Option contracts on the MCX

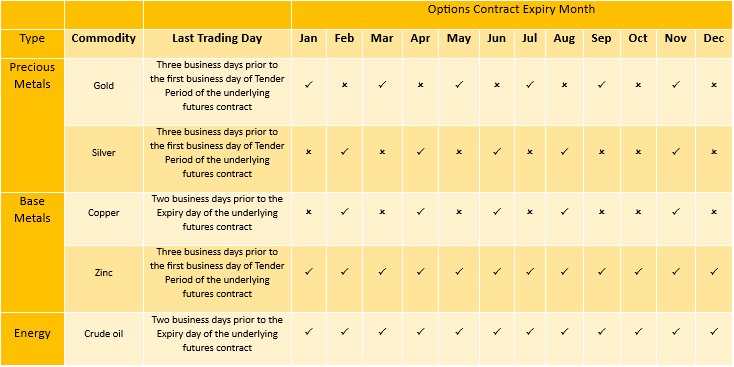

The table below shows the months for which commodity options are available for trading on the MCX:

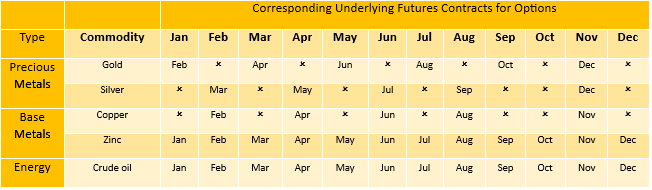

The table below shows the underlying futures contracts for the respective options contracts mentioned above:

Option expiry guidelines

Options on the MCX have futures rather than spot as the underlying. As such, certain elements such as trading unit, quotation per base value, and profit/loss per ₹1 movement remain the same as that seen in the underlying instrument i.e. the futures contract.

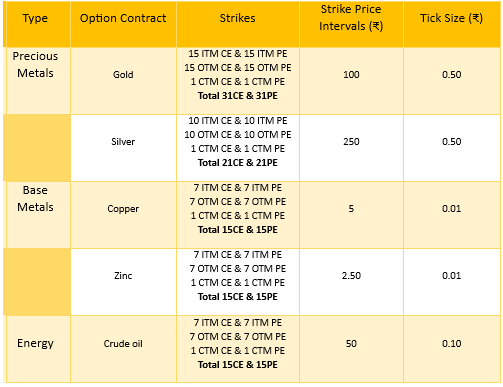

The table below shows some additional contract specifications for options traded on the MCX:

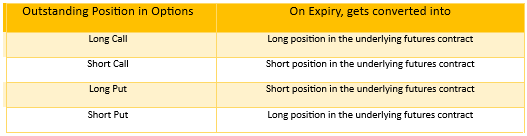

On expiry of the options contract, outstanding positions get converted into futures positions in the underlying futures contracts. How the conversion takes place is mentioned in the table below:

Earlier, we talked about settlement details of futures contracts. Now, let us discuss about the settlement details of option contracts traded on the MCX. On expiry, option settlement depends on the settlement price of the underlying futures contract relative to the options strike price. A thing to keep in mind in case of MCX options is the introduction of a new concept called CTM (Close-to-the-Money). This is how things work in case of MCX options:

-

ITM (In-the-Money) = strike price is below the settlement price for calls and above the settlement price for puts

-

OTM (Out-of-the-Money) = strike price is above the settlement price for calls and below the settlement price for puts

-

ATM (At-the-Money) = strike price that is closest to the settlement price for calls and puts

-

CTM (Close-to-the-Money) = Two strikes immediately below and two strikes immediately above the ATM option as well as the ATM option (in total, 5 strikes would be considered CTM)

Below mentioned are the general expiry settlement guidelines for each moneyness type:

-

For options belonging to the CTM series on expiry, the long position holder will have to give an “explicit instruction” to exercise the option and devolve it into futures, without which the option would expire worthless.

-

All ITM option contracts, excluding those that belong to the CTM series, will be exercised automatically and devolve into futures, unless the long position holder has given a “contrary instruction” to not exercise the option.

-

All OTM option contracts, excluding those that belong to the CTM series, will expire worthless.

-

For CTM option holders who have exercised their option by giving an “explicit instruction” to do so and for ITM option holders, the difference between the settlement price and the strike price would be given in cash.

-

For ITM option holders (excluding those belonging to the CTM series) who have given a “contrary instruction” to not exercise the option, the option contracts would expire worthless.

-

If OTM option holders who are falling under the CTM series exercise their option, they will have to pay the difference between the settlement price and the strike price.

-

Option positions that have been exercised and devolved into futures positions shall be done so at the strike price of the exercised option.

Options liquidity on the MCX

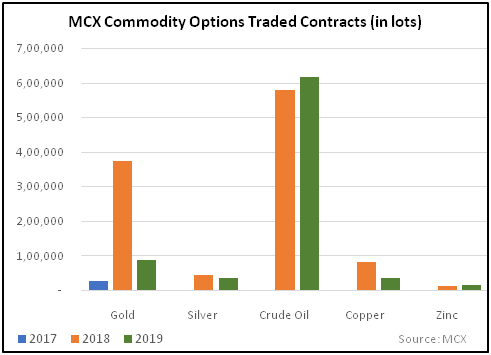

Commodity options were launched by the MCX only recently. The first commodity option to be launched by the MCX was on gold, in October 2017. Since then, the MCX has launched options on silver, crude oil, copper, and zinc. Being launched recently, volumes on options are still low and liquidity continues to be a problem. Below mentioned are the volume figures for various option contracts on the MCX.

As can be seen, volumes for commodity options are yet to pick up, especially in case of silver, copper, and zinc, where volumes are quite negligible at present.

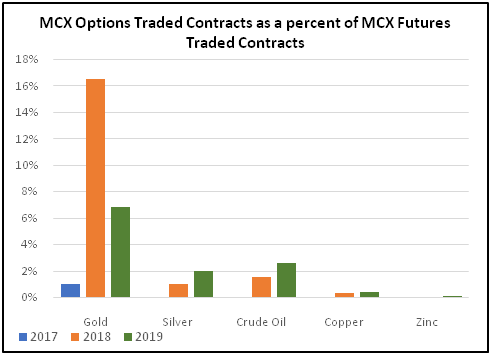

The chart above shows MCX options traded contracts as a percentage of MCX futures traded contracts for gold, silver, crude oil, copper, and zinc. As can be seen, the relative volumes on options are quite low at present. That said, being a product that was launched only recently and with more option contracts likely to be introduced in the future, option volumes are likely to pick up gradually as awareness among participants increases and as the need for options increases in the face of rising volatility across commodities.

One of the major benefits of trading options is the limited risk feature they entail – if you buy options, you cannot lose more than what you have put in. This is unlike futures where losses could be potentially unlimited.

Options can help those who want to hedge their exposure in the underlying commodity. For instance, an investor who has a long exposure in gold but expects some short-term headwinds to gold prices can buy put options to insure against short-term volatility in gold price. Doing so would have dual benefits. If his view goes right and gold price drops in the short-term, his losses in the underlying position would be offset by the gains he would made in the put position. On the other hand, if his view goes wrong and gold price rises in the short-term, his option would expire worthless (meaning he would lose the entire premium that he paid upfront), but this loss would be offset by the gain that he would make in the underlying exposure.

Let us explain this using an example. Let us assume that an investor has a long exposure in gold to the tune of 1kg. Let us also assume that gold is currently trading at ₹30,000 and that the investor is worried that gold price could weaken in the short-term. In order to safeguard against price volatility, the investor can buy a gold put option having a strike price of, say, ₹30,000. Let us assume the premium for this option is ₹500. So, to buy 1 lot of gold put option with strike price ₹30,000, the investor will have to make an upfront payment of ₹50,000 (option price ₹500 * lot size 100). This is the maximum amount he stands to lose in the options position. If by expiry of the option, gold price drops to, say, ₹28,000, the investor would make a loss of ₹2,00,000 in the underlying position ({₹28,000 - ₹30,000} * 1000 / 10), but he would make a gain of ₹1,50,000 in the put position ({₹30,000 - ₹28,000) * 100 - ₹50,000). Alternatively, if by expiry of the option, gold price rises to, say, ₹33,000, the investor would lose the entire premium of ₹50,000 paid upfront, but make a gain to the extent of ₹3,00,000 ({₹33,000 - ₹30,000} * 1000 / 10).

As can be seen above, in case 1 (wherein gold fell to ₹28,000), his net loss was reduced to ₹50,000 (without hedging the exposure, he would have made a loss of ₹2,00,000); while in case 2 (wherein gold rose to ₹33,000), his profit was slightly reduced to ₹2,50,000 (without hedging, he would have gained ₹3,00,000). There are various complex option strategies that can be deployed along with the basic buy call, buy put strategies, in order to lower the cost of options further. However, these strategies are beyond the scope of this section. The idea of this section is just to show that when used effectively, options can be an excellent hedging tool.

Next Chapter

Comments & Discussions in

FYERS Community

Bhupati commented on July 15th, 2019 at 11:25 PM

Can we apply same indicators and strategies like capital market to the commodities?

tejas commented on August 14th, 2019 at 4:25 PM

Indicators and strategies must change as per the instrument and product you're trading. There is no one size that fits all in the trading business. You'll have to understand and strategize everything separately in my opinion.