30 Jul, 2025

30 Jul, 2025

4 mins read

4 mins read

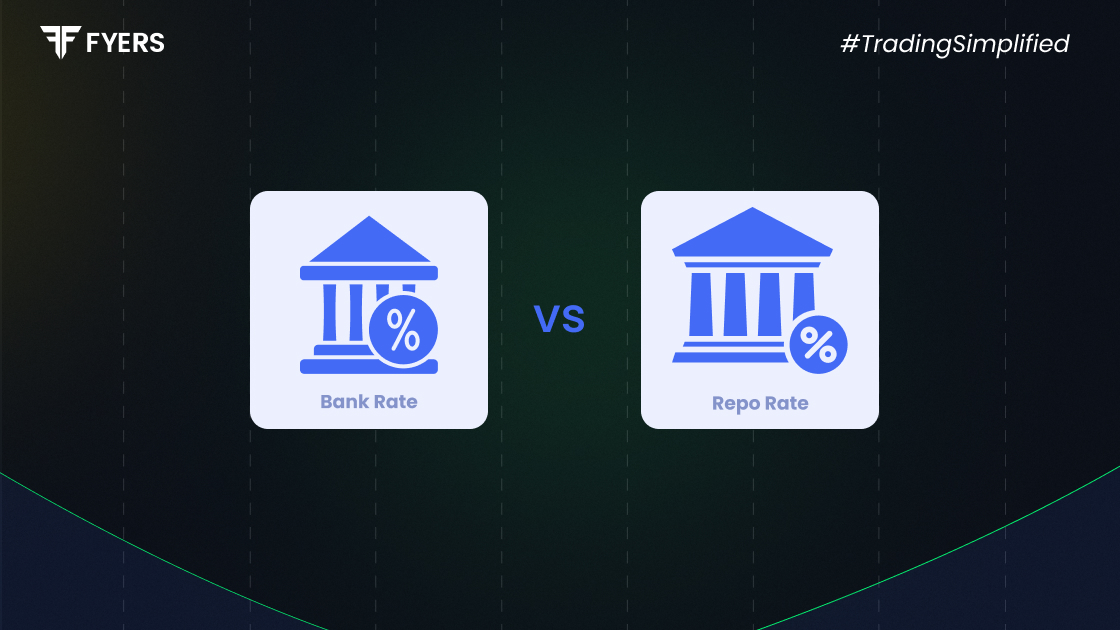

In the intricate machinery of monetary policy, interest rates are the levers that shape liquidity, inflation, and economic momentum. Among these, the repo rate and bank rate stand out as two pivotal tools wielded by the Reserve Bank of India (RBI). Though they may sound similar, their functions, implications, and regulatory roles differ in meaningful ways. Understanding the difference between repo rate and bank rate is essential not only for financial professionals but also for anyone seeking to decode the signals behind RBI’s policy decisions.

The repo rate, short for repurchase rate, is the interest rate at which the RBI lends short-term funds to commercial banks against government securities. These transactions are typically overnight and are governed by a repurchase agreement, where banks pledge securities and agree to buy them back at a predetermined price.

In essence, what is repo rate? It’s the RBI’s primary tool for managing short-term liquidity in the banking system. When banks face a temporary cash crunch, they borrow from the RBI at the repo rate. A higher repo rate makes borrowing more expensive, thereby reducing the money supply and curbing inflation. Conversely, a lower repo rate encourages borrowing, boosting liquidity and stimulating economic activity.

The bank rate is the interest rate at which the RBI lends long-term funds to commercial banks, without requiring any collateral. Unlike repo transactions, loans under the bank rate are not backed by government securities.

So, what is bank rate in practical terms? It serves as a benchmark for long-term lending and regulatory penalties. While it’s not used frequently in day-to-day liquidity operations, the bank rate plays a crucial role in signalling the RBI’s stance on long-term interest rates and is often linked to penalties for banks failing to meet statutory requirements like the Cash Reserve Ratio (CRR) or Statutory Liquidity Ratio (SLR).

Here’s a detailed comparison to clarify the repo rate and bank rate difference:

|

Feature |

Repo Rate |

Bank Rate |

|---|---|---|

|

Definition |

Short-term lending rate by RBI |

Long-term lending rate by RBI |

|

Tenure |

Typically overnight |

No fixed tenure; used for signalling |

|

Collateral Requirement |

Requires government securities |

No collateral required |

|

Use in Monetary Policy |

Actively used to manage liquidity and inflation |

Used for regulatory signalling and penalties |

|

Impact on Economy |

Influences lending and deposit rates |

Sets floor for long-term interest rates |

|

Link to Liquidity |

Direct tool for liquidity management |

Indirect signalling mechanism |

|

Review Frequency |

Bi-monthly via MPC |

Infrequent; discretionary by RBI |

|

Current Rate (June 2025) |

5.50% |

5.75% |

This comparison underscores the bank rate vs repo rate distinction: the repo rate is a dynamic, frequently adjusted tool with immediate economic impact, while the bank rate is more static, serving as a regulatory anchor.

In the symphony of monetary policy, the repo rate and bank rate play distinct yet complementary roles. The repo rate orchestrates short-term liquidity and inflation control, while the bank rate sets the tone for long-term lending and regulatory discipline. Understanding the repo rate and bank rate difference equips investors, borrowers, and policymakers to better interpret RBI’s signals and anticipate shifts in the financial landscape.

As the RBI continues to fine-tune these rates in response to evolving economic conditions, staying informed about the repo rate impact on economy and the strategic use of the bank rate is more than academic. It’s key to making smarter financial decisions.

The current repo rate and bank rate are set by the RBI and are announced during policy reviews. You can check the RBI's official website or financial news platforms for the latest figures.

The Reserve Bank of India sets both rates. The Monetary Policy Committee (MPC) decides the repo rate, while the RBI independently manages the bank rate.

Yes, the bank rate is typically equal to or slightly higher than the repo rate, reflecting its use for long-term lending without collateral.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!