16 Sep, 2025

16 Sep, 2025

4 mins read

4 mins read

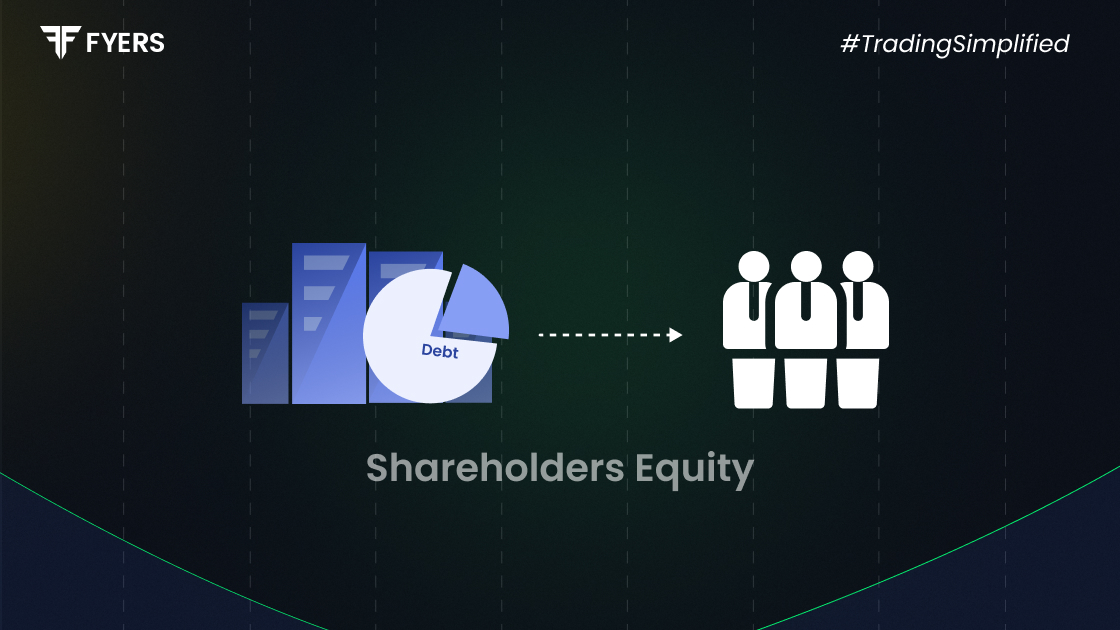

Understanding shareholder equity is essential for evaluating a company’s financial health. Often referred to as net assets or owners' equity, this figure represents the residual interest of shareholders in the assets of a company after deducting liabilities. In this blog, we will break down what shareholder equity means, how it is calculated, and what it reveals about a business.

Shareholder equity is the amount of capital that would be returned to shareholders if all assets were liquidated and all debts were paid off. It reflects the net worth of a business and can serve as a barometer for financial stability and growth potential.

It appears on the balance sheet and is an important metric for investors, analysts, and company management. A positive shareholder equity indicates that the company has enough assets to cover its liabilities, while a negative figure may signal financial distress.

Shareholder equity comprises several components, each offering insight into how the equity base was built. The main components include:

Share Capital: The amount raised by issuing equity shares to investors.

Retained Earnings: Profits that have been reinvested in the business rather than distributed as dividends.

Reserves and Surplus: Includes capital reserves and revenue reserves set aside for specific purposes.

Treasury Shares (if any): Shares that the company has repurchased from the market, which reduce equity.

These components vary based on company structure, policies, and accounting standards, but together, they form the total equity held by shareholders.

The basic formula for calculating shareholder equity is:

|

Shareholder Equity = Total Assets − Total Liabilities |

This calculation is derived from the accounting equation:

|

Assets = Liabilities + Shareholders' Equity |

Let’s break it down further:

Identify all assets, including current and non-current (e.g., cash, inventory, property and equipment).

Identify all liabilities, both current (e.g., accounts payable, short-term loans) and long-term (e.g., bonds payable, deferred tax liabilities).

Subtract the total liabilities from total assets to arrive at the shareholder equity.

This figure is usually found in the company’s balance sheet, under the equity section.

Boosting shareholder equity is often a sign of good financial management. Here are several ways companies can improve this figure:

Increase Profits: Higher net income, if retained, increases retained earnings.

Retain Earnings: Reducing dividend payouts allows more capital to remain within the business.

Asset Efficiency: Selling non-performing assets and improving operational efficiency increases asset value.

Debt Reduction: Paying off liabilities directly increases net equity.

Issuing Shares: Bringing in new capital through equity issuance increases share capital.

Sustainable growth strategies aimed at long-term profitability are usually the most effective in building strong shareholder equity.

Consider the following simplified balance sheet data for Company X:

|

Particulars |

Amount (in ₹ crore) |

|---|---|

|

Total Assets |

500 |

|

Total Liabilities |

300 |

|

Shareholder Equity |

200 |

Calculation:

Shareholder Equity = Total Assets − Total Liabilities

= ₹500 crore − ₹300 crore

= ₹200 crore

This means that Company X has a net worth of ₹200 crore. This capital belongs to the shareholders and reflects the company’s financial cushion.

In another example, if Company Y has accumulated high retained earnings over years, it may show a high shareholder equity even without raising new share capital. This often indicates operational strength and consistency in profit generation.

Shareholder equity is a fundamental measure of a company's financial strength. It helps assess whether a business has sufficient assets to meet its liabilities and gives insight into how effectively it manages profits and capital. A steadily increasing shareholder equity is usually a positive sign, reflecting growing net worth and prudent financial management. For investors, it's a key metric when evaluating long-term investment prospects.

Negative shareholder equity means the company’s liabilities exceed its assets. This can be a red flag, indicating potential insolvency or operational challenges. Persistent negative equity often signals financial trouble and may affect the company’s ability to raise further capital.

No, shareholder equity represents the book value based on accounting records, whereas market value of equity is calculated by multiplying the share price by the total number of outstanding shares. Market value reflects investor perception and can differ significantly from the book value.

It should be reviewed quarterly and annually as part of financial reporting. Frequent monitoring helps stakeholders assess the company's financial health and track changes in its capital structure over time.

Not necessarily. While high equity can indicate financial stability, it must be evaluated alongside profitability, return on equity, and industry norms. A company with high equity but poor returns may not be an efficient allocator of capital.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!