15 Jul, 2025

15 Jul, 2025

4 mins read

4 mins read

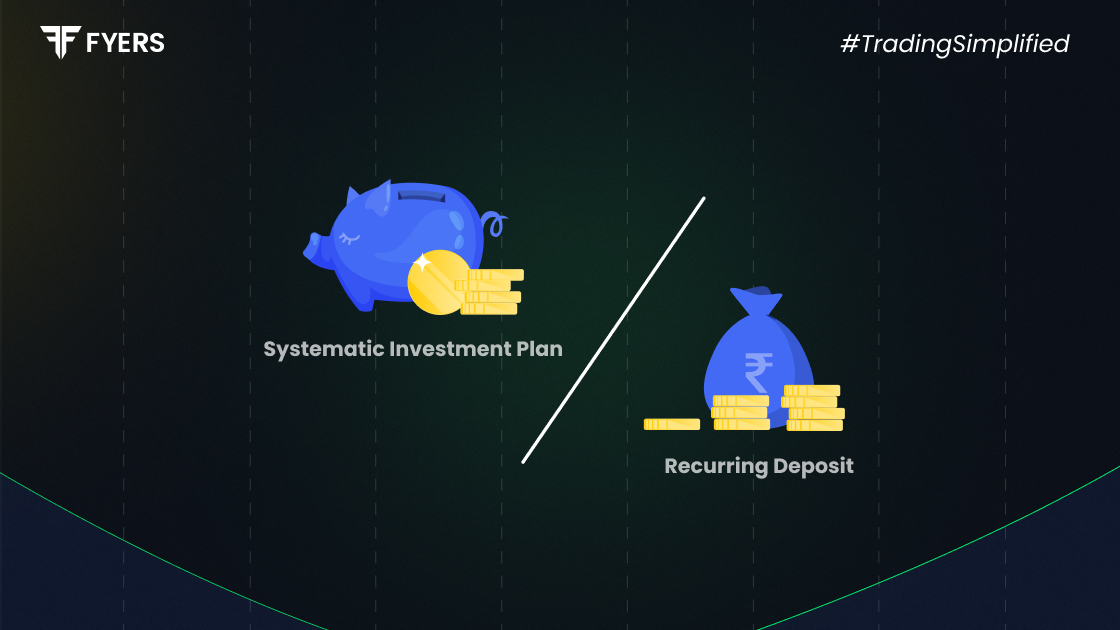

Many investors often compare SIP vs RD as disciplined investment options. Both are popular options for regular, systematic savings, but differ significantly by risk, returns, and liquidity. In this article, we will explain SIP and RD, compare them, and help you decide which is better for you.

A recurring deposit account (RD) is a fixed-income savings product offered by banks and post offices in India. Investors put in a fixed amount each month for a set period and earn guaranteed interest on those savings.

A systematic investment plan (SIP) lets you invest a fixed amount in mutual funds regularly. Instead of keeping your money in a bank account, SIP puts it into stocks or bonds to help it grow over time.

Both SIP and RD encourage disciplined investing, but their underlying structures and risk profiles are quite different.

Here’s a quick comparison of difference between sip and recurring deposit to highlight how they vary:

|

Feature |

SIP |

RD |

|---|---|---|

|

Investment Type |

Market-linked (mutual funds) |

Fixed deposit product |

|

Tenure & Flexibility |

Flexible – can start/stop anytime |

Fixed tenure chosen at the start |

|

Returns & Risk |

Potentially higher returns, carries risk |

Guaranteed fixed returns, almost zero risk |

|

Tax Implications |

Subject to capital gains tax |

Interest income taxable as per slab |

This comparison shows that SIP can offer higher rewards but comes with market risk, while RD is safer but offers lower, fixed returns.

Many investors prefer SIP because of its unique benefits:

Higher potential returns: Since SIP invests in mutual funds, it leverages market performance to potentially deliver better returns compared to traditional deposits.

Power of compounding: Regular investing over a long horizon helps your money grow faster thanks to compounding.

Flexibility & liquidity: You can increase, decrease, or stop your SIP anytime, and take out your money whenever you need.

These advantages of sip make it an attractive choice for long-term wealth creation.

For conservative investors, RD offers several clear benefits:

Guaranteed returns: Your money grows at a fixed interest rate, unaffected by market volatility.

Simple & low risk: Ideal for beginners who want steady savings without worrying about market movements.

Fixed tenure & discipline: Encourages you to save regularly over a defined period, building a habit of saving.

The advantages of rd make it suitable for short-term goals or risk-averse savers.

When comparing sip vs rd, understanding risk is crucial:

Market risk in SIP: Returns are not guaranteed as they depend on mutual fund performance. While the risk is higher, so is the potential reward.

Almost zero risk in RD: Since RD is a fixed-income product, it offers stable and predictable returns.

Investors with a higher risk appetite may choose SIP, while those wanting safety often choose RD.

Historically, SIPs in equity mutual funds have outperformed RDs over the long term. For example, a good SIP can earn about 10–12% per year, while RDs usually give only around 6–7%.

From a liquidity perspective:

SIP units can be sold partially or fully whenever needed, though long-term investors benefit the most.

RD usually requires completion of the tenure; premature withdrawals are possible but come with penalties.

So, sip or rd which is better depends largely on whether you value higher return potential over safety.

Here’s how you can decide:

Risk profile: If you can tolerate short-term market ups and downs for better returns, SIP might be better.

Financial goals: SIP suits long-term goals like retirement or wealth creation. RD fits short-term savings or emergency funds.

Investment horizon: Longer horizons (5+ years) favor SIP, while RD is ideal for 1–3 year goals.

By assessing your risk tolerance and goals, you can choose the right option or even combine both.

In short, SIP vs RD isn’t about which is better — it’s about which suits your goals. SIP offers higher potential returns with market risk, while RD guarantees safe, fixed returns.

Before deciding, consider your financial goals, risk appetite, and investment horizon. And remember, consulting a financial advisor can help you make a smart, personalized choice.

SIPs help build long-term wealth by investing in the market, which can grow your money faster through compounding.

SIP can give you higher returns, more flexibility in how much you invest, and easier access to your money than an RD.

Yes. SIP carries market risk, whereas RD is virtually risk-free. But with higher risk, SIP offers higher reward potential.

Absolutely! Many investors do both: SIP for long-term growth and RD for stable, short-term savings.

Calculate your Net P&L after deducting all the charges like Tax, Brokerage, etc.

Find your required margin.

Calculate the average price you paid for a stock and determine your total cost.

Estimate your investment growth. Calculate potential returns on one-time investments.

Forecast your investment returns. Understand potential growth with regular contributions.

You have successfully submitted your partnership request form. You will be hearing us soon!