Fundamental analysis is an indispensable method and a critical foundation, adopted by most investors for long term investing. This type of analysis has to be detailed and, it is imperative that, each investor gets the much needed understanding of all aspects before selecting any particular company, with conviction, for investment. The two facets to any fundamental analysis include quantitative analysis as well as a qualitative analysis, which together, encompass most of the basic queries to be answered, before taking a final investment decision.

Quantitative and qualitative aspects of the fundamental analysis components can be classified under:

-

Industry Classification & Analysis

-

Financial Statement Analysis

-

Management Analysis

Industry Classification

Continuing from the earlier section on ‘Introduction to Economic Factors’, where the various macro/micro factors affecting the business environment in general have been highlighted, an overview of a specific industry is also essential. A deeper understanding of the prevailing growth prospects, demand-supply cycle, government policies and regulatory mechanisms, peer comparison, price realizations along with the SWOT, will certainly provide the direction for an appropriate sector selection.

Though most of the industries are broadly classified under agriculture, manufacturing or services, a detailed classification can result in more than a 100 possible sectors that influence the economic growth. Similarly, if classified on the basis of themes, there are a lot of sectors which incorporate either a consumption theme or a manufacturing theme export oriented theme and so on. During the sector selection, understanding of the macro factors will help in identifying the headwinds and tailwinds available for each sector, thereby highlighting the industries and companies whose business prospects can be affected positively or negatively in terms of cycles. This classification can be based on the growth, value, cyclical or defensive nature of the businesses.

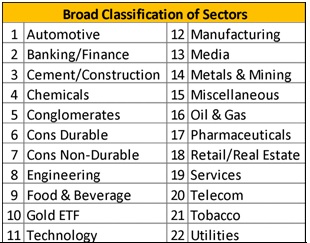

Out of the BSE stock exchange-listed universe of close to 7000 companies, most of the stocks are collated under a specific Industry or a specific sector for ease of understanding the business and for peer comparison. For eg: For understanding at a basic level, Moneycontrol provides a broad classification of sectors under the following 22 categories.

This is a very rudimentary classification, where each sector might have an average of 400 stocks under each category, ranging from less than 10 companies under the Gold ETF category to more than 1000 companies under the Banking/Finance category.

This type of categorization is not very helpful in understanding the economic impact in detail, as many companies are categorized under the same sector but is useful at a primary level. For eg: An interest rate change would have the highest impact on the banking / finance related sector, while it would have a lesser impact on media sector. An environmental regulation, banning a specific product like petcoke will have an impact only on cement/construction, chemical related sectors, but would not have any impact on the technology, banking or automotive sectors.

In this manner, a novice investor can learn and understand, to relate the sector categorization and impact of the business environment at a general level. However, for a more advanced investor, who has the understanding of the macro and micro factors and their effects on each sector, a detailed industry classification is provided.

For eg: Moneycontrol classifies BSE listed stocks into 112 sectors for ease of understanding and comparison. Though many companies have diversified businesses, each company’s major business objective is considered for this classification (source). This is one of the most comprehensive classifications provided to aid a well-informed investor to identify the appropriate industries for sector selection.

Though this classification has its own cons, it offers a much better, in-depth view of the various sectors / industries conducting business and the companies classified under each segment. The 112 sectors classification is as given below:

This industry classification is essential for relating the impact of the macro and micro economic factors driving the business growth of the specific segments of the economy. While a regulation or a policy change or decision affects a particular industry, it is not essential for all the companies in that industry to be affected in a similar manner.

For eg: Many companies are classified under the computer industry, which in-turn is subdivided as computer software, computer hardware, computer software – training, computer software – medium and small. Hence a variation in the exchange rate might not impact all these subdivided segments in a similar manner, as only a few companies in each industry might have exports/overseas businesses, while most companies would be operating as a domestic business only, with no impact.

Another good example would be the pharma industry where the regulatory practices and guidelines laid down by the USFDA are considered to be extremely tough. At the same time, a company with less exports to US and more concentration to the UK/European market would not be affected in a similar manner.

Industry Analysis

After understanding the industry classification, the next step would be to conduct an industry analysis. There are many concepts to understand an industry and the analysis consists of using these concepts to gain sufficient knowledge about each industry, which will result in a comprehensive research till the identification of a particular company.

The most commonly used concepts include the Michael Porter’s Five Forces Theory, 5C Analysis, PEST Analysis, SWOT Analysis etc. The following section will explain the important concepts in detail, which will result in a comprehensive analysis, leading to identification of the right companies in a sector.

Five Forces Theory

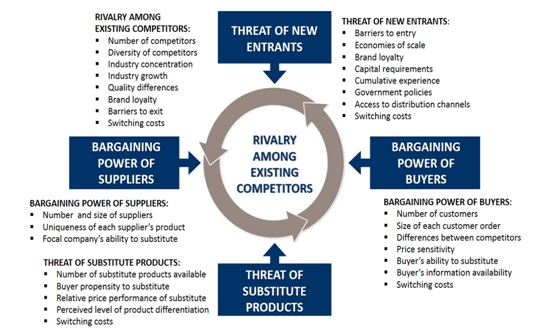

Many investors would have been introduced to the concept of Michael Porter’s Five Forces Theory to understand the industry structure, before concluding an analysis that is reflective of the past, present and future of a particular industry. Michael Porter, a Harvard Business school professor developed a framework that models an industry influenced by five forces in his book "Competitive Strategy: Techniques for Analysing Industries and Competitors". The five forces that govern an industry are as follows:

-

Threat of New Entrants

-

Threat of Substitute Products

-

Bargaining Power of Suppliers

-

Bargaining Power of Buyers

-

Industry Competition

A self-explanatory illustration providing the five forces and the necessary queries to be addressed for understanding an industry are given below:

As a framework, five forces analysis determines the competitive landscape and attractiveness of a market for industry analysis and development of a business strategy. This analysis will help in understanding the operating perspectives of any company as part of an industry.

5C Analysis

This concept’s usage is preferred for analysing the market environment. It is to gain information on the internal, as well as macro and micro environmental factors within the business landscape. The 5C’s are Company, Customer, Competitors, Collaborators and Climate.

Addressing the relevant questions under each ‘C’ will provide sufficient understanding of a company.

-

Company: How successful is the product portfolio? What is the company’s perception in the industry? Are employees in sync with the company’s culture, goals and expectations?

-

Customers: Who are the target customers and what is the market size? Is there a consistent growth in the customer base? What is the USP of the company’s product or service? Is there a continuous change in the sales trends? Is there is a change in the buying process?

-

Competitors: Has the competitive landscape been defined? What are the competitors’ products, market shares in the market? What are their strengths and weaknesses?

-

Collaborators: Who are the suppliers, distributors, channel partners? Is the support adequate enough in growing the business? How does the stability of their business affect the company?

-

Climate: What are the effects of governmental policies and regulations? What are the dependent economic factors? Is the impact of technology high and relational to the demand for product and services? Is a higher technology adaptation necessary for a competitive advantage?

In this manner, there are quite a few questions to be addressed in order to understand the functioning of a company. A properly accomplished 5C analysis can highlight the internal as well as external factors affecting the business prospects of a company, thereby determining the sustainability of the business.

SWOT Analysis

While a five force analysis is specifically geared to focus on the industry in which a company operates, SWOT analysis – Strengths, Weakness, Opportunities, Threats - focuses primarily on the company itself. The strengths and weaknesses of a company are internal in nature, under the control of that particular company and analysed relative to the whole industry, while the threats and opportunities are external factors affecting the company, analysed for impact within the industry.

A typical template of a SWOT analysis is given below:

|

Strengths Capabilities, competitive advantage, R&D/ Innovation, marketing & distribution network, product portfolio, low cost/high quality manufacturing capabilities, brands & patents ,excellent financial & operating leverages. |

Weaknesses Operational and financial risk, capacity & capability ssues, concentrated customer segment due to limited product portfolio, geographical disadvantage, low margin products and services. |

|

Opportunities Industry trends, higher market growth, geographical expansion, target markets, licensing deals, partnerships and alliances, market conditions/customer needs, competitor’s issues, mergers and acquisitions. |

Threats Subject to periodic & intense regulatory scrutiny, technological changes, economic conditions, changing consumer trends, low entry barriers, currency fluctuations, technological changes. |

Some of the queries that are expected to be addressed during a SWOT analysis are as follows:

-

Strengths: What does the company do well consistently? What are the factors that are under the control of the company? What is the competitive advantage? How are company’s products and services superior to competitors in the market? Is the company in a monopolistic business, with high entry barriers?

-

Weakness: Where is the company underperforming? What are the hindrances for the company to succeed? Is this temporary in nature or a continuing obstacle? Are the operational or financial limitations like high cost structure, cost of funds preventing the company from achieving its targets?

-

Opportunities: What are geographies and untapped markets available? Where is the potential for new business? What are the new applications possible with the current portfolio? Can the company take advantage of any market trends? Can the introduction of a new technology provide competitive or a first mover advantage?

-

Threats: What are the deterrents for business growth? Are low entry barriers introducing substitute products at lower prices into the market? Which external factors like political, technological, social or economic are and can cause issues? What are the policy decisions and regulations that can affect the business continuity?

Though most of these questions need to be addressed by that particular company, an investor’s understanding of these queries can be, just that bit of additional knowledge which can work in favour of investing in the company. Hence, spending time in understanding the company’s positioning would result in excellent and consistent rewards to shareholders over longer time periods.

PEST Analysis

As described in the last ‘C’ of the 5C Analysis, PEST Analysis relates to the business environment from various political, economic, social, and technological perspectives. This method provides a comprehensive analysis of external factors that could affect every company. A self-explanatory illustration encompassing some of the issues is given below.

The queries to be addressed for completing a PEST analysis include the following:

-

Political: What laws and regulators affect business and consumers? What’s is the impact assessment of trade regulations, labour laws, and taxation? How stable are the overseas geographies in which the company sell products, has local hires etc.?

-

Economic: Effect of interest, inflation, tax and exchange rates on the company? What are the local business cycles in relation to the overall economic growth?

-

Social: What lifestyles and attitudes affect the buying habits of your consumers? What are the current and changing demographics of the customers?

-

Technical: What patents, innovations and licenses can support the company? Is technological change helpful to the company in its competitive advantage? Which manufacturing trends can increase your production levels or drive down costs?

In recent times, legal and environmental analyses have also been added to PEST to provide additional perspectives of civil and environmental implications of allowing a business to function in a particular geography.

All these types of analyses are called Situation Analyses as they aim to provide a clear and objective view of the business, organizational capabilities, customer segments, industry trends, competitors and a particular company’s position relative to that industry.

Financial Statement Analysis

After a thorough industry analysis, the next step involves the financial analysis of a company through the usage of the three financial statements – P&L, balance sheet and cash flow. Financial Analysis is the process of critical evaluation of the financial data provided in the financial statements, so as to assist the various stakeholders to understand and make necessary decisions. Along with the detailed analysis, it is imperative to interpret the results in a manner which can provide clarity on the operational performance and financial health of the company.

Different stakeholders like promoters, investors, shareholders, lenders, equity analysts etc. have their own analysis and interpretation of the financial information. The nature of analysis will differ depending on the end use of each stakeholder. Also, a Cross Sectional Analysis – comparison with other companies is different from a Time Series Analysis – comparing the company’s own performance over various time periods.

It is important to note that the financial analysis can be done only when the same accounting principles are used in preparing all the statements. Any deviation or change in accounting principles can distort the analysis and the resulting trends.

There are five commonly used techniques of financial analysis and they are detailed as follows:

Comparative Statement Analysis

Also termed as horizontal analysis, the comparative statements show the profitability and financial position of a firm for different periods of time in a comparative format, to provide an indication of the change during two or more periods of comparison. It is usually accomplished with two financial statements - the balance sheet and profit & loss statement which are prepared in a comparative format and declared to the stock exchanges as public information. Comparative figures indicate the trend and direction of financial position and operating results.

Template for comparative statement analysis:

|

|

Column 1 |

Column 2 |

Column 3 |

Column 4 |

Column 5 |

|

S.No |

Parameters |

Financial Year 1 |

Financial Year 2 |

Absolute Increase (+) Decrease (–) |

Percentage Increase (+) or Decrease (–) |

|

1 |

Sales |

Rs. |

Rs. |

Rs. |

% |

|

2 |

Operating Profit |

|

|

|

|

|

3 |

Profit before Tax |

|

|

|

|

|

4 |

Net Profit |

|

|

|

|

|

5 |

Earnings per Share |

|

|

|

|

Steps for comparative statement analysis:

-

List out absolute values in Rs. relating to two financial years (as shown in columns 2 and 3)

-

Compute change in absolute values by subtracting the first year (Column 2) from the second year (Column 3) and indicate the change as increase (+) or decrease (–) in column 4.

-

Calculate the percentage change as input for column 5, using the formula:

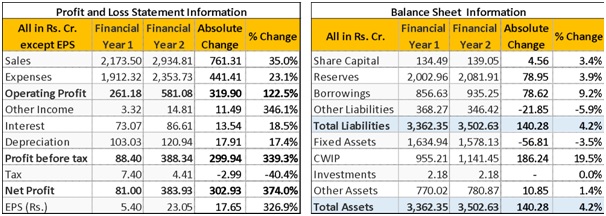

For eg: Consider a company which has declared its annual results at the end of the financial year in March and using the previous year’s results, calculate the absolute change as well as the percentage change in the parameters. This helps us understand the current year’s change in the various profit and loss items as well as balance sheet items of the same company, with respect to previous year’s performance.

.jpg)

For eg: Consider a company which has declared its annual results at the end of the financial year in March and using the previous year’s results, calculate the absolute change as well as the percentage change in the parameters. This helps us understand the current year’s change in the various profit and loss items as well as balance sheet items of the same company, with respect to previous year’s performance.

In simple terms, it is a year-on-year comparison of the annual results. The same analysis can be extended for comparing the quarterly results of a profit & loss statement alone, to observe the change in the financial parameters at an absolute as well as at a percentage level.

Common Size Statements

Also termed as vertical analysis, the common size statements indicate the association of different parameters of a financial statement, by expressing each item as a percentage of a common parameter. For eg: Operating profit margin, net profit margin etc. The percentage thus calculated can be easily compared with the results of corresponding percentages of the previous year or with some other companies in the same sector. Common size statements also referred to as Component Percentage Statements. These statements also help us in comparing the operating and financial parameters of two companies of different sizes in the same industry.

Template for common size statements:

|

|

Column 1 |

Column 2 |

Column 3 |

Column 4 |

Column 5 |

|

S.No |

Parameters |

Financial Year 1 (FY1) |

Financial Year 2 (FY2) |

All Parameters as a % of Sales |

All Parameters as a % of Sales |

|

for FY1 |

for FY2 |

||||

|

1 |

Sales |

Rs. |

Rs. |

% |

% |

|

2 |

Operating Profit |

|

|

|

|

|

3 |

Profit before Tax |

|

|

|

|

|

4 |

Net Profit |

|

|

|

|

Steps for common size statement / analysis:

-

List out absolute values in Rs. relating to two financial years (as shown in columns 2 and 3)

-

Compute % change of each parameter with respect to sales for column 4 – meaning, divide all parameters of FY1 by the sales of FY1; Repeat the same process for column 5, but with parameters of FY2.

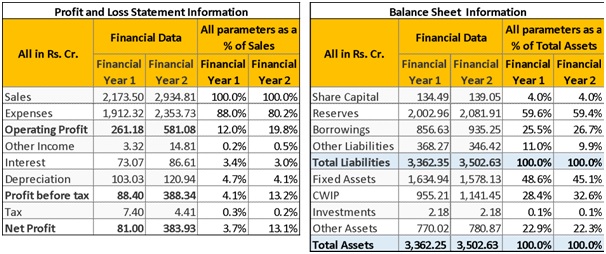

For eg: Considering the same company’s financial data for two consecutive years and evaluating all parameters of the profit & loss account with respect to one single parameter – Sales, will provide us with an understanding of the change in all parameters with respect to sales during the two years.

Similarly, considering all the parameters of a balance sheet and evaluating with respect to one single parameter – Total Assets, will provide the change in the various items of the balance sheet.

Common size statements are useful in intra-company comparisons over different years, as well as in performing inter-company comparisons for the same year or for several years.

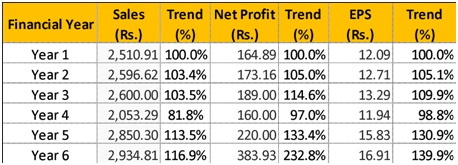

Trend Analysis

As the name suggests, trend analysis is a technique of analysing the operational results and financial position over a series of quarters or years. Using the previous years’ data of a company, trend analysis can be done to observe the percentage changes over time in the various parameters like sales, cost of goods sold, operating profit, net profit etc. The trend percentage is the percentage change, in which same item of different years is compared to the same parameter in the base year. By analysing the trends, an investor can identify if a particular parameter is showing either an upward trending or a downward trending movement or if is relatively constant without considerable change.

Formula for trend analysis:

Template for trend analysis:

|

Financial Year |

Sales |

Trend (%) |

Net Profit |

Trend (%) |

|

Year 1 |

Base Year |

100% |

Base Year |

100% |

|

Year 2 |

Rs. |

Year 2 Sales/ Base Year |

Rs. |

Year 2 Profit/ Base Year |

|

Year 3 |

Rs. |

Year 3 Sales/ Base Year |

Rs. |

Year 3 Profit/ Base Year |

|

Year 4 |

Rs. |

Year 4 Sales/ Base Year |

Rs. |

Year 4 Profit/ Base Year |

|

Year 5 |

Rs. |

Year 5 Sales/ Base Year |

Rs. |

Year 5 Profit/ Base Year |

For eg: If the sales in the base year is considered as 100%, then the relative change in sales each year as compared to the base year, will help us understand the trend of sales growth. Similarly, other financial parameters can be computed to understand the trends over a period of time.

Simply put, trend analysis indicates the change of the same parameter over a period of time.

Ratio Analysis

The most widely used analysis among stakeholders is the ratio analysis and It describes the significant relationship existing between various items of a balance sheet and a profit & loss statement of the company. The ratio analysis incorporates many sub divisions and are categorized for the purpose of understanding the profitability, liquidity, efficiency, solvency positions of a company.

Classification of ratios is done in two ways - traditional classification and functional classification.

Traditional Classification: The traditional classification has been done on the basis of financial statements, to which the determinants of ratios belong, which are sub classified as:

-

Profit & Loss statement ratios, where the ratio is computed using two parameters from the statement of profit and loss only

-

Balance Sheet ratios, where the ratio is computed using parameters from the balance sheet only

-

Composite ratios, where the ratio is computed with one parameter from the profit and loss statement and another parameter from the balance sheet

Functional Classification: The functional classification was done to highlight the impact of continuous operational performance on the financial situation of the company at all times. The most commonly used ratios are:

-

Liquidity Ratios - computed to measure the liquidity position, indicating a company’s ability to pay off its short term debts. Eg: current ratio, acid test ratio.

-

Solvency Ratios - computed to determine the solvency of business through its ability to meet its long term contractual obligations towards stakeholders. Eg: debt equity ratio, total assets to debt ratio, proprietary ratio and interest coverage ratio.

-

Activity (Turnover) Ratios - computed for measuring the efficiency of operations of business based on effective utilisation of resources. Eg: Inventory Turnover, Trade Receivables Turnover, Trade Payables Turnover, Working Capital Turnover, Fixed Assets Turnover and Current Assets Turnover.

-

Profitability Ratios - computed for measuring the profits generated by the company in relation to the revenues or capital employed in the business. Eg: Gross Profit ratio, Operating ratio, Net Profit Ratio, Return on investment (Capital employed), Earnings per Share, Book Value per Share, Dividend per Share and Price/Earnings ratio.

A few examples of the ratios and their calculation, significance and impact are provided for ease of understanding.

Liquidity Ratio:

-

Current Ratio:

-

Calculation: Current Assets/Current Liabilities, where current assets include current investments, inventories, trade receivables, cash & cash equivalents, short-term loans & advances and other current assets such as prepaid expenses, advance tax and accrued income, etc. Current liabilities include short-term borrowings, trade payables other current liabilities and short-term provisions.

-

Significance: Provides a measure of degree to which current assets insure against current liabilities. The excess of current assets over current liabilities provides a measure of safety and the ratio should neither be very high or very low.

-

Impact: A very high current ratio is not a good sign, implying heavy investment in current assets, reflecting underutilisation/ improper utilisation of resources. A low ratio can compromise the business and risk its ability to pay the short-term debts when due. A persisting situation can affect the credit worthiness of the company adversely. Normally, the preferred ratio limits are 2:1.

Solvency Ratio:

-

Debt to Equity Ratio:

-

Calculation: Long term debts/Shareholder’s funds, where shareholder’s funds are equity share capital + preference share capital + reserves & surplus + money received against share warrants.

-

Significance: A low debt equity ratio reflects more security, whereas a high ratio, is considered risky, as it may strain the company in meeting its obligations to lenders. However, from the perspective of the promoters, greater use of debt may help in ensuring higher returns if RoCE > WACC.

-

Impact: Measuring the degree of indebtedness of a company, the ratio provides a perspective to long-term lenders on debt security. Hence, if the debt component of the total long-term funds deployed is small, lenders feel more secure. From security point of view, capital structure with less debt and more equity is considered favourable as it minimises the chances of bankruptcy. A debt to equity ratio of 1.5:1 is considered to be appropriate, but can vary from industry to industry.

The various financial ratios detailed in the earlier sections assist in analysing the financial information, and the interpretation of that analysis can provide sufficient credence, to extrapolate similar trends as future growth and possible company performance.

Simply put, ratio analysis is a technique which involves regrouping of data by application of arithmetic computations, thereby providing information, to compare the company’s operational and financial health with established benchmarks.

Cash Flow Analysis

Cash flow refers to the analysis of actual flow of cash into, and out of a company during the time periods of consideration. The flow of cash into the business is called as cash inflow or positive cash flow and the flow of cash out of the firm is called as cash outflow or a negative cash flow. Net cash flow is the difference between the inflow and outflow of cash into the company.

Cash flow statement is prepared to project the method in which the cash has been received and has been utilised during an accounting year. It depicts a true picture of the sources of cash receipts and also the purposes for which the payments were made during the period. Hence, the cash flow statement summarises the changes in cash position of a company between two accounting periods.

Cash flow statement and analysis is explained in detail in the section - Understanding Your Company.

Summary

Investing in direct equity, through the stocks of a publicly listed company on the stock exchange, is a methodical process. All the sections highlighted during the course of this knowledge base, are geared towards providing a good understanding of the associated financial terminology and in helping a layman prepare for an investment decision like an intelligent and methodical investor.

Investing commences with the understanding of economics and business scenario in general, and hence the Introduction to Economic Factors section suitably addresses the basic concepts, terms and the significance, role and impact of each of the macro and micro economic variables on the country, on each industry and the resulting effect on each company.

Understanding Your Company section caters to simplifying the numerous public disclosure documents provided by the company - in terms of the profit & loss, balance sheet, cash flows, shareholding pattern disclosed periodically – quarterly as well as on an annual basis. The annual report is a document providing the management’s thought process, strategies, highlights of the current operational and financial performance and expectations of the near future going ahead. This document acts as an information sharing and marketing tool for every company.

The Introduction to Financial Analysis section addressing the various mechanisms and theories that can be put to use to discern the effects of a particular regulation or a decision enforced by the government as well as the individual company. The various analyses ascribed in this section help an individual investor as well as other stakeholders to perform basic arithmetic computations related to a set of financial statements.

Most of the commonly computed ratios are highlighted in the Financial Ratios & Analysis section, detailing the various profitability, solvency, liquidity, activity and valuation ratios. These ratios are aimed at assisting the investor in taking an informed decision based on the historic and current prospects of the company.

Hence an investor is expected to use all the available tools at his/her disposal and conduct a detailed research of the company – both, from a qualitative and quantitative perspective – before making the final decision to go ahead with investments in a particular company or a set of companies. At the same time, it is equally important to be resilient during market downturns, or general market volatility and avoid taking any hasty decisions, which might result in loss of capital and avoiding stock market investments on the whole.

All investments should be done from a long term perspective, with periodic reviews – during quarterly results, or at points of major decisions by the company or at any change in the regulation affecting the industry as a whole – while adding more investments in the same company’s stock during general unfavourable market conditions.

Investing is laying out money now, to get more money in the future – Warren Buffett.

Next Chapter

Comments & Discussions in

FYERS Community

Harish commented on May 19th, 2019 at 10:13 PM

Ill be honest. this is good but not the best. Gopal, i follow you on twitter and between your quora responses and tweets,I gain more insights than from anywhere else. hence this module seems to miss the edge that a gopal touch otherwise brings. I am a novice myself so please dont think im here expecting advanced content :-) if there is a way you could compile your twitter/quora responses into a format suited to this platform,it would be way ahead of what currently exists...great work

Gopal commented on May 20th, 2019 at 8:04 PM

Hi Harsh, Thanks for your feedback. The advantage that I have while writing on Twitter or Quora is that I can use images, figures, data points, others view points etc which would be pertinent at that specific time. But, when content is composed on a knowledge sharing/educational platform, it is done with a view that the content will remain "in vogue" and doesn't become obsolete in a very short period of time, thereby requiring frequent updates in a very short span.

However, I will work with Tejas Khoday to see how to make the content better, while still keeping it relevant. Rgds Gopal

Samuvel commented on July 3rd, 2020 at 9:11 PM

Good work.

Informative.