31 Aug, 2025

31 Aug, 2025

5 mins read

5 mins read

Understanding the movement of funds within a business is crucial for financial planning and decision-making. One of the tools used to analyse these movements is the fund flow statement. While often overshadowed by the cash flow statement, this financial document provides valuable insights into how a company sources and utilises its funds over a given period.

In this blog, we’ll explain what a fund flow statement is, its key objectives, components, and how it differs from other financial statements.

A fund flow statement shows the changes in the financial position of a company between two balance sheet dates. Specifically, it tracks the movement of working capital by identifying the sources and uses of funds. Unlike the cash flow statement, which focuses on cash transactions, the fund flow statement looks at all financial resources.

It answers two key questions:

Where did the funds come from?

How were the funds used?

This statement is essential for understanding the financial health and operational efficiency of a business.

The fund flow statement serves several strategic objectives:

Identify financial inflows and outflows: It helps pinpoint how funds are generated and where they are spent.

Analyse changes in working capital: By tracking the variation in current assets and liabilities, it reveals how operations affect liquidity.

Aid financial planning: It supports better forecasting by highlighting long-term financial trends.

Monitor business performance: It helps assess how effectively a company uses its financial resources to grow and sustain operations.

While it may not be part of standard statutory reporting, the fund flow statement is important for both internal and external stakeholders.

Financial control: Managers use it to track whether resources are being allocated efficiently.

Investment analysis: Investors and analysts assess it to evaluate a company’s financial strategy.

Loan assessment: Banks and lenders rely on it to judge a company’s creditworthiness.

Strategic decision-making: It supports decisions like expansion, capital budgeting, and restructuring.

The fund flow statement includes two main parts:

Lists current assets and current liabilities

Calculates the net increase or decrease in working capital

Sources include:

Issue of share capital

Long-term borrowings

Sale of fixed assets

Operational income not affecting working capital

Uses include:

Purchase of fixed assets

Repayment of loans

Payment of dividends

Increase in working capital

|

Sources of Funds |

Amount (₹) |

Uses of Funds |

Amount (₹) |

|---|---|---|---|

|

Issue of Shares |

5,00,000 |

Purchase of Machinery |

2,50,000 |

|

Long-term Loan Raised |

3,00,000 |

Loan Repayment |

2,00,000 |

|

Profit from Operations |

1,50,000 |

Increase in Working Capital |

5,00,000 |

|

Total |

9,50,000 |

Total |

9,50,000 |

While both statements track financial movement, they serve different purposes:

|

Basis |

Fund Flow Statement |

Cash Flow Statement |

|---|---|---|

|

Focus |

Changes in working capital |

Actual cash inflows and outflows |

|

Period |

Long-term view |

Short-term liquidity |

|

Basis of Accounting |

Accrual |

Cash |

|

Objective |

Identify source and application of funds |

Understand cash generation and utilisation |

|

Use |

Strategic planning |

Daily cash management |

Both are complementary. The fund flow statement offers a broader view of financial health, while the cash flow statement addresses immediate cash positions.

Here are the basic steps to prepare a fund flow statement:

Prepare comparative balance sheets: Use the data from two consecutive financial years.

Determine changes in working capital: Prepare a statement of changes in current assets and liabilities.

Identify sources and applications: Track transactions that affect non-current items.

Prepare the fund flow statement: List sources on one side and uses on the other to ensure they tally.

Reading a fund flow statement involves analysing how effectively a business has managed its funds:

A positive net working capital indicates financial stability and good liquidity.

If major funds are used for asset creation, it signals long-term growth.

Rising liabilities or reduced capital could suggest over-reliance on external borrowing.

Compare profit retained vs funds used to assess operational efficiency.

Despite its benefits, the fund flow statement has some limitations:

Does not track cash: It excludes day-to-day cash flow, which can be critical for liquidity.

Historical in nature: It reflects past transactions, not real-time financial status.

Ignores non-fund items: Certain accounting entries that don’t impact working capital are not included.

Requires supporting data: It cannot be prepared in isolation without balance sheets and income statements.

A fund flow statement is a valuable tool for understanding how an organisation manages its financial resources over time. While it may not replace the cash flow statement, it complements it by offering a more strategic and long-term perspective on financial movements.

For business owners, investors, and financial analysts, mastering the fund flow statement can lead to better planning, improved decision-making, and a stronger grasp of a company’s financial operations.

A fund flow statement is a financial report that shows where a company’s funds came from and how they were used during a particular period. It focuses on changes in working capital and helps assess financial health beyond just cash movements.

Fund flow statements are used by company management, investors, lenders, and financial analysts to evaluate how efficiently a company sources and uses its funds. It’s especially useful for long-term planning and financial analysis.

The format includes:

Statement of Changes in Working Capital

Statement of Sources and Uses of Funds

Each section helps identify how much working capital changed and what transactions caused the shift in financial position.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

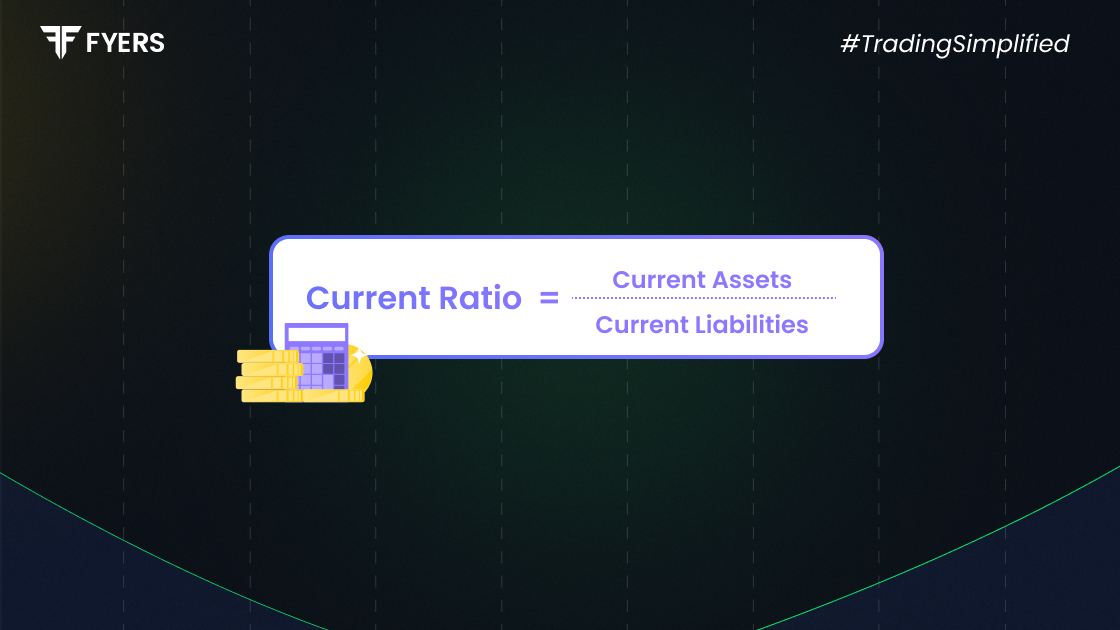

The current ratio is one of the most widely used…

31 Aug, 2025

4 mins read

You have successfully submitted your partnership request form. You will be hearing us soon!