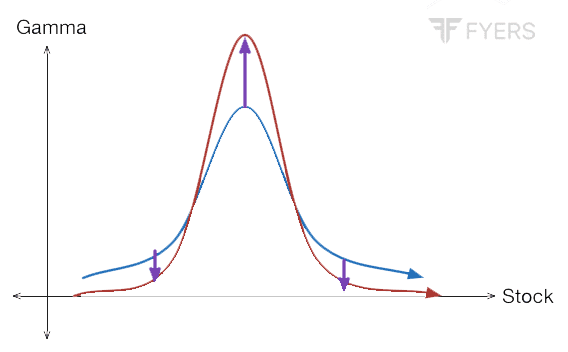

In this chapter, we will study about a derivative of Delta, called Gamma. We will start the chapter by introducing Gamma, including how it impacts the Delta of an option. We will then talk about how Gamma is impacted by option moneyness, time to expiration, and volatility.