20 May, 2025

20 May, 2025

4 mins read

4 mins read

Understanding your CIBIL score is the first step towards managing your financial health. Whether you're applying for a credit card, home loan, or car loan, this little three-digit number can decide your eligibility. But what is a CIBIL score? How is it calculated, and why does it matter so much?

In this guide, we’ll break down everything you need to know - from the meaning of CIBIL score to how to improve it, check it, and keep it healthy.

Your CIBIL score is a number between 300 and 900 that reflects your creditworthiness. It is provided by TransUnion CIBIL or any of the other credit bureaus like Experian, Equifax or Crif High Mark. The higher your score, the more likely lenders are to trust you with credit.

In simple terms, the CIBIL score is a summary of your credit behaviour - how you've used and repaid credit in the past.

Wondering how the CIBIL score is calculated?

It’s based on your credit history collected from banks and financial institutions. This includes:

Your loan and credit card repayment history

Number of credit accounts

Total outstanding debt

Length of credit history

Credit enquiries by lenders

Each of these CIBIL score factors plays a role in determining your score. For instance, regular and timely repayments will raise your score, while defaults or late payments can pull it down.

Here’s a rough breakdown of how these components are weighted:

Payment history – 35%

Credit exposure (amount owed) – 30%

Length of credit history – 15%

New credit enquiries – 10%

Credit mix (secured vs. unsecured loans) – 10%

A good CIBIL score can open doors to better credit opportunities. Here’s why it matters:

Loan approval becomes easier – Lenders are more confident about giving you money.

Better interest rates – You may qualify for lower interest rates on loans and credit cards.

Higher credit limits – With a strong credit history, banks may offer you a higher credit limit.

Faster loan processing – Lenders won’t need as many checks if you’ve got a high score.

In short, your CIBIL score tells lenders whether you're a reliable borrower or a risky one.

Many people are surprised to know how everyday financial behaviour can affect their score. Here are the major CIBIL score factors you should watch out for:

Late Payments - Missing due dates for credit card bills or EMIs can severely damage your score.

Credit Utilisation Ratio - Using a high percentage of your credit limit on credit cards regularly can signal financial stress.

Multiple Loan Applications - Too many hard enquiries in a short time might show you're desperate for credit.

Credit Mix - A good mix of secured (like home loans) and unsecured loans (like credit cards) is ideal.

Length of Credit History - A long and clean credit history works in your favour.

If your score is low, don’t worry - there are simple steps you can take to improve your CIBIL score over time.

This is the most effective way to improve your CIBIL score. Set reminders or automate your payments to avoid delays.

Aim to keep your credit utilisation below 30% of your available limit on your credit card.

Space out your applications to avoid looking credit-hungry.

Closing old credit cards can shorten your credit history and negatively affect your score.

Sometimes, incorrect information can pull your score down. Raise a dispute if you find mistakes.

Remember, improving your CIBIL score is a gradual process - but a worthwhile one.

Curious about how to check CIBIL score?

It’s easy, free, and can be done online in just a few steps:

Go to CIBIL’s official website.

Click on ‘Get Your Free CIBIL Score’.

Enter your details - name, date of birth, ID proof, etc.

Answer a few questions to verify your identity.

View your score and download your report.

It’s a good habit to check your score at least twice a year to monitor changes and spot any issues early.

Your CIBIL score plays a big role in your financial life. Whether you're planning to buy a car, get a home loan, or simply apply for a new credit card, this score can impact your chances.

Now that you understand what is CIBIL score is, how CIBIL score is calculated, and how to improve CIBIL score, you’re in a better position to manage your credit health.

Always aim to build a solid credit history by paying on time, borrowing responsibly, and reviewing your score regularly. Financial discipline today leads to financial freedom tomorrow.

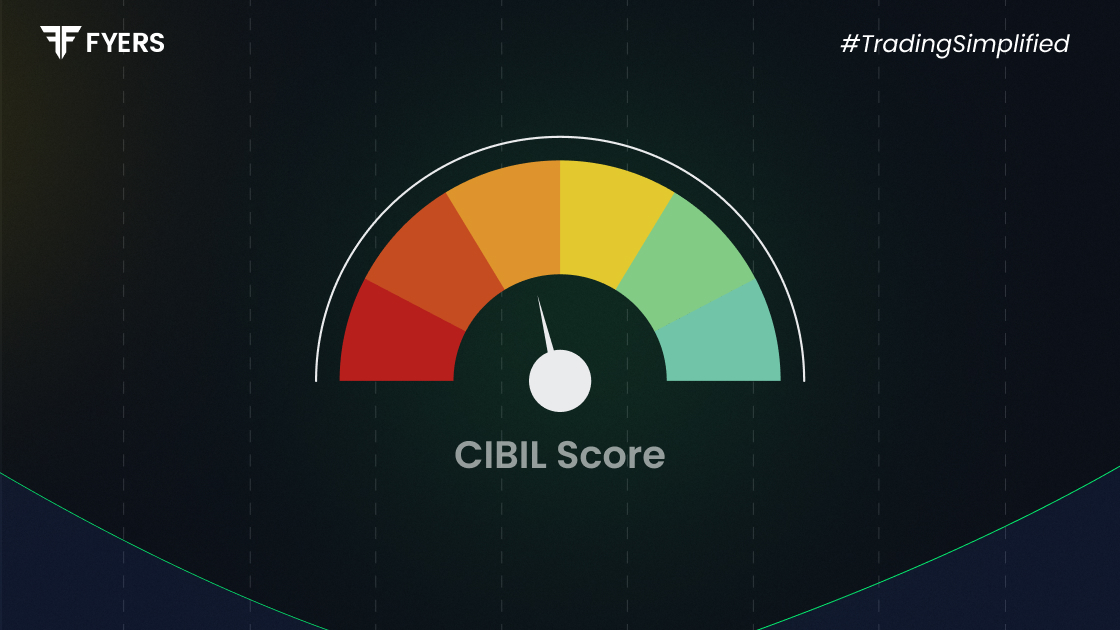

A score of 750 or above is considered excellent and increases your chances of loan or credit card approval. Here's a quick scale:

750 – 900: Excellent

700 – 749: Good

650 – 699: Fair

600 – 649: Poor

Below 600: Very Poor

Your CIBIL score is just a number that summarises your creditworthiness.

A credit report, on the other hand, is a detailed document that shows your entire credit history - loan accounts, credit card usage, repayment behaviour, and more. The score is a part of the report, but the report includes the full story behind that score.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!