15 Sep, 2025

15 Sep, 2025

4 mins read

4 mins read

Understanding where a company’s cash comes from and where it goes is crucial for investors, analysts and business owners alike. Among the different sections of a cash flow statement, cash flow from operating activities (CFO) is often considered the most insightful. This blog explains what CFO is, how it’s calculated, and why it matters.

Cash flow from operating activities refers to the net amount of cash generated or used by a company from its core business operations. It excludes revenue from investments or financing. Instead, it focuses purely on the inflow and outflow of cash directly related to selling goods or services.

It includes transactions such as:

Receipts from customers

Payments to suppliers

Salaries and wages

Tax payments

Other routine operating expenses

CFO gives a clear picture of whether a company can generate enough cash to sustain its daily operations and fund its growth without relying on external financing.

There are two main ways to calculate CFO:

The direct method lists all major operating cash receipts and payments during the period.

For example:

Cash received from customers

Cash paid to suppliers and employees

Cash paid for operating expenses

Cash paid for taxes

This method provides a detailed breakdown but is rarely used due to the complexity of gathering data.

The indirect method is more commonly used, especially in India. It starts with the net profit and adjusts for non-cash items and changes in working capital.

The formula is:

| CFO = Net Profit + Non-Cash Expenses + Changes in Working Capital |

Non-cash items might include depreciation, amortisation and provisions, while working capital changes refer to adjustments in accounts receivable, inventory and payables.

Using the indirect method, the general formula is:

CFO = Net Income

Non-Cash Expenses (Depreciation, Amortisation)

Non-Cash Income (such as profit on sale of assets)

Decrease in Current Assets (like accounts receivable, inventory)

Increase in Current Assets

Increase in Current Liabilities (like trade payables)

Decrease in Current Liabilities

This formula helps bridge the gap between net income and actual cash movements, offering a realistic picture of a company's liquidity.

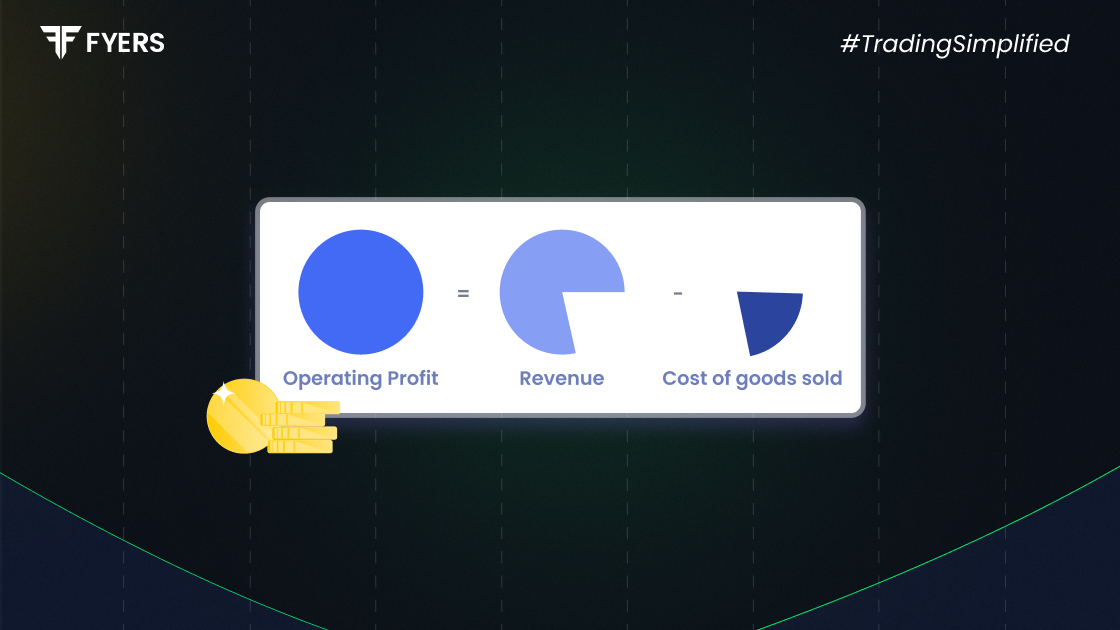

While both CFO and net income measure a company’s profitability, they do so from different perspectives:

|

Basis |

Net Income |

CFO |

|---|---|---|

|

Nature |

Accounting profit |

Actual cash inflow/outflow |

|

Includes Non-Cash Items |

Yes (such as depreciation) |

No |

|

Affected by Working Capital |

No |

Yes |

|

Reflects Liquidity |

Partially |

Directly |

A company may show strong net income but poor cash flow if a lot of its earnings are tied up in unpaid invoices or unsold inventory.

Let’s consider a simplified example:

XYZ Ltd. has the following financials for the year:

Net Income: ₹40 lakh

Depreciation: ₹5 lakh

Increase in Inventory: ₹3 lakh

Increase in Trade Payables: ₹2 lakh

Taxes Paid: ₹10 lakh

Using the indirect method:

CFO = ₹40 lakh (Net Income)

₹5 lakh (Depreciation)

₹3 lakh (Inventory Increase)

₹2 lakh (Increase in Payables)

₹10 lakh (Taxes Paid)

= ₹34 lakh

So, XYZ Ltd. has generated ₹34 lakh from operating activities despite earning a net profit of ₹40 lakh. This indicates good cash management.

Cash flow from operating activities offers a vital insight into a company’s operational efficiency and financial health. It reflects how well the core business is generating cash, separate from financing and investment decisions. While net profit shows accounting success, CFO shows the reality of money movement, which is crucial for paying bills, reinvesting and sustaining growth. Investors, lenders, and stakeholders rely on this metric to assess a company’s long-term viability.

It refers to the actual cash a company earns or spends through its regular business operations, like selling products and paying suppliers. It excludes investment or financing-related cash flows.

The most common formula using the indirect method is:

CFO = Net Income + Non-Cash Expenses ± Changes in Working Capital

This shows how net profit is converted into actual cash flow.

Indian companies generally follow the indirect method for reporting CFO in their cash flow statements, as per accounting standards prescribed by the Ministry of Corporate Affairs.

Yes, if a company spends more cash than it earns from its core business, CFO will be negative. This could indicate operational issues, declining sales, or high working capital requirements.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!