27 May, 2025

27 May, 2025

8 mins read

8 mins read

When you're running a business, managing your day-to-day finances can feel like walking a tightrope. You need enough cash to pay your suppliers, cover employee salaries, and keep operations running smoothly, while planning for future growth. This is where working capital becomes your financial lifeline the difference between thriving and merely surviving in today's competitive marketplace.

Working capital isn't just another accounting term you can ignore. It's the beating heart of your business operations, determining whether you can seize new opportunities or struggle to meet basic obligations. Whether you're a startup founder,managing an established enterprise, or an investor looking to evaluate a company, understanding the importance and how to calculate working capital can be very helpful.

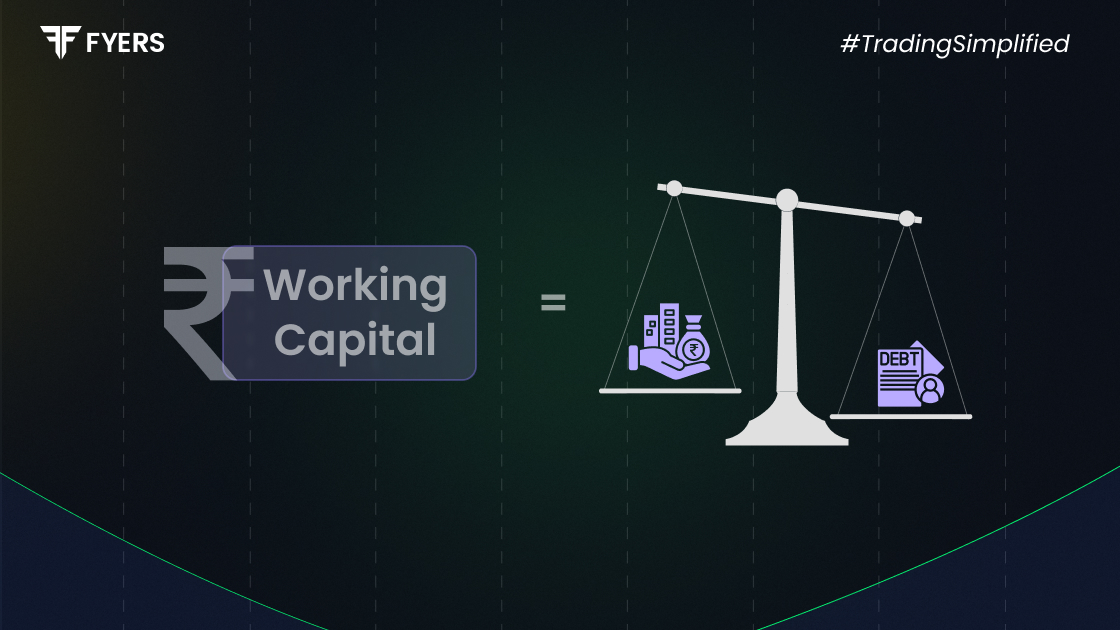

Working capital is critical to gauge a company's short-term health, liquidity, and operational efficiency. You calculate working capital by subtracting current liabilities from current assets, giving you a clear picture of the funds available for daily business operations.

Think of working capital as the money you have readily available to run your business on a day-to-day basis. It's the financial cushion that ensures you can pay bills, purchase inventory, and cover operational expenses without scrambling for emergency funding.

Working capital consists of two main components:

Current Assets include:

Cash and cash equivalents

Accounts receivable (money customers owe you)

Inventory (raw materials, work-in-progress, finished goods)

Short-term investments

Prepaid expenses

Current Liabilities include:

Accounts payable (money you owe suppliers)

Short-term loans and credit facilities

Accrued expenses (wages, utilities, rent)

Tax obligations due within one year

Current portion of long-term debt

The relationship between these components determines your working capital position and ultimately your business's ability to operate effectively.

Proper working capital management ensures a company maintains adequate cash flow to meet its operational needs and financial commitments. Here's why working capital matters for your business:

Without adequate working capital, you risk running out of cash to pay suppliers, employees, or other essential expenses. This can lead to operational disruptions and damage your business relationships.

Positive working capital gives you the freedom to take advantage of unexpected opportunities, such as bulk purchase discounts or sudden market demands, without seeking external financing.

Lenders and suppliers view businesses with healthy working capital as lower-risk partners. This can lead to better credit terms, lower interest rates, and stronger business relationships.

Managing working capital effectively helps reduce the operating cycle of a business – this is the time it takes for a company to convert its investment in inventory and/or other assets into cash generated through sales. This efficiency supports sustainable growth.

Working capital serves as a buffer during economic downturns or unexpected challenges, helping your business weather difficult periods without compromising operations.

The working capital formula is straightforward:

|

Working Capital = Current Assets - Current Liabilities |

Let's break down the calculation with a practical example:

Imagine you run a retail business with the following financial position:

|

Current Assets |

Amount (₹) |

|---|---|

|

Cash in bank |

20,50,000 |

|

Accounts receivable |

12,25,000 |

|

Inventory |

28,75,000 |

|

Prepaid expenses |

4,10,000 |

|

Total Current Assets |

65,60,000 |

|

Current Liabilities |

Amount (₹) |

|---|---|

|

Accounts payable |

16,40,000 |

|

Short-term loans |

12,30,000 |

|

Accrued expenses |

8,20,000 |

|

Total Current Liabilities |

36,90,000 |

Working Capital = ₹65,60,000 - ₹36,90,000 = ₹28,70,000

This positive working capital of ₹28,70,000 indicates your business has sufficient short-term assets to cover immediate obligations, with ₹28,70,000 remaining for operations.

Working capital ratios between 1.2 and 2.0 indicate a company is making effective use of its resources. The working capital ratio formula is:

Working Capital Ratio = Current Assets ÷ Current Liabilities

Using our previous example: Working Capital Ratio = ₹65,60,000 ÷ ₹36,90,000 = 1.78

Companies typically target a working capital ratio of between ₹1.50 and ₹1.75 for every ₹1 of current liabilities, making our example business financially healthy.

Understanding different types of working capital helps you make informed financial decisions:

This refers to the total current assets. It shows the total short-term resources available but doesn't account for obligations.

This is the standard working capital calculation (Current Assets - Current Liabilities) that provides a clearer picture of your financial position.

The minimum level of working capital required to maintain business operations throughout the year. This includes basic inventory levels, minimum cash requirements, and essential receivables.

Additional working capital needed during peak seasons or special circumstances. For example, a toy retailer might need extra working capital before Christmas.

The working capital required for normal business operations under standard market conditions.

Extra working capital maintained as a safety buffer for unexpected situations or opportunities.

Let's examine a real-world working capital scenario using India's leading IT services company:

Company Overview: Infosys, with a market capitalisation of ₹6,56,523 crores and annual revenue of ₹1,92,800 lakh, provides an excellent example of working capital management in the IT services sector.

Based on typical IT services company financials, here's a representative working capital analysis:

|

Current Assets (₹ Crores) |

FY 2023 |

FY 2024 |

|---|---|---|

|

Cash and equivalents |

25,480 |

26,340 |

|

Trade receivables |

8,650 |

9,210 |

|

Contract assets |

2,340 |

2,580 |

|

Other current assets |

3,200 |

3,450 |

|

Total Current Assets |

39,670 |

41,580 |

|

Current Liabilities (₹ Crores) |

FY 2023 |

FY 2024 |

|---|---|---|

|

Trade payables |

1,240 |

1,380 |

|

Contract liabilities |

4,560 |

4,890 |

|

Employee benefit payables |

8,920 |

9,450 |

|

Other current liabilities |

2,180 |

2,320 |

|

Total Current Liabilities |

16,900 |

18,040 |

Working Capital Analysis:

FY 2023: ₹39,670 crores - ₹16,900 crores = ₹22,770 crores

FY 2024: ₹41,580 crores - ₹18,040 crores = ₹23,540 crores

Working Capital Ratio Analysis:

FY 2023: ₹39,670 ÷ ₹16,900 = 2.35

FY 2024: ₹41,580 ÷ ₹18,040 = 2.30

Key Insights:

The company maintains an exceptionally strong working capital of ₹23,540 crores, reflecting the cash-rich nature of IT services.

The high working capital ratio of 2.30 indicates a strong liquidity position

IT services companies typically maintain higher working capital ratios due to advance client payments and strong cash generation

While working capital is a valuable financial metric, it has several limitations you should understand:

Working capital provides a snapshot at a specific date but doesn't show trends or seasonal variations. Your working capital on 31st March might differ significantly from 30th June due to business cycles.

The calculation treats all current assets equally, but some may be more liquid than others. For instance, obsolete inventory might be difficult to convert to cash despite being counted as an asset.

Working capital doesn't indicate when cash will flow in or out of your business. You might have positive working capital but still face cash flow problems if receivables are collected slowly.

High working capital isn't always a good thing. It might indicate that the business has too much inventory or isn't investing excess cash. Different industries have varying working capital requirements, making comparisons challenging.

Companies can temporarily improve working capital figures through techniques like delaying payments or accelerating collections near reporting dates, potentially misleading stakeholders.

Working capital focuses only on short-term financial health and doesn't account for long-term sustainability or strategic investments.

Effective working capital management can significantly improve your business performance. Here are practical strategies:

Implement credit checks: Assess customer creditworthiness before extending credit terms

Offer early payment discounts: Provide 2-5% discounts for payments within 10-15 days

Use electronic invoicing: Speed up invoice delivery and processing

Follow up promptly: Establish systematic collection procedures for overdue accounts

Use just-in-time ordering: Reduce holding costs by ordering inventory as needed

Implement ABC analysis: Focus on high-value items that impact cash flow most

Regular inventory audits: Identify slow-moving or obsolete stock

Negotiate supplier terms: Extend payment periods whilst maintaining good relationships

Take advantage of payment terms: Pay suppliers on the last day of the credit period.

Negotiate better terms: Request extended payment periods for regular suppliers.

Use trade credit wisely: Balance cash conservation with supplier relationships.

Automate payments: Reduce processing costs and avoid late payment penalties

Weekly cash flow projections: Monitor expected inflows and outflows

Scenario planning: Prepare for best-case, worst-case, and most likely scenarios

Use cash flow management tools: Implement software to track and predict cash movements

Regular reviews: Update forecasts based on actual performance

Maintain banking relationships: Keep open lines of communication with lenders

Secure revolving credit: Arrange facilities for temporary working capital needs

Diversify funding sources: Don't rely on a single lender or funding type

Monitor covenant compliance: Ensure you meet all lending agreement requirements

|

Strategy |

Timeline |

Expected Impact |

Key Metrics to measure |

|---|---|---|---|

|

Reduce average collection period |

3 months |

Improve cash flow by 15-20% |

Days sales outstanding |

|

Optimise inventory levels |

6 months |

Free up 10-25% of tied capital |

Inventory turnover ratio |

|

Extend supplier payment terms |

2 months |

Improve cash flow timing |

Days payable outstanding |

|

Implement cash flow forecasting |

1 month |

Better financial planning |

Forecast accuracy percentage |

Working capital management isn't just about crunching numbers - it's about ensuring your business has the financial flexibility to thrive in today's dynamic marketplace. By understanding the components, calculations, and strategies outlined in this guide, you're better equipped to make informed decisions that support both daily operations and long-term growth.

Investors should always remember that working capital requirements vary by industry and business model, so regularly review your position and adjust investment strategies accordingly.

Working capital is the money available for daily operations after paying short-term debts. It's calculated as Current Assets - Current Liabilities.

Working capital ensures your business can pay employees, buy inventory, and cover expenses without interruption. It acts as a financial safety net for smooth operations.

Common causes include poor cash flow management, excessive inventory, too much short-term debt, seasonal business patterns, and delayed customer payments.

Speed up customer collections, manage inventory efficiently, negotiate better supplier payment terms, improve cash flow forecasting, and consider financing options for temporary shortfalls.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!