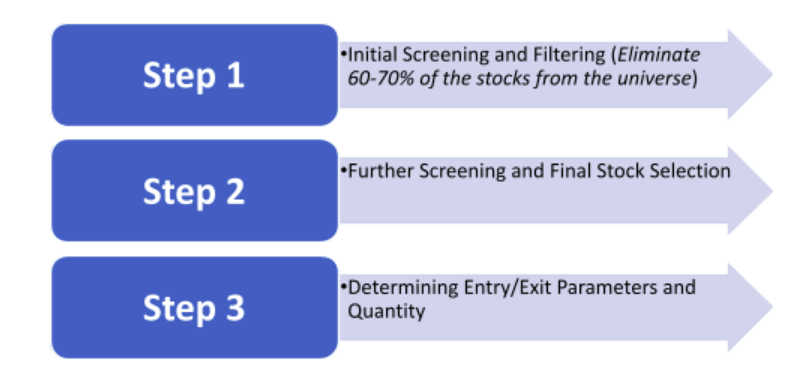

For stock screening and filtering, one could use fundamental parameters, technical parameters, quantitative parameters, or a combination. There are various ways in which stocks can be screened, filtered, and selected. One such example is to deploy a three step approach for filtering and selecting the stocks to buy, as follows:

-

Step 1 (Initial Screening and Filtering): Initially, one could start by filtering out those stocks from the chosen universe that do not fit in the selection criteria. What could this stock elimination criteria be? Well, that varies from traders to traders. A few examples include eliminating those stocks from the universe that are trading below their 20-day MA, those that are priced above a certain level (say ₹5,000 per share), those that are less liquid etc. Several such criteria could be deployed to remove ineligible stocks. Once the ineligible stocks are out, the trader must then quickly scan the charts of each of the remaining stocks from the respective index and filter out those that are underperforming the markets and are not looking promising. The objective of this step is to eliminate at least 60-70% of the stocks from the universe, so that we are left with just a few handful of good stocks.

-

Step 2 (Further filtering and final stock selection): Once the stock list has been narrowed down, again look into the charts of all the remaining stocks, but this time in a much more detailed manner, including looking at the ratio charts of a stock versus the index of which it is a part of. If you are confused of deciding which one stock to select among two or three, you could even look at the ratio chart of one stock versus another stock from the same index, so as to eliminate the one that is showing weak relative strength. The objective of this step is to eliminate all the remaining stocks and retain only those that would be on your final buy list.

-

Step 3 (Determining Entry, Quantity, Stoploss, and Target): Once the final stock selection is done and you have decided which of the 8 smallcap, 7 midcap, and 5 largecap stocks to buy, the final step is to identify the entry level for each trade, quantity of each stock to be purchased, the stoploss for each trade, and the target price for each trade. Keep in mind that the risk to reward ratio must be attractive before entering the trade.

To reiterate, shown below is a sample three-step process of how one could filter and select stocks from a universe:

Sectoral Approach:

On the other hand, if the sectoral approach is chosen, the trader must decide on the allocation that would go into IT, Pharma, Auto, and Metal sector. For our illustration, let us allocate 25% to each sector. Let us also again assume the total deployable capital to be ₹4 lacs. This means ₹1 lac will go into each of the four sectors. For position sizing, let us assume that the trader has decided to deploy ₹20,000 per position in each sector. That means the trader would be buying 5 stocks from each sector, for a total of 20 stocks. Now that the allocation has been decided, we must scan all the stocks, sector wise (50 in total), with the objective of buying 5 stocks each from the IT, Pharma, Auto, and Metal space. Again, the trader could use the three step approach mentioned above to screen, filter, select stocks, and define the entry and exit criteria for each of the five stocks from each of the four sectors.

Stage 4: Monitoring the portfolio and ensuring proper risk management

As said in the previous chapter, the Top Down approach does not end once each of the above three stages are complete. In fact, once a trader has purchased and created a portfolio of stocks, just half of the work is complete. The other half is to repeat each of the previous three stages, as follows:

-

Regularly monitor the overall markets (global as well as domestic, broader as well as sectoral, on absolute as well as relative charts). If there is a material change in market conditions, you may need to make changes to your portfolio to reflect those changes. For instance, if markets are moving into a defensive mode from a risk-on mode, you may need to increase allocation to defensive stocks and sectors.

-

Constantly monitor the ratio charts of one market (such as Midcap and Smallcap) versus the benchmark (Nifty) or one sector versus the benchmark. This would help in tracking the relative trends and make changes in the composition of the portfolio when there is a material change in relative trends (such as break of an important trend line, support, or resistance etc).

-

Closely monitor the price trends of stocks in which capital has been deployed and strictly adhere to risk management principles. If a position gets stopped out, exit without a second thought, and add a new stock in its place that meets your screening and selection criteria.

-

Keep scanning stocks from within your universe to identify stocks that are gaining strength, both individually and relatively. If necessary, you may even remove an existing stock from your portfolio that is constantly underperforming the markets and add a new one in its place that is showing greater strength and momentum or has given an important breakout.

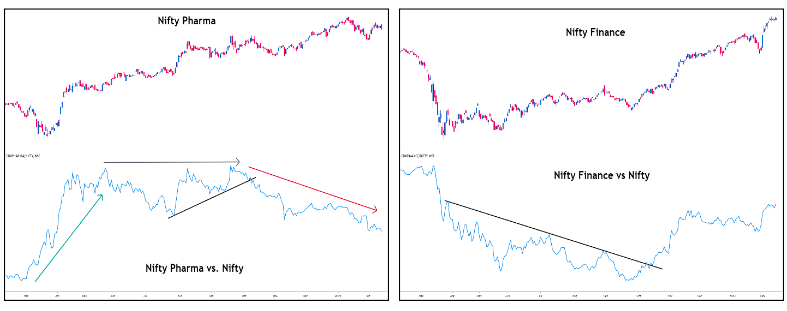

As an example, look at the two charts below:

If you recollect, in Stage 2, we saw Pharma as one of the four sectors that were leading the markets higher and accordingly chose to allocate a certain percent of the total capital to pharma stocks. However, see above that the Pharma outperformance relative to Nifty lasted only till May 2020. Between June and September 2020, see that pharma performed roughly at par with Nifty. However, from October 2020, see that Pharma started underperforming Nifty. On the other hand, now look at the other chart depicting Nifty Financial services index. After months of underperformance, see that the financial services sector finally caught up and started outperforming Nifty from October 2020.

With Pharma starting to underperform from October and the financial sector starting to outperform from the same period, a trader could have rotated out of Pharma stocks and moved into financial services stocks. This is how you rotate your capital from sectors that are underperforming to those that are outperforming. This is a part of Stage 4, wherein you will actively reshuffle your portfolio as and when the need arises.

Let us conclude the chapter by showing a flow chart of the Top Down Approach, using Technical Analysis as a primary decision-making tool.